2025 is the year defence tech breaks records. NATO startups have already raised $9.1 billion in VC funding, 1.4x more than in all of 2024. Europe alone has reached $1.5 billion, accounting for 6.2% of total investments, up from under 1% before 2020, according to new data from Dealroom. Yet the US still dominates, capturing 85% of all defence tech VC funding among NATO allies since 2019. The gap isn’t just financial, it reflects Europe’s struggle for strategic autonomy amid the war in Ukraine and growing uncertainty over transatlantic security.

In this article, Vestbee explores the state of European defence VC funding and what keeps the US so far ahead.

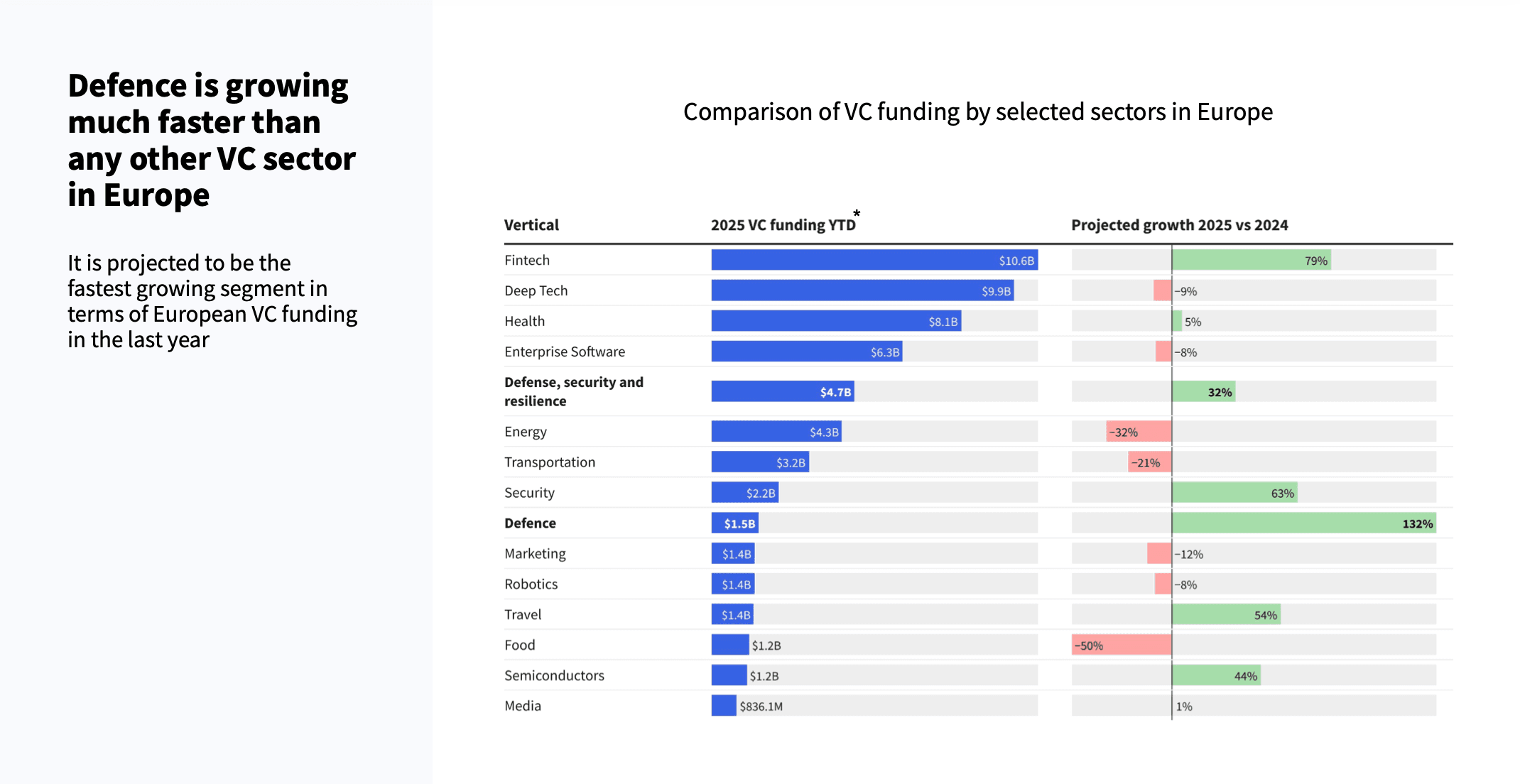

Record high investments for Europe

The European venture ecosystem has undergone a fundamental shift, finally leaving behind its previous caution towards military and dual-use businesses. According to Dealroom, defence is now Europe’s fastest-growing VC sector, projected to expand over 130% year-on-year, outpacing every other vertical.

The broader defence, security, and resilience (DSR) sector, including dual-use technologies, AI, robotics, and critical infrastructure protection, has become Europe’s most dynamic vertical over the past two years. Russia’s full-scale invasion of Ukraine and mounting concerns about the transatlantic security balance have pushed both governments and investors to rethink their roles and make DSR both a moral and economic priority.

“Readiness is the key”, said Marcin P. Kowalik, General Partner at Balnord, speaking at the Vestbee CEE VC Summit 2025, echoing the broader discussion trends across the ecosystem. “I try to concentrate one-third of my time on preparing for the war,” Kowalik explained. “And this is something I ask of my partners and startups. This is the crucial message from my side: we need to be ready.”

The picture for defence tech looks different in Central and Eastern Europe, where development is on the rise, but the region has received only 0.6% of overall European VC funding. More about the defence tech in CEE region read here.

Where the money flows

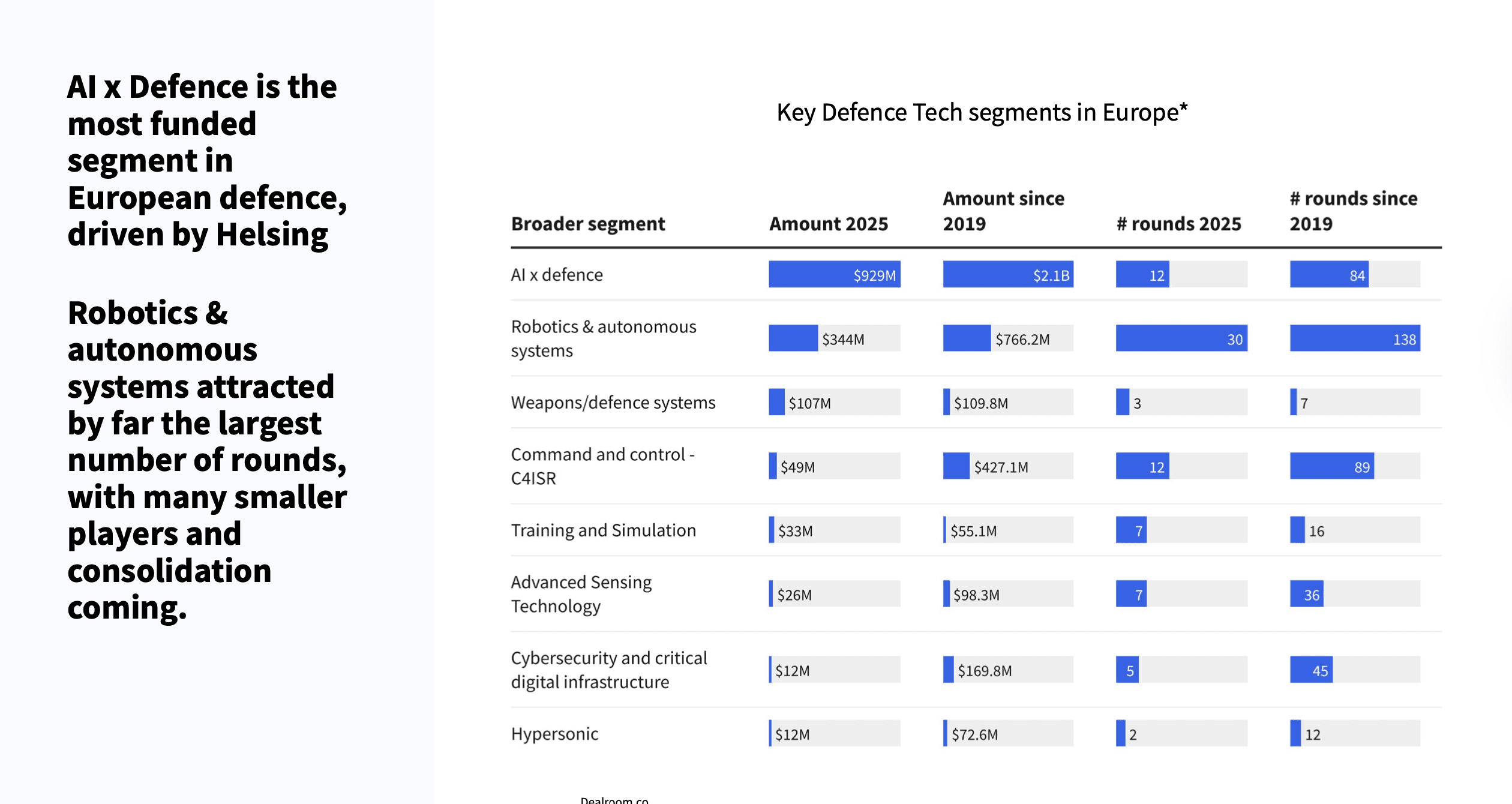

In 2025 alone, European defence VC funding hit $1.5 billion. AI x defence segment leads the charge, raising $929 million this year and $2.1 billion since 2019 — most of it through mega-rounds, which account for more than three-quarters of all funding this year. The surge is driven by Helsing’s record-breaking $600 million Series D round at a $12 billion valuation.

Robotics and autonomous systems follow with $344 million raised this year and 138 rounds since 2019, the most of any sub-segment signaling upcoming consolidation among smaller players. Other active areas include weapons systems with $107 million raised, Command and control solutions with $49 million and training and simulation with $33 million in investments.

Dual-use innovation in quantum, space and semiconductors continues to surge, with European quantum startups surpassing $1.6 billion in funding in 2025 and capturing 88% of global VC in quantum cryptography. Yet key gaps remain. Europe contributed only 12% of funding in space launch vehicles and 6% in AI chips between 2022-2025.

In drones, the US dominates decisively with 53% of global funding, compared to Europe’s 25%. Governments in the UK and France now see this as a strategic vulnerability, working with US semiconductor giants to scale AI infrastructure.

Geographically, Germany leads defence tech fundraising, attracting $2 billion since 2019. This success is largely attributed to the Munich-based Helsing, and a growing cluster of AI-driven dual-use startups. London follows with $485 million, and Paris, with $218 million. Notably, the UK also shows a distributed ecosystem, housing four of the top ten European hubs, as Dealroom data shows.

Investors' maturity and deeptech focus

The investment ecosystem itself is rapidly maturing beyond mere generalist curiosity. The number of investors participating in European defence deals is projected to increase 3.9 times since 2019. Crucially, specialized defence funds, including D3, Nato Innovation Fund, and Expeditions, are now driving deal flow — they participated in 34% of all defence rounds in Europe in 2025, nearly doubling their share from the previous year.

Over the past three years, Europe has seen a wave of new dedicated defence funds emerge. New entrants like Darkstar, Green Flag Ventures, Keen Venture Partners, ScaleWolf, and Hyperion have stepped onto the scene, as the maturing sector attracts larger international rounds. US investors now drive 40-50% of all capital flowing into European defence tech, underscoring its growing global pull.

The full list of the most active VC funds investing in European defence tech startups can be found here.

What’s with US defence tech funding

While Europe celebrates record growth, the US still wins the VC race in both scale and speed. Between 2021 and 2024, global investors poured $155 billion into defence tech startups, and in just the first half of 2025, US-based companies raised $28 billion of it. Since 2019, the US has received 85% of total NATO defence VC funding, according to Dealroom. So far in 2025, NATO allies have raised $9.1 billion, with Europe accounting for just 6.2% of that total.

Driving the US advantage are the so-called “neoprimes”, venture-backed disruptors challenging the dominance of traditional defence giants. Companies like Andurill Industries and Palantir Technologies operate faster, leaner, and with a "software-first" approach that mirrors Silicon Valley’s ethos of building "smarter, faster, and cheaper".

The number speaks for themselves. Anduril, founded by Oculus creator Palmer Lucky, closed a huge $2.5 billion Series G round in June 2025, reaching a $30.5 billion valuation. Other neoprimes, such as Saronic Technologies and Applied Intuition, followed with $600 million mega-rounds each.

So even with record investment in 2025, European defence spending will reach only 2.1% of GDP this year, well below NATO’s 3.5% target. As investors noted at the Vestbee CEE Summit 2025, gaps in critical areas like AI chips, launch vehicles, and secure satellites leave the region trailing. Without major reforms to speed up procurement, improve agility, and provide larger long-term capital, Europe risks falling further behind.