Global VC Investments

The second quarter of 2023 marked a significant downturn in global venture capital investments, recording a drop of 18% from the previous quarter to settle at $65 billion, as corroborated by Crunchbase data. This decline is especially noticeable when compared to the funding in Q2 2022, where investors funneled an impressive $127 billion into startups, resulting in a significant 49% decrease.

The first quarter of 2023 was propped up by momentous investments in OpenAI ($10 billion) and Stripe ($6.5 billion). Accounting for these extraordinary deals in the Q1 statistics would paint a different picture - a remarkable 14% quarter-over-quarter rise in funding for Q2 2023, rather than the marked decrease it currently portrays.

While there has been a downturn in deal volumes in comparison to the previous year, the contraction isn't as steep as it is for funding amounts. Annually, deal volumes have shrunk by 37%, with each investment stage experiencing a drop of over a third. In the last quarter, over 6,000 startups managed to secure funding, marking a noticeable dip from the over 9,500 startups that achieved this during the same period in the prior year.

VC Investments in Europe

Drawing on the KPMG report's findings, it's clear that European investments followed a cautious approach, with $13.5 billion funneled into 1861 transactions. Echoing the global trend, the spotlight in Europe during Q2 2023 was squarely on AI and deep learning technologies. A case in point is the UK-based Quantexa, which garnered a substantial investment of $129 million during this period, thereby earning the prestigious unicorn status.

Even with dry powder at hand, VCs in Europe continue to exercise caution in their investment decisions. The current market dynamics and worries about future fundraising opportunities, compounded by the availability of more investment alternatives for less risk-averse Limited Partners, have contributed to this cautious stance. Additionally, it's projected that exit activity will be less vibrant, as both startups and investors opt for a more patient approach, awaiting better market sentiment.

VC Investments in CEE down to €560M

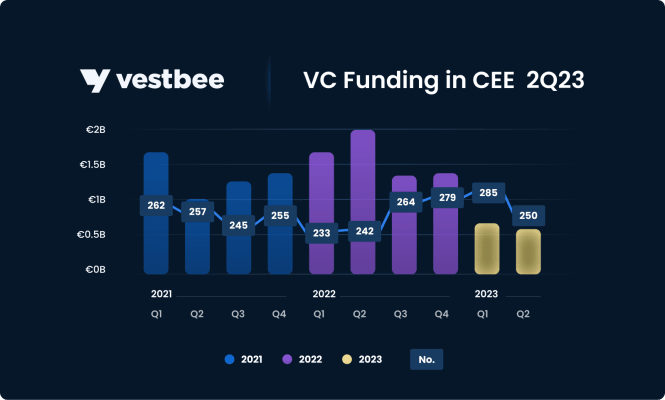

Investors' sentiment was not different in Central and Eastern Europe. During Q2 2023, venture capital investments in CEE experienced a minor decrease, with investments slightly surpassing €560 million, a slight drop from Q1 2023 when startups landed more than €600 million. This trend underlines a downward investment trend. The trajectory signals a noticeable deceleration in the CEE VC market, which is nowhere close to the resilience it showed back in H1 2022, and illustrates a slight misalignment between CEE and the Western markets.

Startup investment rounds in CEE in 2Q 2023

> Number of funding rounds: 250 (172 fully disclosed in terms of amount, month, investors, and company details)

> The biggest disclosed investment rounds: ID.me - Series D - €120M, FounderBeam - Venture Round - €36.8M, FLOWX - Series A - €32.2M, Sunly - Venture Round - €30M, IP Fabric - Series B - €21.1M, Hackajob - Series B - €23M, Woltair - Series A - €20.5M.

>Total value of funding closed in CEE: over €560M*

> Countries with the highest number of funding rounds: Poland - 116 rounds, Estonia - 29, Czechia - 20 rounds,

> The most active VC funds: Angel One, Coinvest Capital, Commerce Ventures, Eleven Ventures, FIRSTPICK, Gapminder VC, Hiventures, Lighthouse Ventures, Nation 1, Presto Ventures, Seedblink, SmartCap, Smok Ventures, SMRK VC, Sofia Angels Ventures, Specialist VC, Spinaker Alfa, Techstars, U.ventures, Venture to Future Fund, Vestman Energia, Vitosha Venture Partners, Y Combinator, ZAKA VC, Zero Gravity Capital

> The most popular industries: Cyber-security, AI, Energy, Enterprise Software, SaaS, Analytics.

*78 rounds undisclosed in terms of transaction value

When comparing the first quarter of 2022 with the corresponding period in 2023, we note a slight decrease in the number of funding rounds. However, a significant decline of over 72% in the total financing value has occurred. Specifically, the total financing value dropped from nearly €2B in Q2 2022 to €560M in Q2 2023. This decrease highlights the challenges that companies are encountering in securing substantial capital investments during this period. This decline can be attributed primarily to the current macroeconomic environment, characterized by increased uncertainty and reduced participation of foreign investors in CEE as well as reduced activity of public funds.

Furthermore, the absence of mega rounds continued in the second quarter. Only one such round was documented in Q2 2022, involving Estonian unicorn ID.me with a Series D round of €120 million. This, in addition to the decreased involvement of foreign investors, signals a potential shift in investor preferences and attitudes. Investors are increasingly embracing a strategy that focuses on diversifying risks.

If we delve deeper into historical data, specifically examining Q2 2021, a noteworthy observation emerges. The quantum of financing present in the market during this period bears a closer resemblance to the earlier part of 2021 rather than its counterpart in 2022. In Q2 2021, startups successfully amassed an impressive sum of nearly €1 billion in funding, significantly surpassing the €560 million recorded in Q2 2022. Remarkably, this surge in funding occurred against the backdrop of the ongoing pandemic, further emphasizing the resilience of the startup ecosystem.

It is evident that notwithstanding the existence of news about individual high-valuation funding rounds circulating in the market, there exists a discernible trend of overall market and startup valuations cooling down in 2023. This shift in sentiment is unmistakable, with investors adopting a more prudent and circumspect approach to their investment decisions. As we progress into the subsequent quarters of 2023, it is reasonable to anticipate that this cautious trend will persist.

Let’s have a closer look at what shaped the CEE ecosystem in Q2 2023.

During the second quarter of 2023, a total of 250 venture capital transactions were documented. This period exhibited a consistent distribution of deals, with a noteworthy 27% decrease in May (comprising 63 deals in June, 46 in May, and 63 in April), while the corresponding value remained relatively modest (surpassing €170 million in April, €130 million in May, and €220 million in June), as per the comprehensive disclosed data.

Among the biggest rounds disclosed in Q2 were secured by Estonian ID.me (Series D - €120M), Estonian FounderBeam (Venture Round - €36.8M), Romanian FLOWX (Series A - €32.2M), Estonian Sunly (Venture Round - €30M), Czech IP Fabric (Series B - €21.1M), Romanian Hackajob (Series B - €23M), Czech Woltair (Series A - €20.5M).

In the first quarter, Poland, Estonia Czechia and Romania accounted for 116, 29, 20 and 19 funding rounds, respectively. Notably, these countries also held a commanding presence in terms of investment volume, with Poland securing over €98M, Estonia amassing over €220M, Romania accumulating over €65M, and Czechia achieving over €60M.

The thematic focus of investment during this period unveiled a pronounced preference for sectors including Cyber-security, Artificial Intelligence (AI), Energy, Enterprise Software, Software as a Service (SaaS), and Analytics, while among the most active investors were Angel One, Coinvest Capital, Commerce Ventures, Eleven Ventures, FIRSTPICK, Gapminder VC, Hiventures, Lighthouse Ventures, Nation 1, Presto Ventures, Seedblink, SmartCap, Smok Ventures, SMRK VC, Sofia Angels Ventures, Specialist VC, Spinaker Alfa, Techstars, U.ventures, Venture to Future Fund, Vestman Energia, Vitosha Venture Partners, Y Combinator, ZAKA VC, Zero Gravity Capital.

Now, let's discover the note-worthy and recently raised VC funds from CEE.

New VC funds from CEE in 2Q 2023:

- Horizon Capital - secures $254M for its fourth growth fund to invest in Ukrainian/Moldovan growth-stage startups.

- Labena Ventures - a €100M fund established by slovenian pharma giant Labena to invest in biotech and health tech startups across CEE.

- The Polish Development Fund initiates a deep-tech-oriented Tech Hub. The fund will support startups by providing up to 50M PLN in funding.

Interested in other new VC Funds investing in CEE and Europe? Check out our article - recently raised VC funds from CEE and Europe.

Let's have a closer look at the Q2 results on a month-by-month basis. However, this review was solely based on fully disclosed rounds (name of startup, closing date, round’s size, participating investors).

Investment rounds in June

> Number of funding rounds: 63

> The biggest investment rounds: Sunly - Venture Round - €30M, IP Fabric - Series B - €21.1M, Woltair - Series A - €20.5M

> Total value of funding secured in CEE: over €220M

> Countries with the most funding rounds: Poland - 14, Estonia - 11 rounds.

> The most active VC funds: Venture to Future Fund, Vitosha Venture Partners

> The most appreciated industries: Energy, SaaS, AI, Cleantech.

In June, the amount of funding obtained by CEE startups exceeded €220M and was raised during 63 disclosed funding rounds. Poland led with its 14 investment rounds. Notably, Estonia and Czechia closely followed suit, with 11 and 10 startups respectively successfully securing funding.

Collectively, these three countries stood at the forefront of funding accomplishments, collectively amassing over €150 million in investments. This aggregate total represented a substantial 68% of the entire venture capital funding secured within the CEE region during that particular month, highlighting their dominance in attracting investor interest.

Among the most active investors were: Venture to Future Fund, and Vitosha Venture Partners.

In terms of sectoral preferences, the funding landscape exhibited a pronounced shift towards emerging industries with significant growth potential. Industries such as Energy, Software as a Service (SaaS), Artificial Intelligence (AI), and Cleantech garnered considerable attention from investors. This strategic redirection underscores the increasing alignment between investor sentiment and burgeoning sectors poised for transformative impact.

Find out more: TOP CEE funding rounds closed in June.

Investment rounds in May

> Number of funding rounds: 46

> The biggest investment round: FounderBeam - Venture Round - €36.8M, FLOWX - Series A - €32.2M, Hackajob - Series B - €23M.

> Total value of funding secured this in CEE: over €130M

> Countries with most funding rounds: Poland - 10, Czechia - 6 rounds, Bulgaria - 6 rounds.

> The most active VC funds: Eleven Ventures, SeedBlink, Venture to Future Fund.

> The most appreciated industries: Cloud, AI, SaaS, Analytics, Enterprise Software.

In the month of May, the venture capital landscape portrayed a nuanced demeanor, characterized by a subdued activity. The secured funding during this period reached a sum that surpassed €130 million, distributed across a modest tally of 46 disclosed funding rounds. This outcome unfortunately marked the least dynamic month in terms of both total secured funding and the frequency of funding rounds.

Among the highlights of this relatively subdued phase were the substantial investments garnered by key players: Estonian FounderBeam (Venture Round - €36.8M), Romanian FLOWX (Series A - €32.2M), and Romanian Hackajob (Series B - €23M). These sizable investments, while notable, were overshadowed by the prevailing backdrop of diminished funding fervor.

Geographically, main points of funding activity were observed in Poland, Bulgaria, and Czechia, gathering 10, 6, and 6 rounds respectively. In a twist, Romania and Estonia, while participating in a lower number of funding rounds, emerged as startup hubs in terms of funding accumulation, attracting over €55 million and over €40 million respectively.

Among the most active investors were Eleven Ventures, SeedBlink, Venture to Future Fund, while Cloud computing, Artificial Intelligence (AI), Software as a Service (SaaS), Analytics, and Enterprise Software commanded the spotlight of investor attention. This pointed focus aligns with the overarching aura of caution and discretion that characterized the month's venture capital narrative.

Find out more: TOP CEE funding rounds closed in May.

Investment rounds in April

> Number of funding rounds: 63

> The biggest investment round: ID.me - Series D - €120M, Fintech Farm - Series B - €20M, Oblivious - Series A - €6.3M.

> Total value of funding secured in CEE: over €170M

> Countries with the most funding rounds: Estonia - 15, Poland - 14 rounds.

> The most active VC fund: SMOK Ventures, Y Combinator, SeedBlink, Techstars, Zero Gravity Capital.

> The most appreciated industries: Cyber-Security, Fintech, Biotech, AI, Analytics.

In April, the startup funding landscape exhibited a somewhat subdued activity with a total of €170 million secured during 63 disclosed funding rounds. Notably, Estonia and Poland were the most active ecosystems, hosting 15 and 14 funding rounds, respectively. Among them, Estonia stood out by attracting over €125 million in funding, primarily due to a significant Series D round of €120 million secured by Estonian unicorn ID.me.

Besides Estonian ID.me, the largest funding rounds in April included Ukrainian Fintech Farm with a Series B funding of €20 million, and Polish-Irish Oblivious with a Series A funding of €6.3 million. Investors exhibited a keen interest in sectors like Cyber-Security, Fintech, Biotech, AI, and Analytics, as evident from their investment preferences.

Among most active investors this month in the CEE landscape were SMOK Ventures, Y Combinator, SeedBlink, Techstars, and Zero Gravity Capital, while most of investors’ interest was visible in the Cyber-Security, Fintech, Biotech, AI, and Analytics fields.

Find out more: TOP CEE funding rounds closed in April.

Now let’s have a closer look at the Top 50 funding rounds closed in CEE between April and June 2023!

Top 50 CEE startup funding rounds closed in 1Q 2023:

- ID.me is a digital identity network that aims to simplify the user's identity verification experience. It provides identity proofing, authentication, and group affiliation verification for organizations across sectors.

- Funderbeam is a tech-powered global marketplace that enables global investors to invest in companies and founders to handle their fundraising across borders.

- FlowX.ai created a platform enabling enterprises to effortlessly develop modern and intuitive web and mobile front-ends for critical business processes.

- Sunly is an Estonian independent power producer that builds solar and wind farms, which helps the current energy crisis.

- IP Fabrics develops an Automated Network Assurance Platform, ensuring network reliability and minimizing the risk of failures or outages.

- Hackajob is a two-sided marketplace that brings together technical candidates and companies looking for help, allowing tech professionals to learn new skills, participate in community events, and ultimately, find their next role. Companies are able to source talents, craft a compelling employer brand and conduct remote interviews.

- Woltair is a renewable energy company, working on expediting the adoption of heat pumps and renewable energy in the residential sector through a SaaS digital platform, increasing technician productivity.

- Fintech Farm is an Ukrainian-founded and UK based startup that creates digital banks in emerging markets.

- Eleven Labs researches novel methods in voice AI. The startup created a text to speech and voice cloning software allowing you to create lifelike voiceovers for your content.

- Resistant AI utilizes artificial intelligence and machine learning to develop solutions that safeguard AI systems against targeted manipulation, adversarial machine learning attacks, and advanced fraud.

- EnduroSat specializes in the design and engineering of spacecraft for business applications and space exploration missions. The company’s mission is to provide easy access to space for visionary entrepreneurs, scientists, and technologists, helping them fly their sensors to orbit fast and at a fixed cost.

- Oblivious’ technology maintains end-to-end payload encryption. While establishing a connection with the enclave, that is said to be a server with special super powers, the company facilitates the exchange of an attestation document, ensuring security and privacy.

- Sensoneo offers advanced smart waste management solutions tailored for businesses, facilitating the digital evolution of waste management processes.

- Turbine combines computer science and biology to simulate cell behavior and discover new ways to treat unexplored and unexplained cancers. The Simulated Cell platform enables identifying treatment options for the 70% of cancers that are currently unexplored.

- NewHomesMate is a marketplace enabling users to find, compare, and buy new construction homes.

- eAgronom is an agritech startup that supports farmers in adopting sustainable farming practices through monitoring and AI consulting platform. eAgronom guides farmers in implementing carbon-capturing methods.

- SuperScale is a revenue growth platform dedicated to mobile game developers and publishers. The platform empowers clients to identify strategies that increase revenue, as well as offers publishing and game management services.

- Instock is creating an as-a-Service 3D goods-to-person (G2P) system for eCommerce operations. Their technology addresses market demands with software-defined automation, simulation-first approach, and embedded self-service for day to day operations.

- Sensible Biotechnologies produces ty mRNA in a cost-effective and scalable manner, paving the way for the development of mRNA-based therapeutics and vaccines that promise to revolutionize the field of medicine.

- Vok Bikes develops electric cargo bikes with a payload of up to 200kg. The company’s bikes are rideable 24/7 thanks to its swappable batteries and a long maintenance cycle.

- Haiqu is a quantum computing software company that develops technology to improve the performance of modern quantum hardware, addressing the adoption obstacles that prevent scalable quantum applications from being realized

- Elmo introduces road-legal, remotely controlled vehicles. Elmo’s automobiles are now present on the streets of Tallinn and Tartu and have been subjected to testing and licensing procedures in different cities across the globe.

- Kende Retail Operation enables obtaining accurate information on product and customer shopping behaviors, creating a smart retail experience for global customers.

- Hedepy is a health application that offers video call-based psychotherapy to all, providing an accessible and user-friendly service.

- Nutrix developed gSense, AI first SaaS platform that uses high-tech devices, artificial intelligence and remote monitoring to provide assistance and monitoring for patients with chronic diseases, improving their quality of life and prolonging longevity.

- Value.Space is a tech firm utilizing satellites to perform evaluations for commercial properties and global infrastructure. This enhances risk assessment, identifies deformations, and helps to prevent disasters in space.

- Change is a FinTech company providing access to investments for everyone, offering a mobile solution for crypto and stock investing, cash management, and investor debit cards.

- Pluria offers a remote and hybrid work solution that enables companies to build teams and expand businesses across borders, all without the need for a fixed office space.

- Cytocast created a cellular health solution by integrating bioinformatics databases with patient data. Gathered information is used to create models, helping to predict how drugs modify cellular health.

- Product Fruits provides a comprehensive digital onboarding platform, designed to help businesses enhance user experience and simplify the client onboarding process, as well as to ensure users can quickly understand and navigate the products.

- NEXINEO is a virtualized computer system designed for schools. Each user is provided with only a monitor and a small virtual desktop device. This setup assists the teacher in classroom management. The required performance to support tens or even hundreds of units is delivered by a central server.

- Masthead Data ensures data reliability for Google BigQuery by using real-time anomaly detection through machine learning.

- Undelucram is a Romanian employee community platform. Job seekers access essential resources, including real reviews, while employees gain tools like the Salariometer for salary insights and a Student Guide for grads.

- Localazy is an AI-powered tool from Czechia, that helps developers, teams & businesses in the translation process of their applications.

- Amlyze’s transaction monitoring tool offers automated service designed for the financial sector and businesses seeking AML/CFT compliance. Each transaction is analyzed to ensure alignment with a customer’s risk profile.

- Zeely is a sales-growth mobile app, enabling users to grow their online sales with AI-powered ads, ad content and landing pages in minutes.

- CRUXO enables e-commerce players and retailers to gain visibility on the market, enhances retailer's revenues and profitability through its platform that combines data, targeting capabilities, and native ad formats.

- SoCyber is a cybersecurity startup that developed a vulnerability management solution, enabling companies to prioritize the remediation of vulnerabilities and address their security issues in a timely manner.

- Traxlo developed a solution that integrates into the daily operations of workers and retail store managers, simplifies tasks and enhances the shop-floor productivity and efficiency.

- Cupffee creates edible coffee cups and stirrers. Their manufacturing process stands out as it generates no industrial waste,while the cups are prepared with the usage of clean steam.

- Synaptiq.io is a software tool that separates cancerous tumors and organs at risk with the help of Artificial Intelligence. Synaptiq.io’s technology saves up to 95% of the time in contouring for radiotherapy.

- BioCam makes gastrology screening more accessible and convenient for every patient. BioCam designs and manufactures an endoscopic capsule for imaging of the digestive system along with AI-powered software.

- Hyperjob created a platform to support companies in attracting and hiring top-tier talent. Their platform enables recruiters to create modern, branded job ads that stand out from the crowd and convert better.

- Supply.Do is a one-stop shop, offering business printing services in addition to packaging, catalogs, direct mail, point-of-sale (POS), and helping to deliver goods for pharmacies, electronics, cosmetics, and automobiles.

- Profluo is a machine learning startup that builds a complete, ML-based technology to automate the processing of accounting documents.

- Liftero transforms space accessibility through the development of reusable spacecraft. Their first orbital transfer vehicle, Motus, will be the smallest vehicle available.

- OSavul is a tech company combating disinformation. It delivers software solutions designed to identify, evaluate, and counter disinformation threats posed by malicious entities.

- BuildJet’s Gaming CPU Cloud, plugged into GitHub Actions, allows developers to enjoy up to 2x faster speeds at significantly reduced costs, optimizing developers’ workflows.

- Proofminder is a farming platform that provides actionable insights to empower growers to achieve higher yields with fewer resources.

- Wope helps to convert marketing data into actionable insights. Wope, backed with AI, enables word-class SEO & content marketing service without human help.

If you have some insights about the report, feel free to drop me a line!

Want to get a more detailed view of the CEE Startup & VC Ecosystem in 2Q 2023?

Discover our monthly, quarterly, and yearly reports:

- VC Funding In CEE Report - 1Q 2023

- VC Transactions in CEE in 2022

- VC Transactions in CEE in 1Q 2022

- VC Transactions in CEE in 2Q 2022

- VC Transactions in CEE in 3Q 2022

- VC Transactions in CEE in 4Q 2022

- TOP CEE Funding Rounds Closed In May 2023

- TOP CEE Funding Rounds Closed In June 2023

- TOP CEE Funding Rounds Closed In July 2023

- New VC Funds Investing in Europe - 1Q 2023

Disclaimer: This report features VC rounds that have been publicly disclosed before the publication date, or were shared by our VC and startup community. Grants and transactions below €50k were not considered. Furthermore, while we value all startups operating in CEE, our focus is on companies that originate from the region, self-identify as CEE companies, or have a significant presence of CEE founders.

Sources: Vestbee VC & startup community, startup press releases, web & social media monitoring, Crunchbase, PFR (Polish Development Fund).