European defence, security, and resilience startups raised a record $8.7 billion in 2025, up 55% year-on-year and nearly four times higher than five years ago, according to the latest Dealroom and the NATO Innovation Fund report. Early 2026 is already bringing new major rounds — here are the key signals and the deals shaping the market.

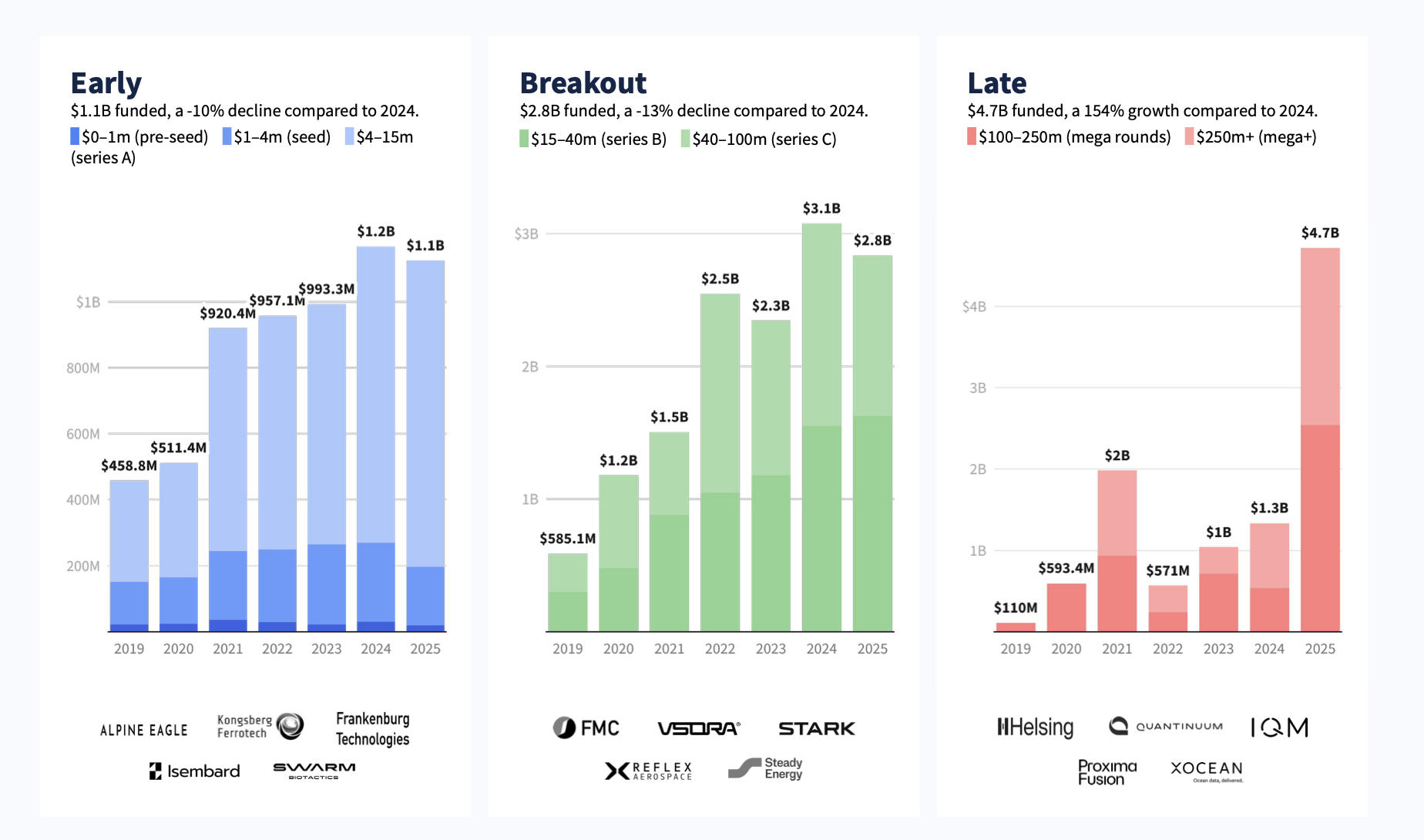

Growth driven by late-stage rounds

In 2025, the sector accounted for 43% of all deeptech funding and 13% of total VC investment in Europe, a share that has tripled in just three years. What used to be approached with caution is now acquiring a meaningful share of capital, driven by geopolitics, sovereignty concerns, and the growing need for deployable technologies.

At the same time, the way capital flows into the sector is changing. Growth is increasingly driven by large, late-stage rounds, which reached $4.7 billion in 2025, tripling year-on-year, while early-stage activity softened slightly. Rather than expanding the funnel, investors are concentrating capital into fewer companies — those already moving from research to real-world deployment.

Much of that capital is now anchored in AI

The technology underpinned 44% of all defence, security, and resilience funding, shaping everything from autonomous systems and drones to intelligence and decision-making infrastructure. Around it, adjacent areas such as quantum computing, AI chips, and satellite systems are scaling rapidly, pointing to a broader shift: defence is evolving into a full-stack technological domain.

Geographically, the market is both consolidating and expanding

The UK and Germany continue to lead in funding, while Munich is emerging as one of Europe’s central defence tech hubs, combining industrial infrastructure with a dense startup ecosystem. At the same time, Central and Eastern Europe is seeing the fastest growth in deal activity, even if that dynamics is not yet fully reflected in capital volumes. The result is a two-speed market — with capital concentrated in Western Europe, and innovation accelerating across CEE.

Record M&A, zero IPOs

M&A activity reached an all-time high in 2025 — up 4x compared to four years ago — while IPOs were absent. With many companies founded after 2022, the sector remains early, with most value creation still ahead rather than realised.

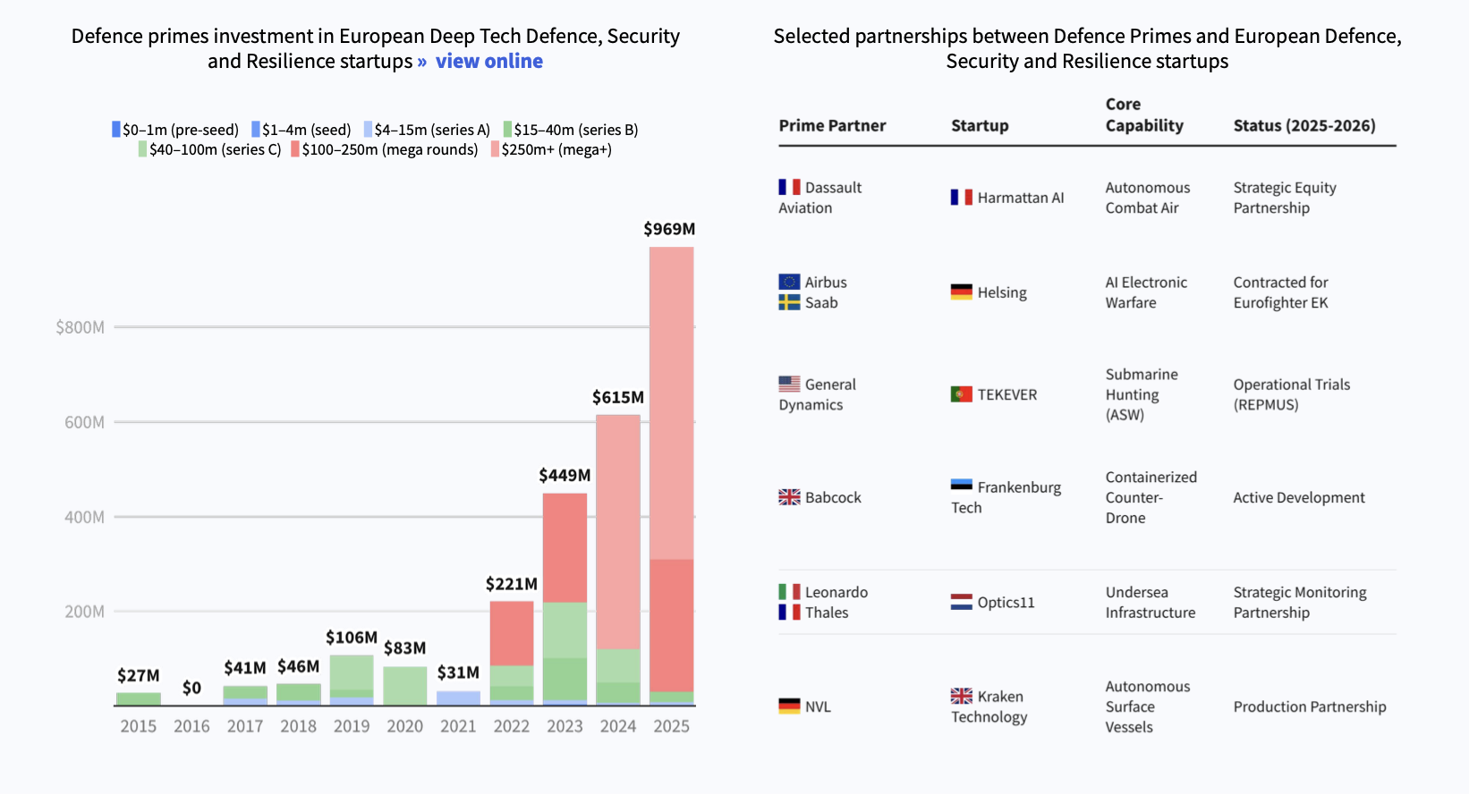

Alongside rising M&A activity, startups are increasingly working with defence primes, securing public contracts, and accessing grants — indicating that value creation is happening through multiple channels beyond traditional VC-backed exits.

If 2025 marked a record year for capital inflows, early 2026 is already pointing to the next phase

Larger and more strategic rounds are emerging, corporates and defence primes are becoming more active, and capital is moving closer to deployment and scale. In other words, the shift is no longer just about funding innovation — but about building and scaling real capabilities.

Here are the top defence and resilience deals of early 2026:

Paris-based Harmattan AI develops AI-driven defence systems, including UAVs and command-and-control software. The company raised $200 million in a Series B, backed by Dassault Aviation, to scale production and deployment across NATO and allied forces.

Founded in 2022, Uforce develops unmanned systems for air, land, and sea operations, tested in Ukraine. The company raised $50 million in a round led by Shield Capital and Lakestar to expand production and scale deployment across allied markets.

- Sensofusion raises €45M to scale counter-drone defence systems

Finnish Sensofusion develops counter-UAS systems for detecting, tracking, and neutralising drones. The company raised €45 million in a Series B round to scale the deployment of its airspace security solutions across defence and critical infrastructure markets.

- Onodrim Industries raises €40M to advance defence and industrial technologies

Amsterdam-based Onodrim Industries develops defence manufacturing, multi-domain sensing, and networked systems to support border security and military interoperability. The company raised €40 million in a seed round to scale its industrial and technology platform across Europe.

Founded in 2020, Munich-based TYTAN Technologies develops autonomous interceptor drones designed to detect and neutralise aerial threats in real time. The company raised €30 million in a Series A round co-led by Armira and the NATO Innovation Fund to expand manufacturing across Germany, Ukraine, and allied markets.

Estonia-based Frankenburg Technologies develops low-cost interceptor missiles designed to counter drone threats. The company secured €30 million in a Series A round led by Plural to expand manufacturing across Europe.

German/UK startup Hypersonica develops hypersonic missiles for European defence, designed for long-range, high-speed strike capabilities. The firm raised a €23.3 million Series A round led by Plural to advance testing and scale development of its missile systems.

Founded in 2016, Austrian startup Enpulsion develops electric propulsion systems for small satellites, enabling orbit control and manoeuvrability. It raised €22.5 million in a private equity round to scale production and expand its space mobility solutions for commercial, government, and defence missions.

Finnish startup Kelluu builds autonomous airships for intelligence and surveillance missions. The company raised €15 million in a round led by the NATO Innovation Fund to scale its platform for defence and dual-use applications.

Croatian startup Orqa develops FPV drones used in defence and industrial applications. It raised €12.7 million in a Series A round backed by Lightspeed and Expeditions to expand manufacturing capacity.

Kyiv-based Buntar Aerospace develops UAVs and mission-support software for reconnaissance and intelligence operations. The startup raised $10.4 million to expand the ISR platforms and scale deployment of its Copilot system for real-time situational awareness.