CEE is transitioning from a generalist startup ecosystem to a region with a clear edge in defence and deeptech — but it remains structurally undercapitalized at scale. The single most important trend this quarter: capital concentration is reshaping the entire venture market — and CEE is beginning to benefit from it in defence and deeptech.

Key takeaways

- Global VC in 2025 was defined by extreme capital concentration. A small number of AI companies absorbed a disproportionate share of funding, leaving the rest of the market capital-constrained — especially at Series A and B.

- For CEE, Q4 looks strong on paper (€860 million), but stripped out the top 3 rounds, and the market shrinks by ~40–50%. The broader ecosystem remains early-stage and fragmented.

- Defence and dual-use technologies are emerging as one of the categories where CEE has a structural advantage globally.

- Europe is no longer lagging in AI — but it is still undercapitalized at scale. While early-stage activity remains healthy, the ability to finance breakout winners is increasingly dependent on international capital.

- The key question for 2026 is not whether capital is available — but where it concentrates next: infrastructure, applied AI, or geopolitically driven sectors like defence.

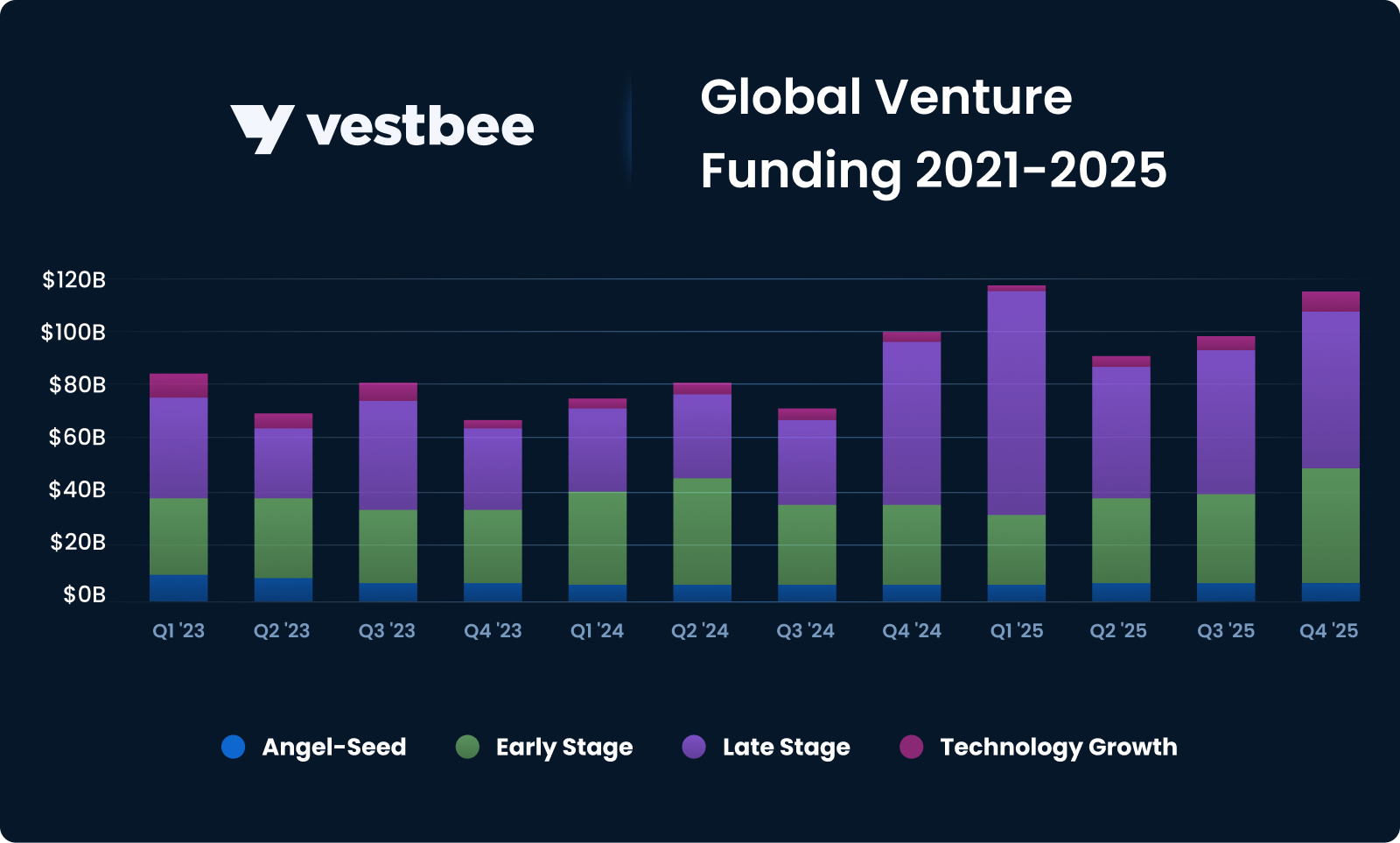

Global VC in Q4 2025: a record-breaking year defined by AI megadeals

Global venture funding reached $113 billion in Q4 2025, according to Crunchbase, making it one of the strongest quarters in recent years. However, the headline number hides a structural shift: capital is no longer distributed broadly. Instead, funding is increasingly concentrated in a small group of companies — primarily in AI infrastructure. Five companies alone accounted for ~$84 billion raised in 2025.

This is not just a cycle, but a different market structure.

This shift disproportionately hurts mid-stage companies that are too large for seed capital, but not dominant enough to attract late-stage mega-rounds.

The AI megadeal phenomenon

Five companies — OpenAI, Scale AI, Anthropic, xAI, and Project Prometheus — raised a combined $84 billion. That is roughly 20% of all global VC committed in 2025. These were not just large rounds. They represented a new class of industrial-scale AI infrastructure bets. The frontier AI race now requires massive, sustained capital to compete.

In Q4, late-stage funding reached $66.5 billion, up slightly quarter over quarter. Healthcare and biotech secured ~$71.7 billion across 2025 — the second-largest sector globally. Financial services attracted $52 billion. The U.S. accounted for ~65% of worldwide investment.

Funding trends across stages

The divergence between capital concentration and deal volume continued through Q4. Late-stage rounds swelled in size. Seed-stage activity showed resilience — $9.9 billion in Q4, up 12% year over year. The pipeline remained active even as the largest checks flowed to fewer companies.

Early-stage showed mixed signals. Deal counts declined while dollar volumes held firm. Investors are recalibrating after the 2021 cycle. Focus has shifted to founders with demonstrated product-market fit and capital efficiency.

Exits and IPOs

IPO activity continued its gradual recovery in Q4. Venture-backed companies found more receptive public markets in the second half of 2025, as institutional investors grew more comfortable with tech valuations at current rate levels. M&A activity remained steady, with strategic acquirers looking to buy AI capabilities rather than build them internally.

The 2025 picture: record capital at the top end, sustained activity at the base, and an IPO window gradually reopening. For 2026, the question is whether AI infrastructure spending plateaus as models mature, or whether the next wave of agentic and applied AI drives another leg higher.

Vestbee view: Capital concentration in AI is real and likely to deepen. The window for backing foundational AI companies may be narrowing — but the application layer is just opening. For most investors, that is where the opportunity now sits.

What this means for investors

- The bar for late-stage investing has shifted — capital flows to clear category leaders, not just competitive companies.

- Series A and B may offer the best risk-adjusted returns due to relative capital scarcity.

- AI infrastructure is becoming crowded — differentiation is shifting toward the application layer and distribution.

- Capital concentration increases downside risk if sentiment around AI shifts.

VC in Europe: AI takes the crown in a record year

European venture funding climbed to $16.6 billion in Q4 2025, up 27% year over year and 20% quarter over quarter — rounding out 2025 as a strong year for the continent’s startup ecosystem. According to Crunchbase, for the first time, artificial intelligence displaced all other sectors to become the leading category for European venture investment, attracting $17.5 billion across the full year. This reflects both the depth of Europe’s AI talent pool and the maturation of its enterprise technology market.

Funding geography and sectors

AI’s rise in Europe was not driven by a single country or cluster. Investments flowed into applied AI companies across the continent — from foundation model builders in France and Germany to enterprise automation platforms in the Nordics and Baltics. Europe’s share of global AI funding is growing.

Late-stage funding in Q4 reached $9.2 billion across 87 deals — up 65% year over year. This shows growing investor conviction around Europe’s most advanced scaleups. Participation from top-tier global funds shows that the European growth market is increasingly integrated with international capital flows.

Funding trends across stages

Early-stage investment totaled $5.3 billion across 250+ rounds in Q4 — down 4% year over year. This likely reflects a shift toward fewer, larger bets. Seed funding held steady at $2 billion across 750+ deals — consistent with 2024 levels and a positive sign for the pipeline.

Late-stage is strong. Early-stage isn’t. Same pattern as globally. European founders at pre-seed and seed face a more competitive environment, but those with clear product-market fit are finding willing backers. Cross-border investor participation — with U.S. and Asian funds investing in European rounds at record rates — shows Europe’s credibility as a source of globally relevant companies.

Vestbee view: Europe’s AI moment is real. But Europe is increasingly becoming an R&D layer for US tech — building companies that are ultimately financed, scaled, and often acquired by US capital. As a result, a growing share of value creation is captured outside Europe — even when the companies are built locally. That is not a funding story. It is a structural problem.

What this means for investors

- Europe has solved early-stage funding. It has not solved scaling.

- The best European companies are increasingly financed by US funds — local capital is not sufficient.

- AI is now the default category, which makes non-AI startups harder to fund regardless of quality.

- The gap between top-tier and average startups is widening.

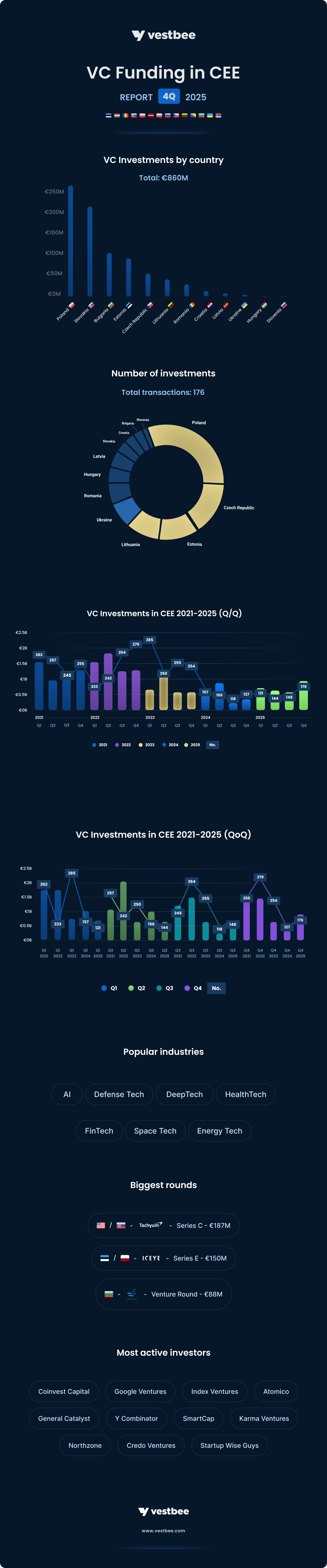

VC investment trends in CEE

Central and Eastern Europe: Q4 2025 in review

CEE closed Q4 2025 with €860 million raised across 176 rounds. At first glance, this looks like a strong quarter. In reality, the market remains highly uneven. A small number of large rounds — particularly in deep tech and defense — drove a significant share of total capital. Outside of these outliers, the ecosystem continues to operate primarily at the seed and early stages.

This is still a region that produces startups — not scaleups.

Strip out the top 3 rounds — Tachyum, ICEYE, and EnduroSat — and total CEE funding drops by roughly 40–50%. The market is significantly smaller than the headline number suggests.

Startup investment rounds in CEE in Q4 2025

- Number of funding rounds: 176 (160 fully disclosed in terms of date and funding amount).

- The biggest disclosed investment rounds: Tachyum, a $220M USD Series C round (US-based, Slovakia originating), ICEYE, a €150M Series E round (Poland-Finland), EnduroSat, a $104M USD Venture round

- Total value of funding closed in CEE: approximately €860M* (total value includes US-based, Slovakia-originating Tachyum and Poland-Finland ICEYE)

- Countries with the highest number of funding rounds: Poland — 54 rounds, Czech Republic — 28 rounds, Estonia — 20 rounds

- The most active VC funds: Coinvest Capital, GV (Google Ventures), Index Ventures, Atomico, General Catalyst, Y Combinator, SmartCap, Karma Ventures, Northzone, Credo Ventures, Startup Wise Guys

- The most popular industries: AI, Defense Tech, Deep Tech, HealthTech, FinTech, Space Tech, Energy Tech

*16 rounds undisclosed in terms of transaction value.

The key shift this quarter: defence and dual-use technologies

The most important shift in Q4 was the rise of defence and dual-use technologies. Unlike SaaS or fintech — where CEE competes globally on cost — defense may be the first category where the region has a structural advantage, driven by:

- proximity to geopolitical risk

- engineering talent

- increasing government demand

This is not a temporary trend. Defence and dual-use are likely to become one of the defining categories of the CEE ecosystem over the next decade.

What shaped the CEE ecosystem in Q4 2025

CEE’s venture market closed 2025 with 176 funding rounds. The rhythm of the quarter reflected familiar seasonal patterns: October was the most active month with 71 deals and over €500 million deployed. November slowed to 41 rounds and approximately €110 million, in line with the traditional pre-holiday deceleration. December rebounded to 48 rounds, amplified by one cross-border mega-deal.

Poland recorded 54 funding rounds — the highest deal count in the region — while Slovakia topped by total capital raised, driven by Tachyum’s $220 million Series C. The Czech Republic came second with 28 rounds, as Prague continued consolidating its position as a hub for enterprise SaaS, AI, and deep tech. Estonia delivered 20 deals — exceptional deal density relative to population size.

CEE is emerging as a beneficiary of Europe’s push toward defence sovereignty. Poland’s Orbotix (autonomous drone systems), Lithuania’s Luna Robotics (tactical FPV cameras), and Ukraine’s HIMERA (military communication systems) all raised capital this quarter, alongside larger dual-use players like ICEYE (satellite radar imagery) and PowerUp Energy Technologies (hydrogen generators). The structural shift toward European defense sovereignty is expected to drive capital flows into CEE’s defense tech ecosystem throughout 2026 and beyond.

AI investments remained active across the region, though the nature of rounds evolved. Q4 saw fewer “AI-as-a-pitch” deals and more companies with demonstrated enterprise traction — including Nexos (€30M Series A for enterprise AI orchestration), Resistant AI ($25M Series B for financial crime prevention), and Ranketta (€1M seed for AI brand visibility). Healthtech remained active, with Jutro Medical (€24M Series A extension), Digitail ($23M Series B), and Self.co (€1.2M), adding to CEE’s depth in medical AI and digital health platforms.

The quarter confirmed a continued increase in international participation. GV (Google Ventures), Index Ventures, Atomico, General Catalyst, and Northzone all participated in significant rounds. Local investors — led by Coinvest Capital, which completed four investments — remained the backbone of deal activity at seed and early stages.

If this trajectory continues, CEE is on a path to exceed €3 billion in annual venture funding by 2026, driven by a maturing founder community, deepening local fund infrastructure, and growing international recognition of the region’s technical talent.

Vestbee view: Strip out Tachyum, ICEYE, and EnduroSat from the €860 million, and the underlying market is solid but modest. The real story is structural: defense and deep tech are creating a category where CEE has genuine global relevance for the first time. That shift will outlast the current funding cycle.

What this means for investors

- CEE remains one of the most active seed-stage regions in Europe.

- Late-stage capital is still limited — most breakout companies will require international funding.

- Defense and dual-use may become the most important category in the region over the next 3–5 years.

- Headline funding numbers can be misleading due to deal concentration.

Now, let’s discover the noteworthy and recently raised VC funds from CEE.

New VC funds from CEE in Q4 2025:

Key pattern: fund formation in CEE is increasingly driven by public and institutional capital.

A significant share of new funds announced in Q4 relies on government-backed LPs (PFR, EIB, NATO Innovation Fund) and regional development mandates. This shows that private capital is still not sufficient to sustain the ecosystem independently. This creates stability — but also risks misallocation of capital if investment decisions become driven by policy rather than market dynamics.

- Croatian Provectus Capital Partners has reached a €162.5 million first close of its PCP SEE Fund II, targeting a final size of €250 million to invest in tech-enabled growth companies across Southeast Europe.

- Warsaw-based VC firm Expeditions has closed the first €100 million of Fund II, backed by NATO Innovation Fund (NIF) and the Polish Development Fund, to support founders and strengthen Europe’s tech and defense capabilities.

- Balnord, an early-stage investor focused on the Baltic Sea Region, has reached a first close for Fund I, exceeding its €70 million target. It is on track to reach €100 million by mid-2026. The fund will invest in deeptech and dual-use companies.

- Ukrainian VC firm Ukraine Phoenix Tech Fund has launched a €50 million fund backed by the European Investment Bank (EIB) and Bpifrance. The fund aims to support around 50 early-stage startups with up to €1 million each.

- Budapest-based VC firm Day One Capital has launched a €45 million fund to support early-stage tech startups in Central and Eastern Europe, with a focus on B2B software and innovative technologies.

- PFR Ventures has backed four new investment vehicles, including Betacluster Ventures, Cofounder VC, Stelo Ventures, and VO2 Ventures, providing a total of €46.3 million of the nearly €62 million available to finance Polish startups at various stages of growth.

Interested in other new VC funds investing in CEE and Europe? Check out our article about new VC funds investing in Europe in Q4 2025.

Let’s take a closer look at the Q4 results on a month-by-month basis. This review was solely based on fully disclosed rounds (name of startup, closing date, round’s size, participating investors).

Investment rounds in October

- Number of funding rounds: 71

- The biggest investment rounds: Tachyum, a €187M Series C round; EnduroSat, a €88M round; Starship Technologies, a €42.4M Series C; Better Payment Network, a €42.4M seed round

- Total value of funding secured in CEE: over €500M

- Countries with the most funding rounds: Poland — 20 rounds, Czech Republic — 12 rounds, Lithuania — 12 rounds

- The most active VC funds: GV, Y Combinator, 42CAP, SmartCap, Karma Ventures

- The most appreciated industries: AI, spacetech, deeptech, Fintech, enterprise software, defence tech

October was the quarter’s most active month, with 71 disclosed rounds raising over €500 million — headlined by two of the largest deals in CEE’s history.

- Slovakia-originating Tachyum closed a €187 million Series C, advancing its Prodigy Universal Processor designed to replace separate CPU, GPU, and TPU hardware in hyperscale data centers.

- Bulgaria’s EnduroSat followed with a $104 million round, drawing capital from Lux Capital, GV, and the European Innovation Council. Together, these two deals signaled a new chapter for CEE’s deeptech and space technology sectors.

Two further rounds shaped October’s landscape.

- Starship Technologies, the Estonian-founded autonomous delivery robot company, closed a $50 million Series C backed by SmartCap and Karma Ventures.

- Warsaw-based Better Payment Network secured a $50 million seed round from YZi Labs (formerly Binance Labs) to build stablecoin payment infrastructure — one of the largest blockchain seed rounds ever completed in the CEE region.

October’s deal activity reflected CEE’s broad innovation base: AI enterprise platforms (Nexos, Resistant AI), financial services infrastructure (BPN), space technology (EnduroSat), autonomous systems (Starship Technologies), and consumer edtech (Deepstash). Poland and Czech Republic led by deal count. Lithuania showed high per-capita activity driven by Nexos’s €30M Series A.

What mattered in October

- Two mega-rounds defined the month (Tachyum, EnduroSat) — both in deeptech and space

- Increasing participation of top-tier global funds

- Defence and AI presence across nearly every deal tier

Find out more: Top CEE funding rounds closed in October.

Investment rounds in November

- Number of funding rounds: 41

- The biggest investment rounds: GymBeam, a €30M round; Digitail, a €19.5M Series B; Kick, a €17M round

- Total value of funding secured in CEE: over €110M

- Countries with the most funding rounds: Poland — 9 rounds, Estonia — 7 rounds

- The most active VC funds: Coinvest Capital, Atomico, Partech, SmartCap

- The most appreciated industries: healthtech, AI, energy tech, retail tech, defence tech

November brought a predictable seasonal slowdown, with 41 disclosed rounds totaling approximately €110 million — roughly one-fifth of October’s capital deployment. Despite the quieter pace, the month delivered several strategically significant transactions.

- The largest deal came from Slovakia’s GymBeam, which secured €30 million from the European Bank for Reconstruction and Development and PortfoLion to continue scaling its fitness e-commerce model across 13 CEE markets.

- Romania’s Digitail followed with a €19.5 million Series B backed by Atomico and Partech, becoming one of the best-funded veterinary software companies globally.

- Kick, the AI-native bookkeeping platform co-founded by Polish entrepreneur Bartek Pucek, raised €17 million in a round backed by General Catalyst, GV, Felicis, and the OpenAI Startup Fund — one of the most high-profile November deals connected to the CEE ecosystem. With GV and the OpenAI Startup Fund on the cap table, the round signals conviction that automated accounting for small businesses is a durable, high-margin opportunity.

At the ecosystem level, November confirmed that Poland and Estonia maintained active deal flow even outside the year’s major deal clusters, while smaller ecosystems in Croatia, Lithuania, Bulgaria, and Latvia contributed steady seed and early-stage activity.

What mattered in November

- Health and climate tech carried the month despite lower deal volume

- Kick's round showed that the CEE founder diaspora is attracting tier-one US backers

- Poland and Estonia maintained consistent deal flow — the region’s two most reliable ecosystems

Find out more: Top CEE funding rounds closed in November.

Investment rounds in December

- Number of funding rounds: 48

- The biggest investment rounds: ICEYE, a €150M Series E round (Poland-Finland); Jutro Medical, a €24M Series A; duovo.ai, a €12.7M seed round

- Total value of funding secured in CEE: over €260M*

- Countries with the most funding rounds: Czech Republic — 13 rounds, Poland — 9 rounds, Estonia — 7 rounds

- The most active VC funds: South Central Ventures, General Catalyst, Coinvest Capital, Index Ventures

- The most appreciated industries: AI, healthtech, defence tech, deep tech, energy tech

*December disclosed dataset total of €260M includes ICEYE’s €150M Series E (Finland-Poland), also included in the quarter’s overall €860M figure.

December closed the quarter with 48 rounds and over €260 million in disclosed funding, headlined by ICEYE’s €150 million Series E led by General Catalyst. The Finnish-Polish company is accelerating plans to build out its synthetic aperture radar (SAR) satellite constellation and establish US manufacturing capabilities.

Within the CEE-headquartered deal flow, December was marked by quality over quantity.

- Warsaw’s Jutro Medical raised €24 million to extend its AI-first primary care rollup model.

- Prague-based duovo.ai raised a $15 million seed round led by Index Ventures, bringing together the founders of Rohlik — one of Central Europe’s most successful e-commerce exits — to build AI-powered automation for retail operations. CEE’s top founders are increasingly backed by the world’s top funds from day one, rather than needing to build regional credibility first.

The Czech Republic led by deal count with 13 rounds. Poland contributed 9 rounds, with Jutro Medical accounting for the bulk of Polish capital deployment. Estonia delivered 7 deals — consistent with its position as a disproportionately active early-stage ecosystem.

What mattered in December

- ICEYE’s €150M round was the clearest signal that CEE deep tech is attracting global institutional capital

- Czech Republic led deal count — Prague emerging as CEE’s most consistent late-year dealmaker

- Quality over quantity: fewer rounds, but several with serious international backing

Find out more: Top CEE funding rounds closed in December.

Now, let’s look closely at the most interesting CEE startups that closed rounds between October and December 2025.

Key patterns across top CEE startups

- AI-enabled infrastructure: Nexos, Resistant AI, duovo.ai

- Defense and dual-use: ICEYE, Orbotix, HIMERA, Luna Robotics, SalesPatriot

- Continued strength in vertical SaaS and marketplaces

- An increasing number of globally oriented companies from day one

Most companies are still early-stage, with relatively few late-stage scaleups.

Top CEE startups that closed funding rounds in Q4 2025:

Below is a curated selection of the most relevant startups — not just by size of round, but by strategic importance to the CEE ecosystem.

- Tachyum is a US-headquartered, Slovakia-originating semiconductor company developing Prodigy — the world’s first Universal Processor that unifies CPU, GPU, and TPU functions in a single chip, delivering 10x lower power consumption for hyperscale data centers and AI workloads.

- EnduroSat is a Bulgarian Space-as-a-Service provider that designs, builds, and operates software-defined nanosatellites, enabling commercial and scientific customers to access space data in weeks rather than years through its modular, cloud-connected satellite platform.

- Starship Technologies is an Estonian-founded company that develops autonomous six-wheeled delivery robots capable of navigating sidewalks and completing last-mile deliveries of groceries, food, and packages, having already completed over 9 million deliveries across 270 locations in 7 countries.

- Better Payment Network is a blockchain-native cross-border payment infrastructure built on BNB Chain, enabling instant stablecoin settlements between fiat-pegged currencies for banks, payment providers, and financial institutions, with transaction costs reduced from ~2% to 0.3%.

- Nexos is a Vilnius-based enterprise AI orchestration platform — founded by the creators of cybersecurity unicorn Nord Security — that provides organizations with secure, unified access to 200+ AI models through a single governed interface with built-in compliance controls and full visibility.

- GymBeam is a Slovak fitness e-commerce platform offering 500+ sports nutrition products and supplements across 13 Central and Eastern European markets, operating its own brands and logistics infrastructure and distributing over 4,000 packages daily.

- Jutro Medical is a Polish AI-first primary care operator that combines telemedicine, AI agents for clinical administration, and clinic acquisitions to modernize primary healthcare delivery, helping doctors reduce administrative burden and patients access faster, more continuous care.

- Resistant AI is a Prague-based provider of AI-native financial crime prevention models that protect financial automation systems from document fraud, synthetic identities, money mules, and transaction manipulation — with clients reporting 3x improvement in fraud detection and 90% automation rates.

- Digitail is a Romanian-founded AI-powered cloud practice management platform for veterinary clinics, integrating scheduling, medical records, invoicing, AI-driven SOAP note dictation, and a companion pet-parent app, currently serving over 10,000 veterinarians and 3 million pet parents.

- Katana is an Estonian ERP platform designed specifically for small and medium-sized manufacturers, covering inventory management, production planning, and e-commerce integrations (Shopify, Amazon, WooCommerce), helping manufacturers boost productivity by up to 80% across 1,300+ companies in 80 countries.

- duovo.ai is a Prague-based AI-driven automation platform for retail operations that integrates with SAP, portals, and legacy tools to automate repetitive workflows without coding, enabling retail and FMCG enterprises to reduce manual work by up to 40%.

- PowerUp Energy Technologies is an Estonian developer and manufacturer of modular hydrogen fuel cell generators originally engineered for space missions with the European Space Agency, now serving defense, off-grid, and commercial sectors with resilient, portable power solutions.

- Finax is Slovakia’s first robo-advisor and the first in Central Europe, offering AI-managed diversified ETF portfolios and personal finance management tools to retail investors across 6 EU countries, with regulated operations under the National Bank of Slovakia.

- Supernova Studio is a Czech-founded AI-powered design system platform — the first Czech company to graduate from Y Combinator — that unifies design, code, and documentation for product teams, automating workflow synchronization between Figma and engineering codebases for 400+ enterprise customers.

- Deepstash is a Romanian microlearning app that curates bite-sized insights from books, articles, podcasts, and videos across 200,000+ topics, helping professionals and students replace doomscrolling with structured daily learning, with over 12 million active users.

- GlycanAge is a Croatian-founded biotech company that measures biological age through glycan analysis of IgG antibodies in blood samples, providing individuals and clinicians with actionable data on how lifestyle, diet, and interventions influence the aging process.

- Evrotrust Technologies is a Bulgarian provider of qualified electronic signatures, digital identity (eID), e-delivery, and trust services compliant with EU eIDAS regulation, operating Bulgaria’s official national digital identity scheme and serving businesses across the European Union.

- Orbotix is a Polish defense tech startup developing AI-powered autonomous drone systems, including swarming technology and the Autonomous Target Acquisition System, designed for European defense forces, special operations, and critical infrastructure protection.

- Trustyfy Labs is an Estonian fintech company providing DeFi banking services, including crypto banking cards and financial tools to businesses and individuals, targeting expansion into emerging markets in Asia and Africa.

- Hyphen is a Latvian-founded AI startup that automates cloud infrastructure configuration, enabling developers to describe their service goals in natural language and automatically generate production-ready infrastructure across AWS, Google Cloud, Azure, and Cloudflare.

- BioResearch Pharma is a Polish clinical-stage biotech developing novel topical dermatological therapies for conditions including androgenetic alopecia and psoriasis, leveraging repurposed market-authorized compounds to address conditions affecting millions of patients globally.

- Yaga is an Estonian-founded online marketplace for secondhand fashion that operates as a social e-commerce platform with an escrow-based payment system, currently generating over €50M GMV annually and expanding from its market-leading position in South Africa into the Middle East and North Africa markets.

- Algori is a consumer analytics platform with a Lithuanian tech team that captures purchase data directly from shopper receipts to deliver real-time, SKU-level insights on brand performance, shopper behavior, and competitive positioning to FMCG brands and retailers across Europe and Latin America.

- MyDello is an Estonian B2B digital freight forwarder offering instant door-to-door pricing and routing across 400+ carriers for international shipments in all freight modes, with partnerships with DHL, Lufthansa, and Maersk, currently onboarding 12,500 businesses across Europe.

- Pikralida is a Polish clinical-stage biotech developing neuroprotective therapies for stroke, traumatic brain injury, and venomous snakebites, with its lead molecule PKL-021 (marimastat), advancing toward Phase II clinical trials.

- Boost.Space is a Czech no-code agentic database and integration platform connecting 2,600+ tools — including Make, Zapier, and n8n — to help businesses build a single source of truth for AI automations and workflows, with over 130,500 AI automations already running on the platform.

- Holi is a Polish fully digital obesity treatment clinic combining GLP-1 pharmacotherapy, AI-powered dietary coaching, and behavioral support through a subscription mobile app, helping patients achieve, on average, 17% body weight reduction in 12 months while cutting medication costs by up to 50%.

- Moontop is a Croatian flexible employee benefits platform allowing employers to set budgets and employees to customize their own benefits from a network of 500+ partners, including restaurants, fitness centers, healthcare providers, and mobility services.

- Vaxican is a University of Gdańsk spin-off developing next-generation anti-cancer vaccines using proprietary eVLP (enveloped virus-like particle) technology, also offering advanced next-generation sequencing (NGS) services as a certified Oxford Nanopore partner.

- HIMERA is a Ukrainian defense tech company developing secure, encrypted military-grade radio communication devices designed to operate in combat conditions, featuring 256-bit encryption, resistance to electronic warfare, and up to four days of battery life, with active deployments at the front line.

- Repsense is a Lithuanian AI-driven information analytics platform that tracks, detects, and forecasts how narratives spread across digital and traditional media, helping businesses, NGOs, and governments detect disinformation campaigns and manage reputational risks in real time.

- Rhuna is a Romanian on-chain payment infrastructure layer enabling stablecoin-based payments, ticketing, loyalty, and access control for entertainment venues, events, and theme parks, having already powered 165+ events, including UNTOLD and Neversea, with over 2 million users and $90M in volume.

- Kuube is a Hungarian developer of solar-powered off-grid smart public furniture — including benches with mobile charging, WiFi, and digital displays — deployed across 15+ countries, including Japan, Thailand, and the Philippines, and manufactured in partnership with Foxconn.

- Leil Storage is an Estonian developer of HDD-native software that optimizes shingled magnetic recording (SMR) drives for enterprise storage, delivering 20% more capacity per disk and 70% lower energy consumption, targeting the $22B enterprise storage market.

- Nodu is a Latvian-founded stablecoin infrastructure platform that provides banks, fintechs, and payment service providers with a compliance-ready framework for sending, receiving, and holding stablecoins under MiCA regulation, with automated KYC, AML, and regulatory reporting built in.

- eID Easy is an Estonian identity verification and e-signature aggregator that connects businesses to a global network of Qualified Trust Service Providers through a single API integration, making compliant digital identity and electronic signatures accessible across multiple jurisdictions.

- KatalistAI is a Slovenian-founded AI-powered video production platform used by 250,000+ professionals that transforms scripts into consistent shotlists, storyboards, and high-quality video outputs, serving content marketers, film producers, and creative agencies worldwide.

- Carfix is a Romanian SaaS platform that digitally connects insurers, brokers, auto repair shops, dealers, and leasing companies in a 100% online ecosystem for claims management, cost estimation, and preventive maintenance, reducing operating costs by up to 60% for its 150+ enterprise clients.

- Self.co is a Lithuanian digital health company offering at-home molecular allergy and food intolerance testing that detects 300+ allergens from a small blood sample, making accurate diagnostics accessible and affordable across Europe, currently expanding from Poland and Lithuania into Germany, Austria, and the UK.

- Desktop Commander is a Latvian AI desktop automation tool built on the Model Context Protocol (MCP) that enables AI assistants like Claude to manage files, run terminal commands, and execute real-world computer workflows using natural language instructions.

- Luna Robotics is a Lithuanian defense tech company that develops LunaCam — Lithuania’s first domestically manufactured FPV drone camera with true 24/7 visibility, built without Chinese components and already battle-tested in Ukraine.

- WorkQuest is an Estonian decentralized employment protocol combining AI-powered job matching, smart contract-based payments, and on-chain reputation scoring to create a transparent, borderless global labor marketplace for employers and workers.

- Ranketta is a Czech AI visibility platform founded by a 21-year-old AI researcher that tracks and optimizes brand presence in AI-generated search results from ChatGPT, Gemini, and Perplexity, helping e-commerce brands maintain accurate and prominent representation in the AI search era.

- VETSTOR is a Czech startup building a platform for pet longevity and veterinary health products, aiming to extend the healthy lifespan of pets through innovative nutrition and preventive health solutions.

- ICEYE is a Polish-Finnish company operating the world’s largest synthetic aperture radar (SAR) satellite constellation, delivering high-resolution Earth observation imagery for defense, insurance, disaster response, and government applications, having reached profitability and doubled revenues to ~€200M in 2025.

- Kick is an AI-native accounting platform co-founded by a Polish entrepreneur that automates bookkeeping for small businesses and accounting firms, integrating with major fintech platforms including Gusto, Mercury, Ramp, Stripe, and PayPal, with over 3,000 businesses adopted since launch.

- SalesPatriot is a Polish-American defense procurement platform that automates RFQ processing and order management for defense manufacturers and suppliers, helping them find, bid, and win contracts up to 7x faster — backed by Y Combinator and operating hubs in San Francisco and Warsaw.

- Minerva is a Polish B2B SaaS platform that automates EU public procurement workflows, enabling businesses to discover relevant tenders, analyze complex documentation, and submit compliant bids using AI, having helped clients win 383 tenders worth over PLN 250M within its first six months.

- Delta Green is a Czech virtual power plant operator that manages flexibility assets in households (solar panels, batteries, heat pumps, EVs) to reduce electricity costs, generate income for homeowners, and stabilize the energy grid, targeting tens of thousands of connected homes by 2026.

- Juo is a Polish subscription commerce platform that enables businesses to design, launch, and manage physical product subscriptions, supporting 500,000+ active subscriptions across hundreds of clients in Europe and North America in categories from supplements and cosmetics to medical equipment.

- Proteine Resources is a Polish biotech startup developing a fully autonomous insect protein manufacturing facility and functional beef alternatives for pet food rich in taurine and L-arginine, supported by the European Innovation Council and targeting 100 tons of annual production capacity.

- WhiteBridge AI is a Lithuanian AI-powered people research engine that finds, verifies, and analyzes publicly available data on individuals, helping professionals quickly verify identities, check backgrounds, and build comprehensive profiles with context rather than guesswork.

- Remix Global is a Bulgarian technology company operating Europe’s largest secondhand fashion recommerce platform across 9 countries, running one of the largest automated distribution centers in CEE and offering a Recommerce-as-a-Service (RaaS) model to retailers navigating new EU circular economy regulations.

Outlook for 2026

- Fewer rounds, but larger average ticket sizes

- Continued growth of defense and dual-use funding

- Increasing participation of US investors in CEE rounds

- More pressure on early-stage founders to show traction earlier

The question is no longer whether CEE can produce globally relevant companies, but in which categories it will dominate.

If the current trajectory holds, the next generation of globally relevant defense and deep tech companies may not come from Silicon Valley — but from Central and Eastern Europe.

If you have some insights about the report, drop me a line!

Want to get a more detailed view of the CEE startup & VC ecosystem in Q4 2025? Discover our monthly, quarterly, and yearly reports:

- VC Funding in CEE in Q3 2025

- New VC Funds Investing in Europe — Q4 2025

- TOP CEE funding rounds closed in October

- Top CEE funding rounds closed in November

- Top CEE funding rounds closed in December

Disclaimer: This report features VC rounds that have been publicly disclosed before the publication date or were shared by our VC and startup community. Grants, debt funding, and transactions below €50,000 were not considered. Furthermore, while we value all startups operating in CEE, our focus is on companies that originate from the region, self-identify as CEE companies, or have a significant presence of CEE founders.

Sources: Vestbee VC & startup community, startup press releases, open data from web & social media sources, DaaS platforms such as Crunchbase and Dealroom.