Key takeaways

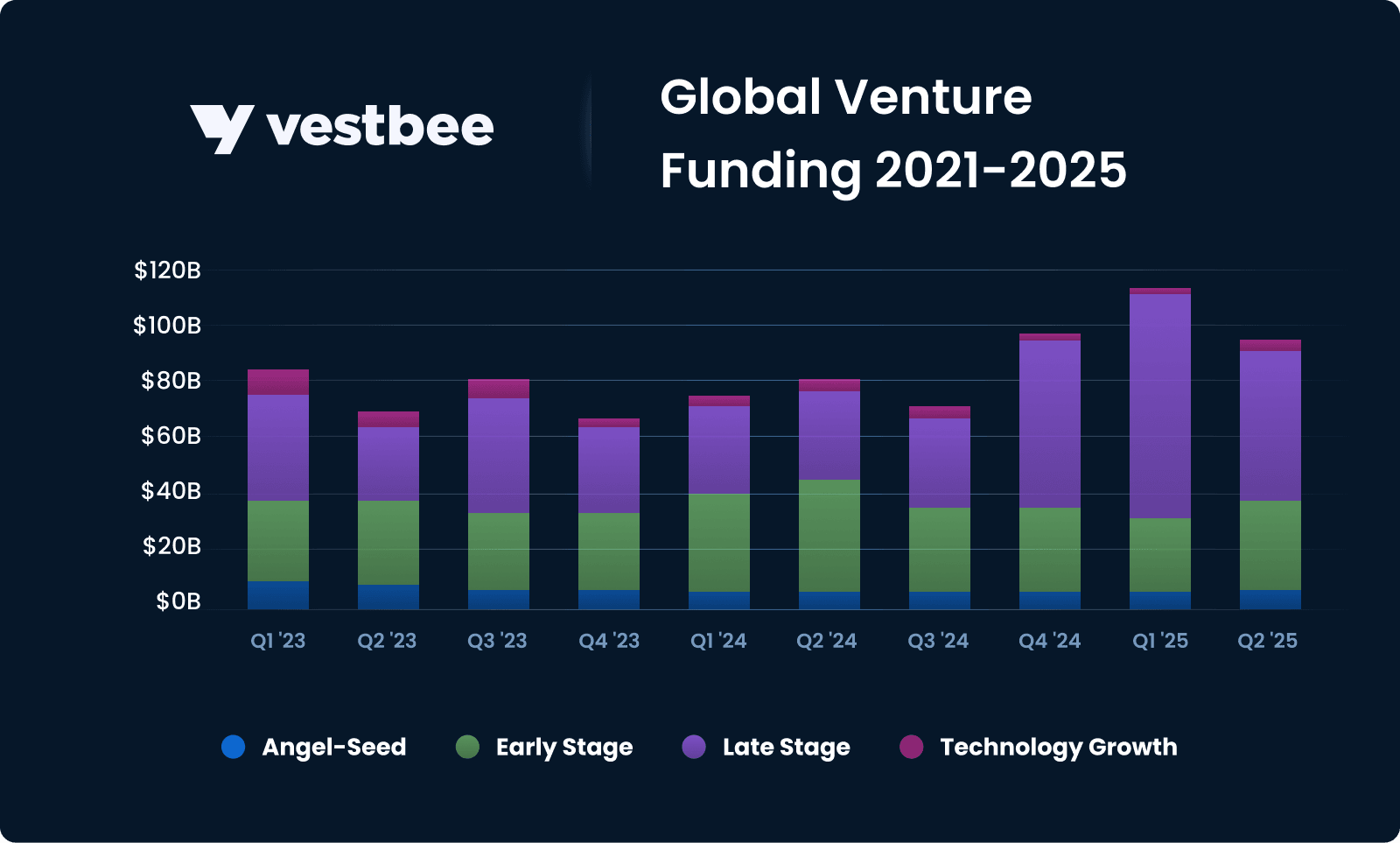

Global venture funding in Q2 2025 reached $91 billion, up year over year, despite a dip from Q1 highs.

- This quarter was marked by a significant concentration of capital into a handful of mega-rounds, especially in the AI sector, which alone captured $40 billion, with standout deals like Scale AI’s $14.3 billion raise.

- The US continued to dominate the landscape, accounting for two-thirds of all VC investment. While late-stage funding fueled most of the annual growth, early-stage deals held steady, particularly in fields such as quantum computing, energy, and therapeutics.

Venture funding in Europe held steady at $12.6 billion for 1,200 startups — unchanged QoQ, but 24% below last year’s peak.

- Germany surpassed the UK in capital raised for the first time since 2012, with significant activity seen in deeptech and high-growth sectors, yet the largest round was Turkey’s Dream Games at $1.25 billion.

- Growth-stage funding softened, accounting for just 10% of global late-stage VC, while early-stage deals remained relatively resilient at 19% of global allocation.

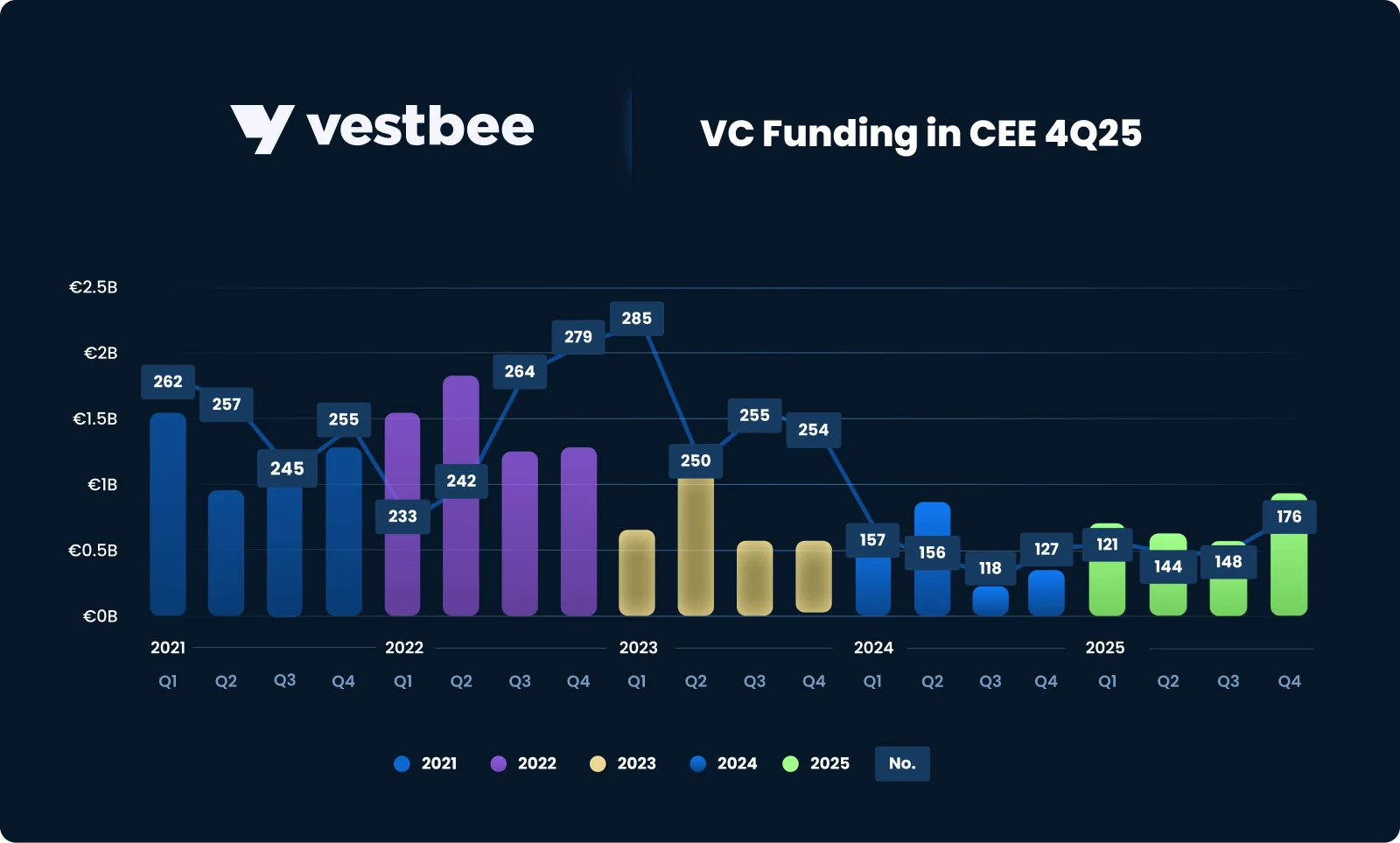

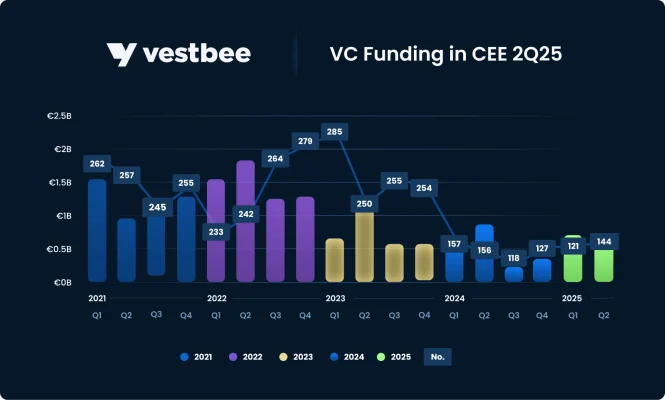

Venture activity in Central and Eastern Europe in Q2 2025 showed resilience, with 144 rounds and funding driven by a few standout transactions.

- Landmark raises from CEE-rooted global players like Cast AI, Aerones, and Pactum bolstered headline figures, but overall investment remained muted, highlighting investor selectivity.

- The region’s established hubs: Poland, Estonia, and Ukraine, led the activity, yet early-stage startups struggled to access meaningful capital. As the region’s ecosystem enterprise value expands, sustaining growth will require more inclusive capital access, stronger local funds, and proactive global investors’ engagement.

Global VC in Q2 2025: large deals dominance and AI surge

The global venture capital ecosystem showed sustained strength in the second quarter of 2025, albeit with some noteworthy shifts in the flow and concentration of capital. According to recent Crunchbase data, total investment activity reached $91 billion in Q2 2025, a healthy increase from $82 billion during the same period last year. However, this figure also represents a step down from Q1’s extraordinary $114 billion, a quarter that stood out as the highest point for global VC funding since late 2022. The pattern suggests a market recalibration after a strong start to the year, but overall momentum remains solid.

One defining feature of this period has been the pronounced concentration of capital in the largest deal rounds. Roughly one-third of all funds deployed in Q2 were allocated to just 16 companies, each of which secured at least $500 million in a single round. This trend underscores investors’ focus on high-impact plays and perceived market leaders, especially in the artificial intelligence sector. A particularly striking example is Scale AI, which landed a record-setting $14.3 billion investment in a single round, accounting for more than a third of all AI investments for the quarter.

Dominant sectors

AI has clearly emerged as the dominant force within the venture landscape. The sector attracted $40 billion or about 45% of all global venture capital deployed in Q2. This marks the third consecutive quarter where AI-focused startups have achieved record-setting levels of funding, signaling both investor enthusiasm and a belief in the sector’s transformative potential for a wide range of industries. Much of the capital continues to flow into AI research laboratories and infrastructure providers, establishing new benchmarks for what constitutes a “mega-round” in today’s VC environment.

Outside of AI, other sectors still commanded significant attention from investors.

- Healthcare and biotech companies collectively raised $14.8 billion in the quarter, making these industries the second-largest recipients of venture financing.

- Financial services followed, attracting $10.8 billion in VC capital. These figures highlight continued interest in sectors addressing essential aspects of human health and financial infrastructure, even as AI dominates the headlines.

Funding geography

Geographically, the United States remains the central hub for venture capital deployment, with American startups attracting $60 billion — roughly two-thirds of all VC funding for the quarter. This continued US leadership reinforces its position as the undisputed epicenter of global startup innovation and investment.

Funding trends across stages

Late-stage rounds drove much of the YoY growth, securing $55 billion in Q2, a surge of more than 53% compared to the previous year. Despite this strong annual growth, late-stage funding did decline by nearly a third from Q1’s peak, suggesting that while appetite remains robust, some cooling has followed a period of rapid acceleration.

Early-stage funding remained resilient, showing little change from the previous quarter at $26 billion deployed across approximately 1,600 companies. The largest early-stage investments reached up to $220 million, with significant Series A and B rounds seen in innovative areas such as quantum computing, clean energy, autonomous vehicles, therapeutics, satellite technology, as well as human resources and enterprise chat software.

In summary, the venture capital environment in Q2 2025 showcased a dynamic interplay between sector-specific surges, the increasing importance of large-scale deals, and the continued dominance of the US market. While AI continues to rewrite the record books, other innovation-driven sectors remain attractive, and the market overall appears poised to maintain its momentum in the face of evolving macro and industry trends.

VC in Europe: stabilization amid shifting hubs and shrinking market share

The European venture capital market demonstrated a period of stabilization in Q2 2025. Aggregate funding activity settled at $12.6 billion across approximately 1,200 startups, maintaining parity with the preceding two quarters but representing a 24% contraction from the record Q2 of 2024, according to Crunchbase data.

Funding geography and sectors

The regional capital allocation profile shifted, with Germany surpassing the UK in funds raised, a first since 2012, highlighting evolving dynamics in European innovation hubs and investor appetite. Despite Germany’s strong performance, the largest deal of the quarter originated in Turkey, where Dream Games closed a landmark $1.25 billion round, illustrating the outsized impact of outlier transactions in shaping quarterly funding totals.

The largest funding rounds were also concentrated in deeptech, with significant capital deployed into verticals such as defence technology, quantum computing, new energy, robotics, aerospace, therapeutics, in addition to key fintech and enterprise software plays. Berlin-headquartered Helsing, an AI-enabled defence tech startup, secured a $694 million Series D, while Spain’s Multiverse Computing attracted $218 million for quantum software, a testament to investors’ continued conviction in Europe’s emerging frontier technologies.

Examining country-level capital flows, Germany captured $2.8 billion, overtaking the UK’s $2.5 billion, which marked a post-2019 low. France remained resilient, attracting $1.8 billion in venture investment.

Funding trends across stages

Market segmentation by stage revealed that growth-stage deployment totaled $5.7 billion across 75 transactions, amounting to just 10% of global late-stage funding, reflecting softer LP appetite and lower allocation for European scale-ups relative to global peers. Early-stage deal activity was comparatively robust: $5 billion was invested across 270+ rounds, amounting to 19% of global early-stage pools, but still trailing North America’s heft at just over a third of its volume.

On a macro basis, Europe’s share of global VC investment compressed to 13% in H1 2025, down materially from 19% in the same period last year, underscoring increasing competition for capital on a global scale. Year-to-date, aggregate funding in the region declined 11% YoY, highlighting an environment where investors are both more selective and more focused on high-conviction bets, especially as the continent contends for relevance amidst strong US dominance and the ongoing surge in next-generation technology sectors.

VC investment trends in CEE

Central and Eastern Europe: steady deal flow with late-stage round dependency

In the second quarter of 2025, startups across Central and Eastern Europe closed 144 publicly reported funding rounds, collectively raising in excess of €640 million. Each month, deal counts remained steady, typically fluctuating between 35 and 42 rounds, suggesting a foundational level of ongoing entrepreneurial activity. Yet, this aggregate funding was notably skewed: a small number of landmark transactions, such as the headline rounds secured by Cast AI, Aerones, and Pactum, accounted for a substantial portion of total capital raised, with many early- and even mid-stage startups continuing to face pronounced funding challenges.

Beneath the surface, the broader market saw relatively muted interest beyond a handful of standout companies, and several rounds outside these headline deals were modest in size, reflecting a cautious investor stance and selective risk appetite.

While the ability to consistently generate deal flow demonstrates the inherent resilience and promise of the CEE innovation landscape, the persistent concentration of funding into just a few large-scale rounds highlights an important vulnerability: the ecosystem’s dependency on occasional blockbuster deals for overall growth metrics.

For CEE to achieve sustained scale and become a true contender within the global startup arena, it is critical to broaden and deepen access to capital, particularly for early- and growth-stage ventures.

- This may be achieved by nurturing a greater pool of local investors, fostering new and repeat founders through training, mentorship, and community support, and encouraging the entry of more international funds committed to long-term regional engagement.

- Public and private sector stakeholders alike should prioritize policies and programs designed to catalyze early-stage investments, build syndication capacity, and anchor new funds that can provide not just capital, but also hands-on guidance and network effects. Supporting angel networks, simplifying cross-border investment procedures, and amplifying success stories to attract follow-on funding will also be vital.

Ultimately, a more diversified and active VC environment, supported by both regional and global partners, will empower a wider spectrum of CEE startups to advance from concept to scale, reducing dependency on sporadic large rounds and fueling continuous innovation, job creation, and economic expansion throughout the region.

Startup investment rounds in CEE in Q2 2025

- Number of funding rounds: 144 (116 fully disclosed in terms of date and funding amount).

- The biggest disclosed investment rounds: Cast AI, a €93M Series C round, Aerones, a €53M venture round, Pactum, €47M Series C round

- Total value of funding closed in CEE: over €640M* (total value includes Lithuanian-rooted but US-based Cast AI and Estonian-founded but US-based Pactum)

- Countries with the highest number of funding rounds: Poland — 48 rounds, Estonia — 20, Ukraine — 17 rounds

- The most active VC funds: Smok VC, FIRSTPICK, Inovo VC, Hard2Beat, LAUNCHub Ventures, Startup Wise Guys

- The most popular industries: AI, deeptech, financial services, SaaS, security, energy.

*28 rounds undisclosed in terms of transaction value.

What shaped the CEE ecosystem in Q2 2025

In the second quarter of 2025, Central and Eastern Europe’s VC market delivered 144 funding rounds, maintaining a stable pace with 39 disclosed investments in April, 42 in May, and 35 in June. While the overall deal volume reflected a degree of investor caution, likely shaped by prevailing macroeconomic challenges, the steady month-to-month activity highlights a foundational level of resilience within the region’s startup ecosystem.

Several headline-grabbing transactions drove the lion’s share of capital inflow this quarter, notably Cast AI’s €93 million Series C round (Lithuanian-founded, US-headquartered), Latvia’s Aerones with a €53 million venture round, and Pactum (Estonia-founded, US-based) securing €47 million in Series C funding.

These landmark deals underscore not only the region’s capacity to generate high-potential ventures but also reinforce a well-established pattern: the most ambitious CEE-born startups are increasingly establishing legal or operational presences in Western Europe or North America, enabling access to deeper capital markets and broader commercial opportunities.

On a country-by-country basis, Poland, Estonia, and Ukraine stood out as the region’s most active ecosystems, recording 48, 20, and 17 transactions, respectively. Collectively, these three hubs contributed nearly 55% of all deals and about 30% of total capital raised in Q2, a testament to their comparative ecosystem maturity, founder pipelines, and expanding networks of repeat entrepreneurs — all factors that continue to attract both local and international investment.

Sectorally, investor preference in CEE remained aligned with broader European and global venture trends, with heightened interest in AI, deeptech, fintech, software-as-a-service, cybersecurity, and energy. This sectoral convergence signals both the region’s growing integration into global innovation currents and its ability to compete for capital and talent in next-generation fields.

Now, let's discover the noteworthy and recently raised VC funds from CEE.

New VC funds from CEE in 2Q 2025:

- Rockaway Ventures, a Prague-based investment fund under the Rockaway Capital group, has closed its second fund at nearly €55 million to back late-seed and Series A startups across CEE and Western Europe.

- Polish VC firm Movens Capital has launched a €60 million multi-stage fund to invest in CEE-founded startups at pre-seed, seed, and Series A+ stages. As of Q2 2025, it has achieved a €40 million close.

- Vilnius-based VC firm Iron Wolf Capital has raised €30 million for its second fund, with a final target of €100 million. It will support and scale deeptech startups across Estonia, Latvia, Lithuania, and Baltic founders globally.

- Vilnius-based second-hand marketplace app Vinted has launched Vinted Ventures. It aims to invest in Series A to C startups, driving re-commerce and encouraging sustainable consumer behavior. Cheques will range from €500,000 to €10 million.

Interested in other new VC funds investing in CEE and Europe? Check out our article New VC Funds Investing in Europe — 2Q 2025.

Let's take a closer look at the Q2 results on a month-by-month basis. However, this review was solely based on fully disclosed rounds (name of startup, closing date, round’s size, participating investors).

Investment rounds in June

- Number of funding rounds: 35

- The biggest investment rounds: Aerones, a €53M venture round, Pactum, €47M Series C, Dronamics, €29.8M venture round

- Total value of funding secured in CEE: over €240M

- Countries with the most funding rounds: Poland — 10, Estonia — 5, Lithuania — 5

- The most active VC funds: Iron Wolf Capital, BD Partners, Vinci

- The most appreciated industries: robotics, enterprise software, energy

In June 2025, startups from CEE collectively raised over €240 million across 35 disclosed funding rounds. Poland, Estonia, and Lithuania registered the highest deal activity with 10, 8, and 8 transactions respectively, yet it was Latvia and Estonia that dominated by capital raised, primarily fueled by landmark investments in Aerones and Pactum. The month’s headline funding was notably amplified by these major rounds, with Bulgarian-based Dronamics also securing a significant €29.8 million funding.

Collectively, just these three transactions represented more than half of June’s total capital deployed, underscoring the region’s current dependence on a few large-scale investments to drive overall volume. Absent these outlier deals, the underlying level of activity is substantially less vigorous.

From a sector perspective, June’s investments were concentrated in robotics, enterprise software, and energy — verticals that both reflect CEE’s emerging specialization and echo broader global investment priorities.

The local investor community remained active, with firms such as Iron Wolf Capital, BD Partners, and Vinci backing ventures across the region. At the same time, the participation of international funds, most notably Lightrock and Insight Partners in high-profile rounds, highlighted the growing cross-border appeal of select CEE technology companies.

Find out more: Top CEE funding rounds closed in June.

Investment rounds in May

- Number of funding rounds: 42

- The biggest investment round: EnduroSat, a €42M venture round, Genomika, a €5M venture round, Deus Robotics, a €4.2M Series A

- Total value of funding secured this in CEE: over €90M

- Countries with most funding rounds: Estonia — 9, Ukraine — 8 rounds

- The most active VC funds: Silicon Gardens, Inovo.vc, NGL

- The most appreciated industries: robotics, health, space, AI

May 2025 marked the slowest month for venture funding in CEE within the first half of the year, with just over €90 million raised through publicly announced rounds. The month’s headline transaction was a €42 million investment into Bulgaria’s EnduroSat, which alone made up nearly half of all capital deployed, underscoring the influence of single, large-scale deals in shaping monthly figures.

Estonia and Ukraine led the region in deal volume, recording nine and eight transactions, respectively. However, Bulgaria claimed the top spot in terms of capital raised, thanks chiefly to the EnduroSat deal.

On the investor front, local players such as Silicon Gardens, Inovo.VC, and NGL emerged as some of the most active backers across multiple deals. In parallel, global funds, including Founders Fund, Morphosis Capital, and Ceecat Capital, helped anchor the largest round of the month. Their participation signals a measured but noticeable willingness among select international investors to engage with high-potential opportunities emerging from the CEE region.

In terms of sectoral focus, capital remained concentrated in high-growth, innovation-driven verticals: robotics, health, space, and AI. These segments continue to attract both local and international capital, reflecting their alignment with broader strategic priorities and their perceived scalability.

Nevertheless, despite a few standout successes and continued interest in future-facing sectors, the overall market picture remains one of caution. Deal sizes were heavily skewed toward a handful of transactions, while early-stage activity across the broader ecosystem remained subdued. This points to a persistently risk-averse investment climate, where proven or later-stage ventures are more likely to access capital, while emerging startups face greater challenges in securing early backing. At the same time, the participation of leading global investors, though positive, remains sporadic, and often tied to only the most mature or market-ready companies.

Find out more: Top CEE funding rounds closed in May.

Investment rounds in April

- Number of funding rounds: 39

- The biggest investment round: Cast AI, a €93M Series C round, Ultra.io, a €10.2M venture round, Ominimo, a €10M venture round

- Total value of funding secured in CEE: over €230M

- Countries with the most funding rounds: Ukraine — 8 rounds, Estonia — 6 rounds, Poland — 6 rounds

- The most active VC fund: Lunar Ventures, Vesna Capital

- The most appreciated industries: Enterprise Software, Fintech, AI, Health.

In April 2025, startups across CEE raised over €230 million across 39 publicly disclosed funding rounds. Despite occasional headline-grabbing mega-deals, the underlying funding environment remains subdued, defined by a limited flow of capital beyond a handful of established players. The heavy influence of outlier transactions such as Cast AI’s round distorts the true state of the market, which, when adjusted for these exceptional cases, signals that venture activity in the region is still constrained.

Ukraine emerged as the most active country, leading the region with eight completed funding rounds. Poland and Estonia followed closely, each recording six deals. A nearly 20% decline in deal count compared to early 2024 demonstrates sustained investor conservatism amid ongoing macroeconomic headwinds. While sectors like enterprise software, fintech, AI, and health continue to attract funding in line with continental and global trends, genuine breadth and depth of deal activity remain elusive.

This increasing concentration of capital in a select few mature startups is a double-edged sword: it validates the region’s ability to build globally competitive companies but simultaneously exposes a vulnerability at the foundational layer of the ecosystem. Without resurgent interest, particularly in earlier-stage ventures and from a wider pool of both local and international backers, the risk is that grassroots innovation and pipeline development may stagnate.

To ensure long-term resilience and continued relevance on the global venture stage, CEE needs to broaden its funding base, stimulate a healthier early- and growth-stage investment environment, and foster conditions that encourage more founders and investors to engage at all levels of the ecosystem. In the absence of such developments, the region risks losing momentum just as it seeks to convert its emerging reputation into lasting impact and value creation.

Find out more: Top CEE funding rounds closed in April.

Now, let’s look closely at the 50 most interesting CEE startups that closed rounds between April and June 2025.

Top 50 CEE startups that closed funding rounds in Q2 2025:

- Pactum is an AI-based platform enabling global companies to automate and optimize commercial procurement negotiations using agentic AI.

- Lendurai provides autonomous navigation systems for drones that operate without GNSS or radio signals using onboard AI.

- Magic Feedback is an AI tool that aggregates, analyzes, and categorizes customer feedback for actionable business insights.

- Flowstep is an AI-native design platform that helps product teams quickly create UI designs, wireframes, and user flows, streamlining the ideation process.

- Lifeyear is a digital health company delivering personalized cardiovascular care remotely through integrated clinical protocols, real-time monitoring, and AI.

- Aerones specializes in robotic systems for automated wind turbine inspection and maintenance, optimizing efficiency and safety for renewable energy operators.

- TAC Build is a Layer 1 blockchain project offering infrastructure solutions and a unique TON-Adapter for Web3 applications.

- Cast AI is a platform for automating cloud infrastructure management, reducing costs, and optimizing Kubernetes performance for applications.

- Sintra AI offers AI-powered solutions to optimize various business processes, with details specified on its solutions page.

- Astrolight Space develops space technology architectures and solutions.

- Traxlo provides a digital platform for retailers to improve workforce management and operational efficiency.

- Sortabrick delivers AI-driven technology to automate the sorting and resale of used LEGO bricks for enthusiasts and resellers.

- Filuta AI develops advanced AI models and software for business process optimization.

- Robotwin creates and manufactures industrial robotic systems and automation tailored for manufacturing and industrial use.

- Kardi.ai is a platform providing AI-enhanced cardiovascular health monitoring and remote patient care solutions.

- Oddin.gg is a B2B platform offering AI-powered esports betting odds, content, and integrity monitoring for the betting industry.

- Ominimo Insurance is a digital insurtech offering online motor insurance policies and leveraging AI to deliver competitive, user-friendly coverage solutions and risk assessment.

- Riptides provides a unified identity fabric for access control and secure, credential-free workload-to-workload communication across cloud-native and AI-powered software environments.

- Ingenix.AI builds AI-powered foundation models for clinical trials, integrating multiple biological data types to accelerate biotech research and drug development.

- Spacelift is a DevOps automation platform that allows teams to manage infrastructure as code with streamlined cloud workflows.

- SR Robotics develops robotics solutions, including modular submarines for underwater operations and innovative cleaning robots for maritime and industrial applications.

- ReSpo.Vision uses computer vision and AI to capture, analyze, and visualize sports performance data.

- Fresh Inset creates and patents post-harvest technologies like Vidre+™ stickers to extend the shelf-life of fruits, vegetables, and flowers by protecting produce freshness throughout the supply chain.

- DBR77 Robotics is an industrial robotics marketplace connecting manufacturers with automation providers and solutions.

- BidFinance offers a platform for debt portfolio management and trading, enabling efficient transactions for financial institutions.

- Neurolabs delivers AI-driven computer vision technology for automated object recognition in retail and logistics environments.

- EnduroSat builds advanced nanosatellites and provides satellite mission services for commercial and research clients.

- Dronamics designs and builds cargo drones for fast, cost-effective long-range freight transport.

- Thinkpilot develops an AI-powered workspace for product managers to structure, track, and optimize product development.

- Sunrise Robotics creates industrial robotic systems to automate manufacturing processes and boost efficiency.

- Wasp is an open-source web framework designed to accelerate development with React, Node.js, and Prisma.

- Prepia is a platform offering payment processing and transaction optimization for online businesses.

- PeopleForce provides an HR management suite for automating HR, performance, and employee engagement operations.

- Deus Robotics develops autonomous mobile robots (AMRs) for warehouse automation and logistics.

- pleso is a digital mental health platform connecting users with online therapy and mental well-being resources.

- Respeecher offers AI-driven speech synthesis that enables voice cloning for media and content creators.

- Banani is an AI-powered platform that enables users to generate and prototype user interfaces from text input, streamlining and democratizing beautiful, user-friendly UI design for teams and founders

- Esgrid provides ESG data analytics and management solutions to help companies measure and report on sustainability.

- WeSky develops aviation technology solutions for in-cabin entertainment and connectivity in aerospace.

- DecisionRules is a no-code engine for automating and managing business decision logic.

- DiffuseDrive builds AI-powered solutions for data management and training in physical AI systems.

- Skarbe provides software for automating document management and contract processing with AI.

- Asynchronics develops platforms for asynchronous collaboration, enabling productivity for distributed teams.

- mysite.ai offers AI-driven tools for website creation and personalized content for small businesses.

- Lace.ai delivers AI solutions to automate customer support and call center operations.

- Proteine Resources focuses on developing and producing alternative protein sources for food and feed industries.

- Defguard offers cybersecurity solutions specializing in user and device access management.

- Darvin creates business workflow automation and productivity software for teams.

- DefendEye provides AI-based security and surveillance technologies for personal and property protection.

- Neuromedical develops neurotechnology devices and digital health solutions for neurological diagnostics and therapy.

If you have some insights about the report, drop me a line!

Want to get a more detailed view of the CEE startup & VC ecosystem in Q2 2025? Discover our monthly, quarterly, and yearly reports:

- VC Funding in CEE in 2Q 2024

- Central and Eastern European Startups Report 2025

- New VC Funds Investing in Europe — 2Q 2025

- TOP CEE funding rounds closed in April

- TOP CEE funding rounds closed in May

- TOP CEE funding rounds closed in June

Disclaimer: This report features VC rounds that have been publicly disclosed before the publication date or were shared by our VC and startup community. Grants, debt funding, and transactions below €50,000 were not considered. Furthermore, while we value all startups operating in CEE, our focus is on companies that originate from the region, self-identify as CEE companies, or have a significant presence of CEE founders.

Sources: Vestbee VC & startup community, startup press releases, open data from web & social media sources, PFR’s (Polish Development Fund) reports, DaaS platforms such as Crunchbase and Dealroom.