Global VC Investments

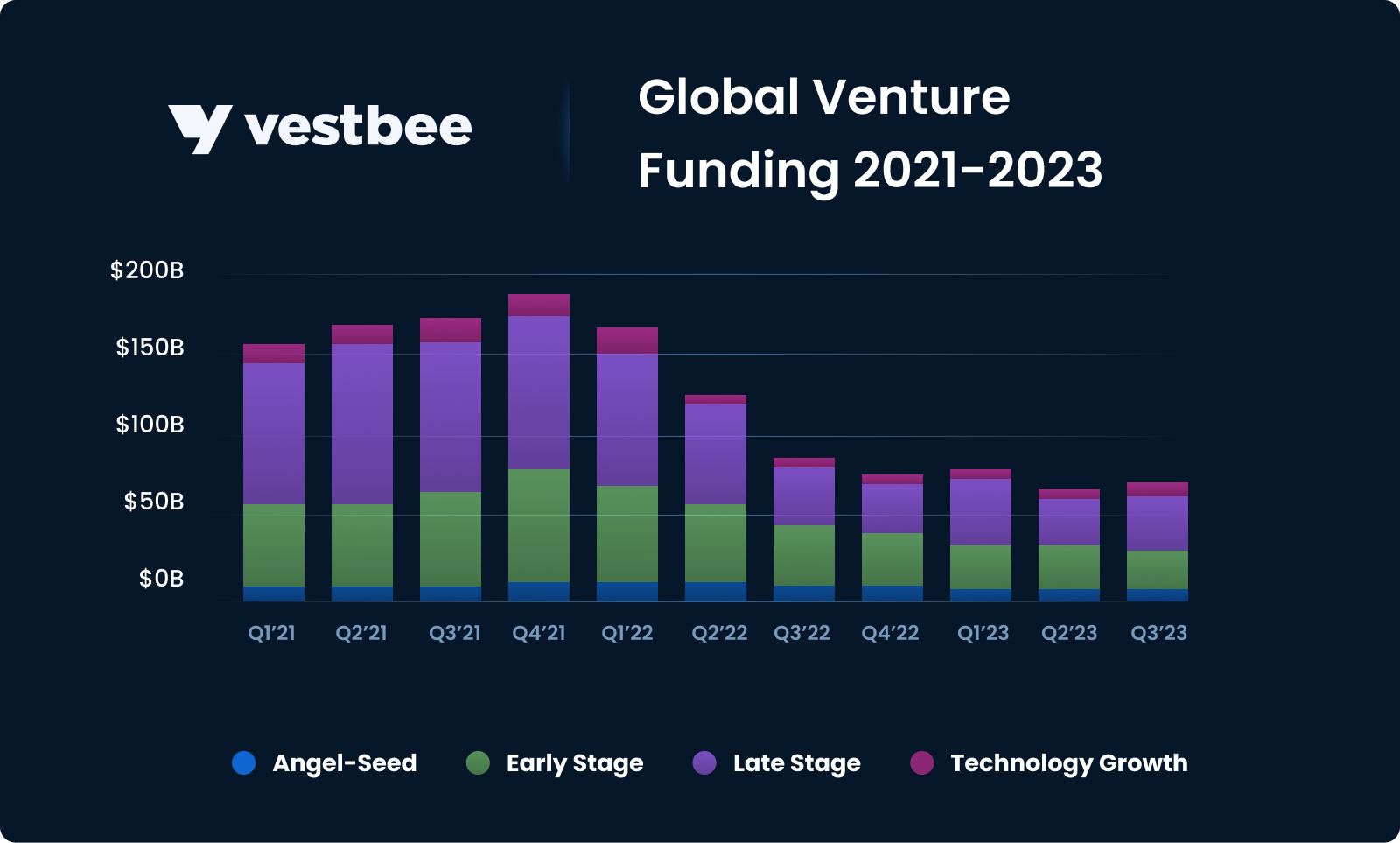

The third quarter of 2023 falls again despite a late-stage rebound led by huge AI deals. Global venture funding in the third quarter of 2023 reached $73 billion — up a bit quarter over quarter and down 15% from the $86 billion invested in Q3 2022, Crunchbase data shows.

Seed and early-stage funding, however, continued its decline year-over-year, reinforcing the notion that venture markets have yet to regain momentum fully. Late-stage funding was up by close to 10% year over year and 30% quarter over quarter. This upward trajectory was fueled by companies in strategic sectors such as semiconductors, AI, electric vehicles, and sustainability, which secured significant funding.

AI companies raised more than $10 billion this past quarter, on par with Q2 2023, Crunchbase data shows. The largest AI rounds went to OpenAI competitor Anthropic. The company raised $1.3 billion from Amazon. Cloud data company Databricks raised $500 million at a value of $43 billion in a deal led by T. Rowe Price. That was the largest priced round last quarter and marked an up round from Databricks’ $38 billion value in 2021.

In parallel, the semiconductor sector attracted $4.5 billion in Q3, with a noteworthy 96% of investments directed towards companies based in China, as per Crunchbase data.

In a nutshell, even with big investments in AI, semiconductors, and sustainability, the overall slump in global funding hasn't been stopped. The total global funding for the first three quarters of 2023 hit $221 billion, showing a significant 42% drop compared to the $381 billion invested in the same period in 2022. Moreover, the year-to-date global venture funding in 2023 lags behind the $501 billion invested between Q1 and Q3 2021, highlighting ongoing challenges and a careful approach in the global venture capital scene.

VC Investments in Europe

As per findings from Crunchbase, European startup funding surged to $16.4 billion in Q3 2023, representing a notable 28% quarter-over-quarter increase and maintaining a stable year-over-year performance. Despite this overall positive trajectory, a closer examination reveals a concentration of growth in late-stage funding. At the same time, seed and early-stage companies in Europe experienced their lowest stats in both funding amounts and counts.

Within Europe, the United Kingdom emerged as the largest recipient of funding in the third quarter, followed by Sweden, France, and Germany. This regional distribution aligns with broader funding trends observed globally.

Reflecting the global inclination, AI remains one of the primary investment directions in European investment portfolios. AI companies in Europe secured $1.8 billion in Q3 2023, constituting 11% of the continent’s funding and nearly one-fifth of the global AI funding pool. Key beneficiaries of these substantial rounds include Conigital, a UK-based driverless transport company, Helsing, a Berlin-based AI defense company, Poolside, an AI infrastructure company in Paris, Tractable, a London-based AI for disaster recovery firm, and Neura Robotics, a Germany-based consumer and industrial robotics developer, while among the least popular investment directions in Q3 2023 were Software in general, but to be more specific: HR, event tech, fashion, legal, and gaming.

In anticipation of Q4’23, VC investment in Europe is poised to maintain a cautious stance, with companies confronting challenges in securing funding. The prevailing high-interest rate environment may contribute to subdued VC fundraising activity, potentially leading to lasting repercussions for the VC market. Amidst this tightening landscape, consolidation may take center stage, with industry leaders securing funds while other startups face the risk of losing momentum or fading into obsolescence. Despite the broader investment slowdown, AI is expected to retain its allure for VC investors.

In this tough environment, we might see more consolidation taking place. Big players in the industry will probably get funding, but other smaller startups might struggle to keep going or become irrelevant. Even with the overall decrease in investments, the field of Artificial Intelligence is still likely to attract VC investors.

VC Investments in CEE - low but stable

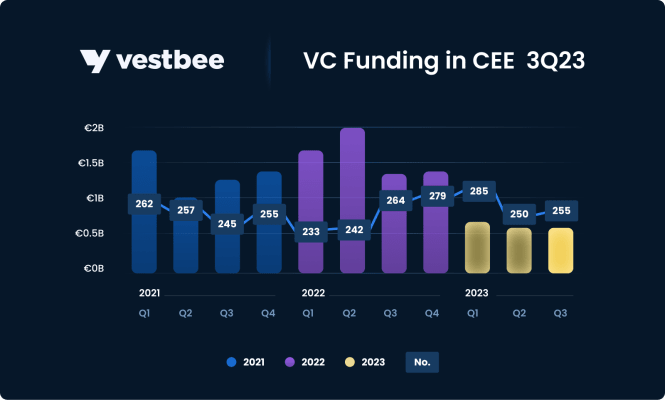

In the Central and Eastern European landscape, things in Q3 2023 stayed pretty much the same—no big dips, but no major leaps. We noted 255 investment rounds totaling €560 million, almost identical to what we saw in Q2 2023 (250 rounds and the same €560 million). This steadiness in investment volume and value indicates a pause in the downward trend in available financing. However, it's imperative to acknowledge that this resilient posture falls short of reinstating the heightened levels observed in the dynamic periods of Q1 and Q2 2022. In the CEE, public funds play a significant role in shaping the entrepreneurial landscape. Several public fund programs are reaching their end, and the new initiatives are still pending. This potential hiatus in program availability can make the upcoming Q4 even more challenging for startups. One noteworthy example is the Smart Growth Operational Programme, supported by PFR Ventures and NCBR. The investment periods for funds operating under this program are set to conclude by the year-end. Subsequently, the program will transition to the FENG program (European Funds for a Modern Economy) later. But still, Q4 is the last chance for them to invest the capital raised from investors.

To sum up, In the CEE, everyone's playing the waiting game, hoping for a spark to ignite some fresh excitement among investors. The path ahead offers opportunities, so let's stay sharp and see what the next quarters will bring to CEE.

Startup investment rounds in CEE in 3Q 2023

Number of funding rounds: 255 (170 fully disclosed in terms of amount, month, investors, and company details)

The biggest disclosed investment rounds: PV Case - Series B - €89M, SkeletonTechnologies - Venture Round - €50M, Preply - Series C (add-on) - €38.2M, DRUID - Series B - €28.2M, Hi - Venture Round - €27.3M, Nibulon - Venture Round - €27M, GenePlanet - Series B - €20M.

Total value of funding closed in CEE: over €560M*

Countries with the highest number of funding rounds: Poland - 95 rounds, Estonia - 35, Czechia - 24 rounds

The most active VC funds: Vitosha Venture Partners, Spinnaker Alfa, Baltic Sandbox Ventures, Credo Ventures, Hiventures, a16z, Aper Ventures, bValue Fund, Change Ventures, Czech Founders VC, Depo Ventures, Feelsgood Capital, FIRSTPICK, FJ Labs, FundingBox Deep Tech Fund, N1, Outlier Ventures, Presto Ventures, Specialist VC, Startup Wise Guys, Tera Ventures, Vesna Capital, Zaka VC.

The most popular industries: Energy, AI, Fintech, Cyber-security, SaaS, Analytics, Biotech.

*59 rounds undisclosed in terms of transaction value

When comparing the third quarter of 2022 with its counterpart in 2023, we can see a consistency in the volume of funding rounds, yet a striking downturn of over 56% in the aggregate financing value is evident. The total financing value secured in the market dropped from nearly €1.3 billion in Q3 2022 to €560 million in Q3 2023, underscoring the formidable challenges companies face in securing substantial capital investments during this period. This decline is connected to the prevailing macroeconomic landscape, marked by heightened uncertainty and further diminished participation of foreign investors in the CEE region, coupled with a reduced activity of public funds.

The lack of mega-rounds in CEE and the diminished involvement of foreign investors signals a potential paradigm shift in investor preferences and attitudes. Investors appear to be adopting a risk-diversification strategy, steering away from the high-risk and high-valuation landscape prevalent in mega-rounds.

Concurrently, the CEE market aligns itself with broader European trends, showcasing a decline in early-stage funding and a sustained focus on later-stage investments. This inclination could be correlated with the inherent lower risk associated with later-stage investments, aligning with the current trend of investors adopting a more cautious stance amid prevailing uncertainties.

Let’s look closely at what shaped the CEE ecosystem in Q3 2023.

During the second quarter of 2023, a total of 255 venture capital transactions were documented. Regarding the number of rounds, only one month (September) stands out, reaching 83 rounds. However, in July, startups collected the most funding (over €300M in 62 rounds), as per the comprehensive disclosed data.

Among the biggest rounds disclosed in Q3 were secured by Lithuanian PV Case - Series B - €89M, Estonian SkeletonTechnologies - Venture Round - €50M, Ukrainian Preply - Series C (add-on) - €38.2M, Romanian DRUID - Series B - €28.2M, Estonian Hi - Venture Round - €27.3M, Ukrainian Nibulon - Venture Round - €27M, and Slovenian GenePlanet - Series B - €20M.

In the third quarter, Poland, Estonia, and Czechia accounted for 95, 35, and 24 funding rounds, respectively. However, Lithuania held a commanding presence in terms of investment volume amassing over €115M.

The thematic focus of investment during this period unveiled a pronounced preference for sectors including Energy, Fintech, Cyber-security, SaaS, Analytics, and AI, while among the most active investors were Vitosha Venture Partners, Spinnaker Alfa, Baltic Sandbox Ventures, Credo Ventures, Hiventures, a16z, Aper Ventures, bValue Fund, Change Ventures, Czech Founders VC, Depo Ventures, Feelsgood Capital, FIRSTPICK, FJ Labs, FundingBox Deep Tech Fund, N1, Outlier Ventures, Presto Ventures, Specialist VC, Startup Wise Guys, Tera Ventures, Vesna Capital, Zaka VC.

Now, let's discover the note-worthy and recently raised VC funds from CEE.

New VC funds from CEE in 3Q 2023:

- EIT InnoEnergy has raised over €140M to support cleantech and energy innovation sectors.

- Ukrainian Horizon Capital raised $125M, focusing on tech companies in Ukraine and Moldova.

- Polish Inovo VC closed €105M fund to back early-stage-based founders with up to €4M investments.

- Polish Movens announced a €100M fund to support CEE startups with ticket size €250k - €5M.

- Polish-American ffVC announced a €60M fund to back late-seed to series A startups from Central Europe.

- Tilia Impact Ventures launched a €32M second fund to Drive Climate, Education, and Healthcare Solutions.

Interested in other new VC Funds investing in CEE and Europe? Check out our article - New VC funds investing in Europe.

Let's have a closer look at the Q3 results on a month-by-month basis. However, this review was solely based on fully disclosed rounds (name of startup, closing date, round’s size, participating investors).

Investment rounds in September

Number of funding rounds: 83

The biggest investment rounds: Sunly - Venture Round - €30M, IP Fabric - Series B - €21.1M, Woltair - Series A - €20.5M

Total value of funding secured in CEE: over €130M

Countries with the most funding rounds: Poland - 16, Estonia - 16 rounds.

The most active VC funds: Vitosha Venture Partners, Spinaker Alfa, Baltic Sandbox Ventures, Credo Ventures, Feelsgood Capital, FundingBox Deep Tech Fund, N1, Specialist VC, Startup Wise Guys

The most appreciated industries: AI, Cybersecurity, Fintech.

In September, the CEE startup landscape faced a challenging funding environment, with a total funding of just over €130 million distributed across 83 disclosed funding rounds. Despite these efforts, Poland and Estonia emerged as the leading contributors, with 16 investment rounds each. Notably, Bulgaria, Lithuania, and Czechia closely followed suit, with 10 funding rounds each.

Collectively, Poland, Estonia, and Romania attracted over 60% of investments this month (reaching nearly €90 million out of the €130 million invested in the region). This concentration highlights the limited dispersion of investor interest and capital, underscoring a cautious approach within the CEE startup ecosystem.

The most active investors were Vitosha Venture Partners, Spinaker Alfa, Baltic Sandbox Ventures, Credo Ventures, Feelsgood Capital, FundingBox Deep Tech Fund, N1, Specialist VC, and Startup Wise Guys. Endeavor, Gapminder VC, Hoxton Ventures, Karma Ventures, Smedvig Capital, TQ Ventures, and Verve Ventures are also worth distinguishing due to their participation in the biggest investment round this month (DRUID’s).

Despite the prevailing caution, sectoral preferences remained consistent, with investors continuing to focus on Artificial Intelligence, Cybersecurity, and Fintech.

Find out more: TOP CEE funding rounds closed in September.

Investment rounds in August

Number of funding rounds: 53

The biggest investment round: Bobnet - Venture Round - €18.4M, Wingbot - Seed - €8.2M, CUBE3.AI - Seed - €7.5M.

Total value of funding secured this in CEE: over €85M

Countries with most funding rounds: Poland - 10, Estonia - 9 rounds.

The most active VC funds: Hiventures

The most appreciated industries: AI, Cloud, SaaS, Fintech.

The venture capital landscape in August revealed a nuanced disposition characterized by subdued activity that mirrored an ongoing funding challenge. The total secured funding for the month surpassed €85 million, distributed across a modest count of 53 disclosed funding rounds. Regrettably, this marked August as the least dynamic month in terms of both total secured funding and the frequency of funding rounds.

Among the highlights of this relatively subdued phase were the investments into like Romanian Bobnet (Venture Round - €18.4M), Czech Wingbot (Seed - €8.2M), and Lithuanian CUBE3.AI (Seed - €7.5M). While these substantial investments added a glimmer of positivity, their impact was eclipsed by the prevailing backdrop of diminished funding fervor.

Geographically, the main points of funding activity remained consistent with the trends observed throughout the quarter, primarily in Poland and Estonia, securing 10 and 9 rounds, respectively. In an unexpected turn, despite participating in a lower number of funding rounds, Romania attracted the highest amount of investments for the month, exceeding €18 million.

Hiventures emerged as the most active investor in August, yet the cautious sentiment overshadowed the overall landscape. The spotlight of investor attention continued to focus on AI, Cloud, SaaS, and Fintech, aligning with the overarching enthusiasm for AI investments, albeit within the context of a more reserved investment environment.

NCH Capital merits distinction for its role in the largest investment round of the month (Bobnet’s).

In summary, August sustained the prevailing trend of stagnation within the venture capital ecosystem, marked by constrained funding dynamics and cautious investor behavior. Despite notable investments and the involvement of key players, the overall sentiment remained subdued, signaling a persistent and challenging landscape for startups seeking funding during this period.

Find out more: TOP CEE funding rounds closed in August.

Investment rounds in July

Number of funding rounds: 62

The biggest investment round: PV Case - Series B - €89M, SkeletonTechnologies - Venture Round - €50M, Preply - Series C (add-on) - €38.2M.

Total value of funding secured in CEE: over €300M

Countries with the most funding rounds: Poland - 12, Estonia - 10 rounds.

The most active VC fund: Presto Ventures

The most appreciated industries: Energy, Fintech, Biotech, AI.

July witnessed a surge in startup funding activity, marking the most substantial month in terms of total secured funding, with over €300 million secured across 62 disclosed funding rounds. Despite this apparent vigor, a closer examination reveals underlying challenges in the CEE startup ecosystem. Poland and Estonia emerged as the most active ecosystems, hosting 12 and 10 funding rounds, respectively, yet even their robust performance could not fully dispel the prevailing uncertainties.

The two countries collectively attracted over €180 million in funding, constituting approximately 60% of the total funding secured for the month. While seemingly positive, this concentration highlights the uneven distribution of funding and the challenges faced by startups in other parts of the region.

The largest funding rounds in July included Lithuanian PV Case (Series B - €89M), Estonian SkeletonTechnologies (Venture Round - €50M), and Ukrainian Preply (Series C (add-on) - €38.2M).

Investors exhibited a keen interest in sectors like Energy, Fintech, Biotech, and AI, while among most active investors this month in the CEE landscape was Presto Ventures.

Elephant, Energize Capital, Highland Europe are also worth distinguishing due to their participation in the biggest investment round this month (PV Case’s).

In summary, July showcased a semblance of activity within the startup funding landscape, marked by substantial funding rounds and concentrated successes in specific sectors. However, the nuanced challenges persisted, hinting at a more complex and challenging landscape for startups navigating the intricacies of funding in the CEE region.

Find out more: TOP CEE funding rounds closed in July.

Now let’s look closer at the Top 50 funding rounds closed in CEE between July and September 2023!

Top 50 CEE startup funding rounds closed in 3Q 2023:

- PV Case - is a leading solar design solution making solar project design faster, more efficient, and precise while solving the solar industry’s growing problem of data risk.

- Skeleton Technologies - is a cleantech that uses its own patented raw material, curved graphene, to produce tools such as supercapacitors and superbatteries.

- Preply- is an online tutoring platform, aiming to help students achieve their learning goals and prepare them to speak confidently.

- DRUID - is a conversational AI platform for enterprise companies that allows easy development of intelligent virtual assistants.

- hi - is a cross-ecosystem financial services platform through the world’s most popular social media messengers, such as WhatsApp and Telegram.

- Nibulon - is an agricultural enterprise that specializes in the production and export of grains such as wheat, barley, and corn.

- Geneplanet - is a biotechnology company, specializing in genetic testing and research (in preventive genetic tests in particular).

- Bobnet - is working on a series of hardware and software automation solutions, developed to overcome problems of implementing and managing large retail chains.

- Binalyze - is a DFIR platform to speed up cyber incident response and improve cyber resilience.

- KYP.ai - is a productivity and process mining platform.

- Dexory - captures real-time insights of warehouse operations using fully autonomous robots and Artificial Intelligence.

- Commsignia - specializes in the research and development, manufacturing and distribution of cooperative intelligent transportation systems.

- AI Clearing - is a full digital field construction progress tracking.

- Inuru - is a manufacturer of low cost OLED and OLED labels for packaging, medication and safety clothing.

- Continuum Industries - is a provider of an AI-powered infrastructure development platform for the energy sector.

- Rolla - help users track, compete, and have fun while working out, both outdoors and indoors.

- Monetizr - is an in-game ad experience platform that integrates brand stories at scale into mobile games.

- Stroom - DeFi startup developing a liquid staking protocol.

- Oasis Diagnostics - is a medical technology startup which is working to advance obstetrics care through the introduction of innovative diagnostics.

- Vool - is an EV charging solution that provides business and private customers with dependable, smart, and cost-effective charging.

- GoRamp - is a cloud-based Transportation Management Software, which helps shippers source, plan & monitor freight logistics.

- 57hours - is a marketplace connecting consumers with adventure guides for activities such as Rock climbing, backcountry skiing, hiking, and mountain biking trips.

- badu - is a fast growing ecommerce marketplace dedicated to improving intercontinental retail trade.

- Axoflow - is a platform that transforms on-premises and cloud logs, metrics, and traces into a cloud-native observability infrastructure.

- Formaloo - is a no-code collaboration platform that enables users to build custom business applications and tools.

- SATIM - provides insights based on satellite radar data acquired regardless of weather and day/night time.

- SharpGrid - is a data and technology business that is redefining on-trade and hospitality market research.

- Blockmate - is an open-crypto API platform which integrates and connects users' crypto data to a single unified API.

- Deskree - is a no-code back-end for any app in under 10 minutes.

- Avokaado - is a digital workspace for contract lifecycle management.

- DevSkiller - is a startup specialising in tech talent assessment and management solutions.

- Tuito - gives e-commerce shoppers straightforward insurance with a tempting offer.

- AIOT Cloud - is an innovative and affordable real-time energy monitoring and management solution.

- Access4you - is an app that offers surveys and assessment request audits for property owners and companies.

- Outfindo - is a SaaS solution driven by AI, designed to increase conversion rates by replicating the experience of a skilled and empathic expert.

- Spenfi - streamlines payment cards, expenses, subscriptions, and invoices with employees in an organized way.

- Fungies - is a SaaS platform to build Web Storefronts in the Gaming industry.

- Salespartner - is a customizable solution for the automotive industry that automates sales and approval processes, through modern interfaces, API, RPA, and AI.

- Swotzy - is a solution that streamlines last-mile operations for eCommerce, optimizing carrier selection to save on operational costs.

- Zibra AI - is a deep-tech company that utilizes Gen AI to expedite and simplify the creation of AI-generated assets.

- ReadyCode - is a SaaS solution that empowers game developers to integrate mod editors into their games at any development stage.

- BunnyShell - is an environment as a service platform simplifying the creation and management of full-stack environments for development, staging, and production.

- Prefixbox - is an AI-driven eCommerce site search solution, enhancing online revenue and conversion rates for eTailers.

- CupLOOP - is a reverse vending machine for reusable packages, integrating SaaS and Fintech to facilitate end-to-end tracking and management of reusable packages.

- KSM Vision - is an optical system for automated quality control in industrial applications, specializing in mechatronics and optical R&D services, with products designed for the healthcare industry.

- WeSky - is an in-seat power system that enhances in-flight experiences for airlines while improving operational efficiency by reducing fuel consumption.

- Ringil - is a logistics and transportation management solution that enables online tracking of data and KPIs.

- TrustLynx - is a solution supporting digital identity methods like e-signing, e-sealing, validation, and time-stamping, offering accessible tools for companies.

- Genus AI - is a gen AI platform that creates product catalog images, seed audiences, copy, and video to enhance growth across social media such as Facebook or Instagram

- ReCatalyst - is a solution focused on developing next-generation PEM fuel cell catalysts.

If you have some insights about the report, drop me a line!

Want to get a more detailed view of the CEE Startup & VC Ecosystem in 3Q 2023?

Discover our monthly, quarterly, and yearly reports:

- VC Transactions in CEE in 2022

- VC Transactions in CEE in 1Q 2022

- VC Transactions in CEE in 2Q 2022

- VC Transactions in CEE in 3Q 2022

- VC Transactions in CEE in 4Q 2022

- VC Transactions in CEE in 1Q 2023

- VC Transactions in CEE in 2Q 2023

- New VC Funds Investing in Europe - 3Q 2023

- TOP CEE funding rounds closed in July

- TOP CEE funding rounds closed in August

- TOP CEE funding rounds closed in September

Disclaimer: This report features VC rounds that have been publicly disclosed before the publication date or were shared by our VC and startup community. Grants and transactions below €50k were not considered. Furthermore, while we value all startups operating in CEE, our focus is on companies that originate from the region, self-identify as CEE companies, or have a significant presence of CEE founders.

Sources: Vestbee VC & startup community, startup press releases, web & social media monitoring, Crunchbase, PFR (Polish Development Fund).