Accroding to the PitchBook The investment in European-based startups in 2022 exceeded €90B, indicating a YoY decline of more than 15% from the previous year. The main driver of this decline is the growing aversion to risk induced by slowing economy, inflation, higher interest rates and resulting increasing cost of capital. In the twilight of the zero interest rates many investors are more hesitant to allocate money into high risk – high return assets. For over a decade the VC market experienced a period of excessive optimism and inflated valuations, which ultimately led to a correction that currently unwinds in front of us.

Given the end of the era of cheap money and the resulting challenges, investors are becoming more interested in shielding themselves from market volatility. The end of 2022 showed that more and more investors started questioning the value and feasibility of the growth at all cost strategy, shifting their attention more into finding a balance between growth and profitability. Undoubtedly the market sentiment is changing and many investors are no longer willing to pay a premium just to be a part of a hyped round. Meanwhile, rising interest rates and the adjustment of startup valuations have forced out many casual investors, particularly those who were new to venture capital and entered the market when the cost of capital and risk were low.

2022 marked a significant turning point for European venture capital, indicating a beginning of a new era. How it is going to look is still to be seen as the amount of uncertainty is significant.

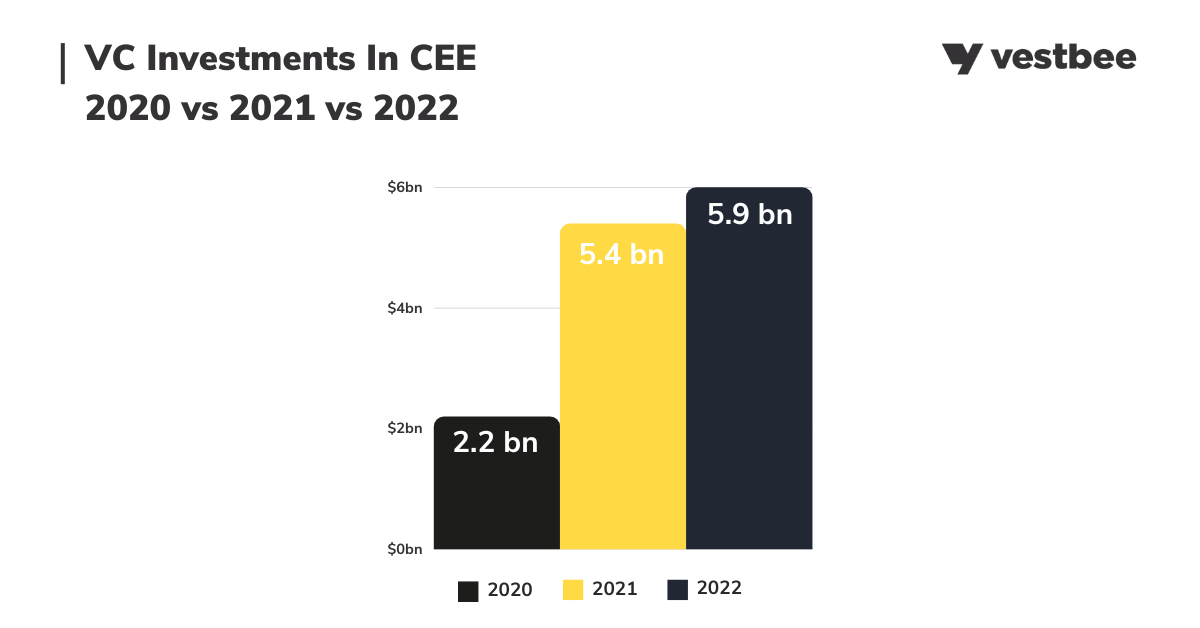

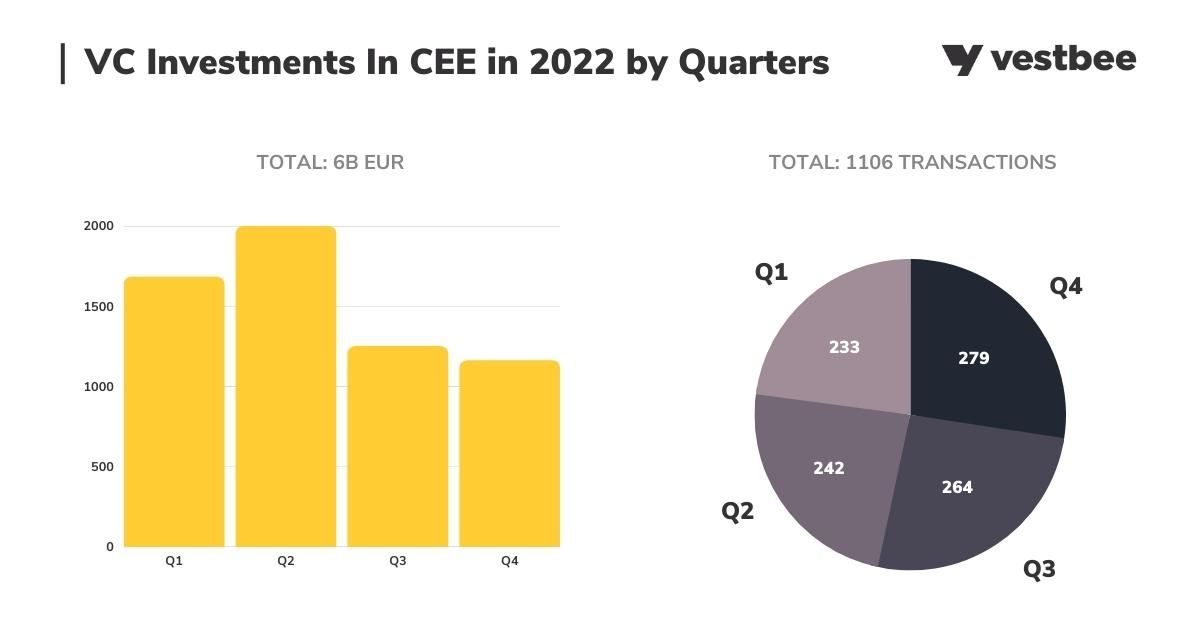

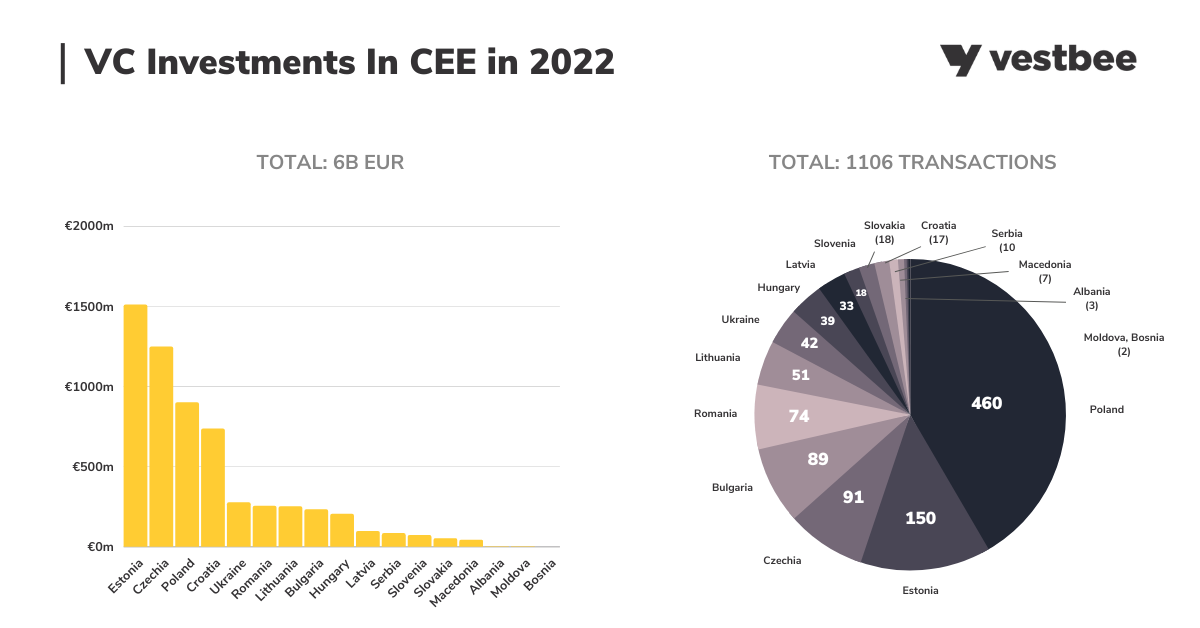

VC Investments in CEE in 2022 exceeded €5.9B

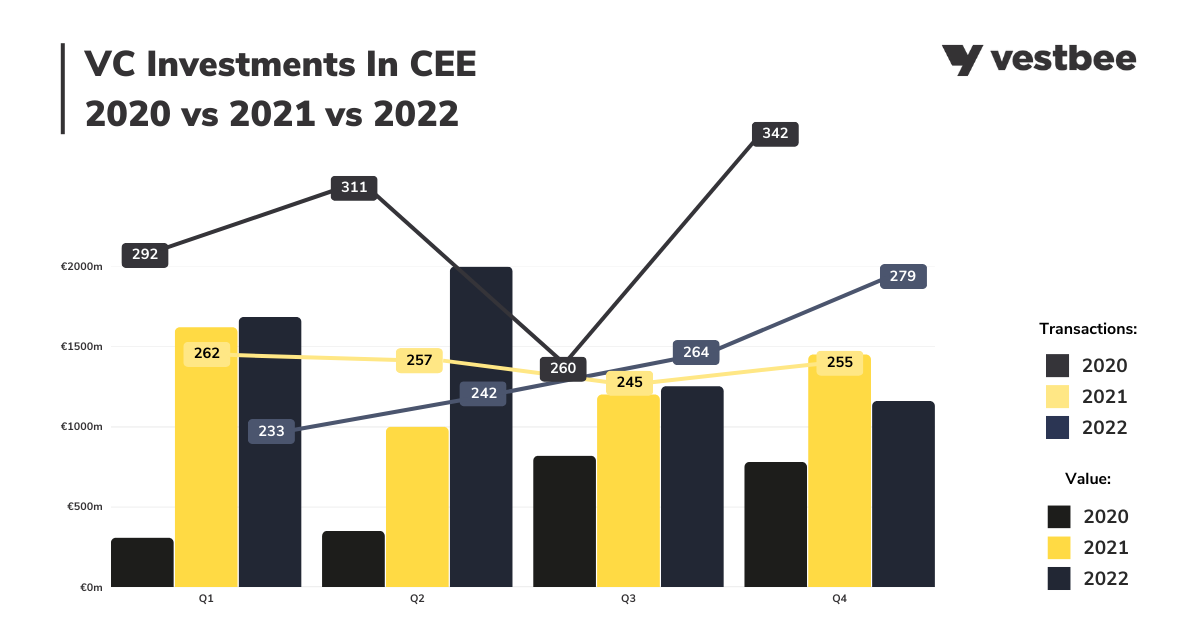

In 2022, the CEE ecosystem demonstrated resilience, surpassing €5.9B in deals and with over 1100 financial rounds taking place (a healthy 260% growth compared to 2020). The year 2021 proved to be a breakthrough, with the CEE region experiencing an exceptional increase in venture capital investment. Compared to the previous year, 2020, in which startups raised over €2.2 billion in more than 1,200 rounds, the total amount of investments year-on-year was doubled and the average round size almost tripled.

At a closer look however, it becomes visible that CEE is not an isolated island. Although VC investing was relatively strong, it slowed down in the second half of the year. There was a promising start to the year (startups secured over 1.6B EUR in 1Q, and over 2B EUR in 2Q) but deal value dropped significantly in 3Q, likely due to uncertainty fueled by the rising inflation.

Source: Vestbee, Crunchbase, surveys, community, web & media monitoring

The data shows that in 2021, the number of deals decreased throughout the year, while in 2022, it consistently increased. However, despite more transactions in 2022, the amount of funding allocated to them decreased, especially in Q3 and Q4. This could be due to investors trying to reduce risk in response to macroeconomic conditions. They may have invested in more companies but at smaller rounds to manage these challenges better.

Despite the decrease in the average deal size in 2022 as compared to the previous year, the fact that the total funding delivered to startups increased from 5.4 billion to almost 6 billion is a positive sign. Moreover, the data shows that mega rounds, defined as rounds of over 100 million dollars, still accounted for more than half of the total capital deployed.

All in all what we see in the data from 2021 and 2022 is a strong indication that the market is changing and investors are adjusting their strategies too. What 2023 will hold for the CEE’s startupland is very hard to predict. Nonetheless we are rather optimistic as the region has strong foundations and it was not over inflated as its older brother in the Western Europe.

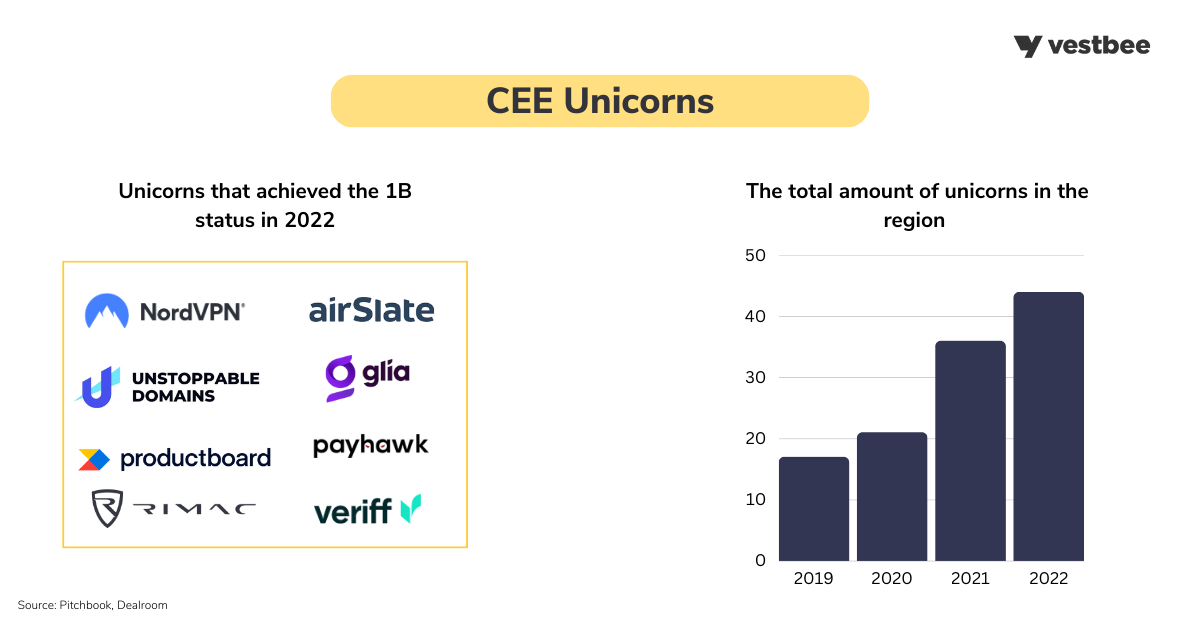

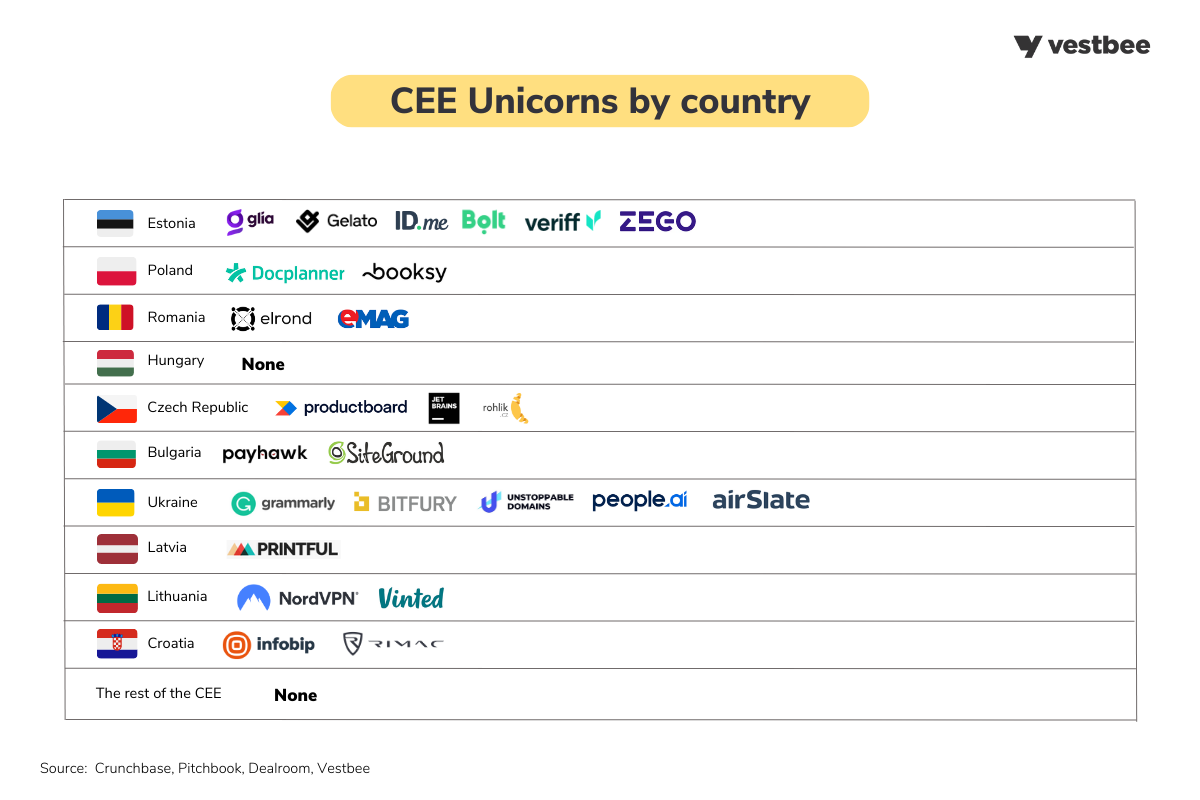

CEE Unicorns are on the rise

The CEE region has seen a significant increase in the number of new CEE unicorns, reflecting a positive trend in the ecosystem. Particularly strong years were 2021 and 2022, with more than half of the regional billion-dollar companies emerging in these two years alone. In 2021, 15 new unicorns emerged, followed by 8 in 2022, bringing the total number of unicorns to 44+ in 2022.

In 2022, the following companies from CEE reached a billion-dollar status:

Some of the most notable international investors with unicorns in their portfolios include:

- Index Ventures Productboard, Printify, and Rohlik),

- Accel (UiPath, Vinted, Veriff),

- Bessemer Venture Partners (Productboard, Pipedrive), -- Molten Ventures (Wise),

- Atomico (Pipedrive, Katana),

- Sequoia (Bolt, UiPath, Productboard),

- Insight Partners (Vinted, Pipedrive),

- Creandum (Bolt, Seon),

- Earlybird VC (UiPath, Payhawk).

Additionally, there are several noteworthy regional VC funds, such as:

- KAYA (Rohlik, Docplanner, and Booksy),

- Orbit Capital (Rohlik),

- Eleven Ventures (Payhawk),

- Inovo VC (Booksy),

- Credo (UiPath. Productboard),

- Superangel (Veriff).

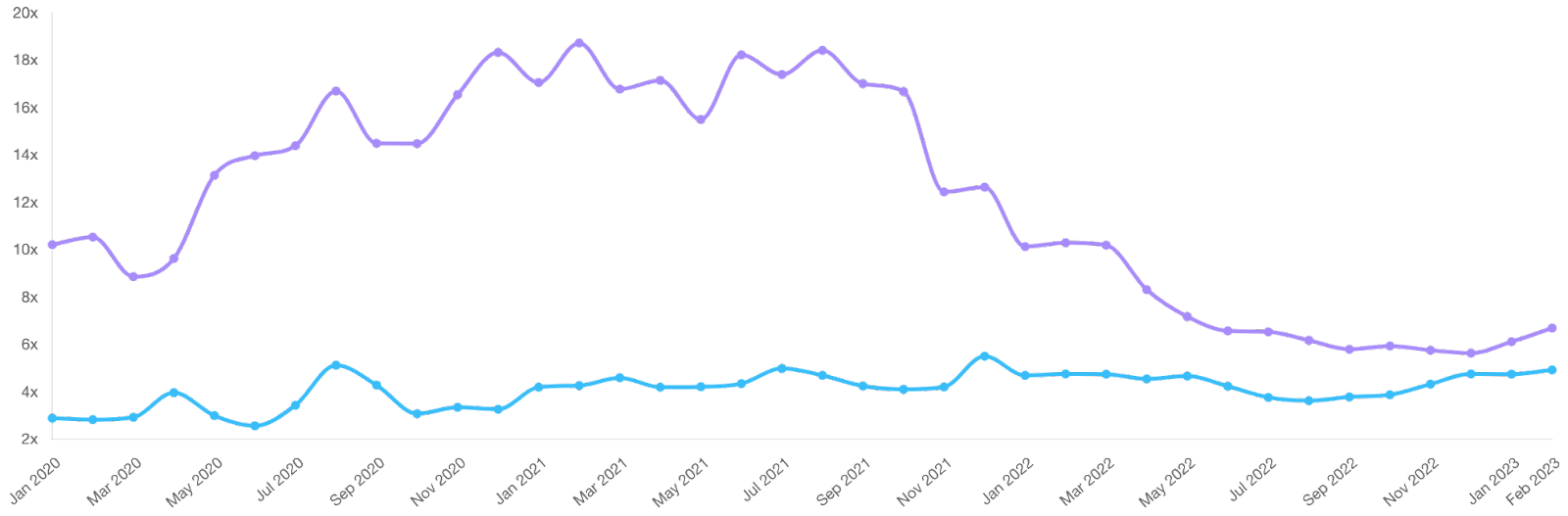

The drop in valuations

In 2022, for the first time since the 2008 financial crisis, Europe experienced falling startup valuations. The aftermath of COVID followed by the war in Ukraine with all its consequences have a significant impact on the economy, making investors increasingly cautious. The decline in valuations was particularly evident in the tech sector, where many companies were unable to meet or sustain their growth projections due to changing consumer behavior. Several major European tech companies also underwent significant staff layoffs. For example, Deliveroo announced a layoff of 2,000 employees, and Glovo laid off 25% of its workforce. These layoffs were a stark reminder of the fragility of hyper growth companies in a rapidly changing economic landscape. As a result, many investors became more risk-averse and embraced a more wait and see approach or redirected their capital into less risky and more liquid asset classes. This tendency is further reinforced by increasing interest rates and overall cost of capital. Startups are still able to raise by the valuations are nowhere near their historic heights of 2021.

As usual, the fluctuations on the global markets affect regional markets with a few months delay, and the CEE ecosystem is no exception. While the data for 2022 may not fully reflect the shift in valuations, signals from the first quarter of 2023 already suggest that the region is experiencing similar challenges to its western counterparts.

We expect that this will be also soon visible in the recently launched by Vestbee and Warsaw Equity Group CEE SaaS Index - a benchmark valuation tool for startups and investors based on revenue multiples from publicly traded SaaS companies residing in the CEE.

CEE vs US Revenue Multiple

Overall, the current situation serves as a reminder of the importance of resilience and adaptability in the face of economic uncertainty. This also applies to the CEE ecosystem, which although relatively nascent is not immune to the global volatility.

VC investments in CEE in 2022

Total value of VC funding in CEE: over €5.9B*

Number of funding rounds: 1106

The biggest disclosed investment rounds: Bolt - Series F - €628M, Rimac - Series D - €500M, Rohlik - Series D - €220M, Sunly - venture round - €200M, Mews - Series C - €185M

Countries with the most funding rounds: Poland - 460, Estonia - 150 rounds, Czech Republic - 91 rounds.

The most active VC funds: Startup Wise Guys, EBRD, LT Capital, Presto Ventures, Credo Ventures, EIC Fund, Movens Capital, Nation 1, Carlson ASI EVIG Alfa VC Fund, Depo Ventures, Early Game Ventures, Seedblink, Smok Ventures, Change Ventures, Inovo VC, J&T Ventures, Hiventures, Kaya, Vitosha Venture Partners, Next Road Ventures, Eleven Ventures, JR Holding, Miton, New Vision 3, Satus Starter, Speedup VC, Techstars.

The most appreciated industries: Artificial Intelligence, Financial Services, Energy, E-commerce, Cybersecurity, Healthcare, Analytics, Shared-services.

*154 rounds undisclosed in terms of the transaction value

Startups from certain countries in CEE have consistently performed better than others in terms of funding. In 2022, startups from Poland, Estonia, and the Czech Republic stood out, securing over €750M, €1.5B, and €1.1B, respectively. These countries have been leading the way in the CEE, mainly thanks to their well-established infrastructure, government support, and vibrant community of talented professionals. It is important to notice that the distribution of investments across the region is more even, as it was last year. This is a positive indication that the CEE startup ecosystem is diversifying and growing beyond the traditional top tier countries.

Below we present a comprehensive breakdown of investment rounds shown by quarters and countries. This insightful presentation of data effectively illustrates trends that have been previously identified within the CEE market in the year 2022. These trends include a decline in the total value of transactions within the second half of the year, coupled with a simultaneous, modest increase in the total number of transactions.

In recent years, venture capital investments in the Central and Eastern European (CEE) region have been steadily increasing, with Polish startups leading the way by securing over 41% of total funding rounds (460 out of 1106). Estonia, Czechia, and Bulgaria also stood out, with 150 (13,5%), 91 (8,2%), and 89 (8%) rounds respectively. It's worth mentioning that Bulgaria's performance was particularly impressive, given that this market has been somehow flying under the radar in the past.

It's important to notice that the majority of funding secured by Estonian and Czech startups came from mega-rounds raised by companies such as Bolt, and Rohlik. Bolt's €628M funding round was the largest investment round in the region, followed by Rimac's €500M round, Rohlik's €220M round, Sunly's €200M round, and Mews' €185M round.

Several investors stand out for their active investing and significant contributions to the CEE startup ecosystem's growth. These include Startup Wise Guys, EBRD, LT Capital, Presto Ventures, Credo Ventures, EIC Fund, Movens Capital, Nation 1, Carlson ASI EVIG Alfa VC Fund, Depo Ventures, Early Game Ventures, Seedblink, Smok Ventures, Change Ventures, Inovo VC, J&T Ventures, Hiventures, Kaya, Vitosha Venture Partners, Next Road Ventures, Eleven Ventures, JR Holding, Miton, New Vision 3, Satus Starter, Speedup VC, and Techstars.

Investors in the CEE region have shown particular interest in startups operating in areas such as artificial intelligence (AI), financial services, energy, e-commerce, cybersecurity, healthcare, analytics, and shared-services. These sectors are critical and rapidly evolving, making startups operating in those verticals highly attractive for investment.

Below, we present the quarterly overview of VC transactions in CEE.

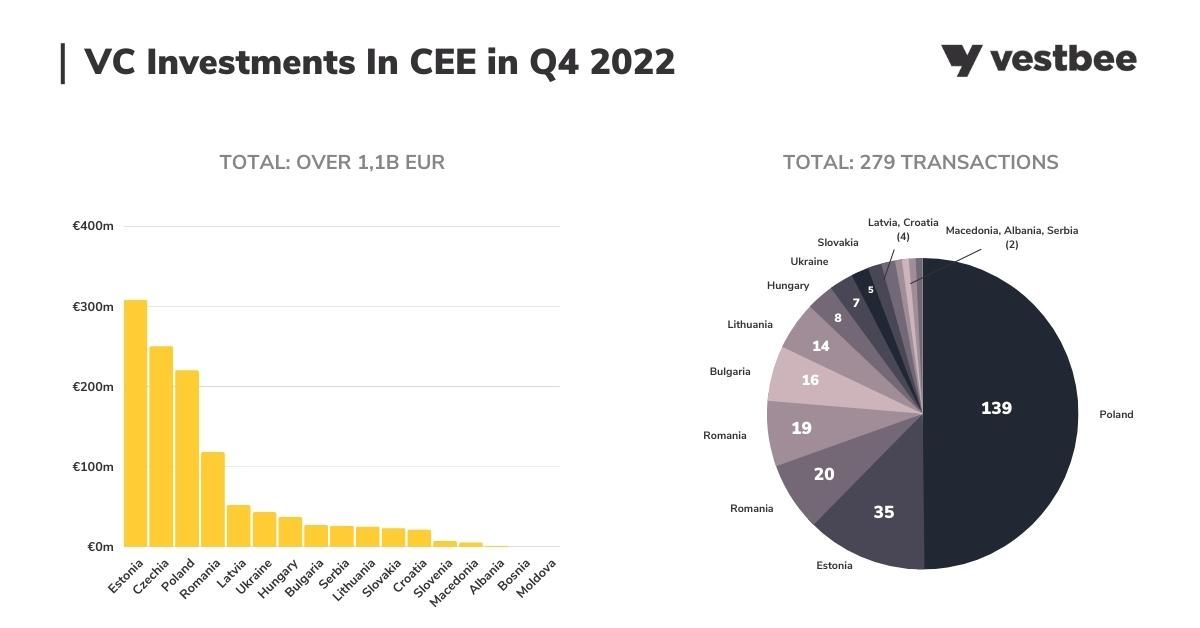

VC investments in CEE in Q4 2022

Total value of funding closed in CEE: over €1.1B*

Number of funding rounds: 279

The biggest disclosed investment rounds: Sunly - venture round - €200M, Mews - Series C - €185M, ZoidPay -venture round - €70M

Countries with most funding rounds: Poland - 139 rounds, Estonia - 35 rounds, Romania - 20 rounds

The most active VC funds: EBRD, InnovX, Depo Ventures, New Vision 3, Change Ventures, Eleven Ventures, Impetus Capital, Kaya, Nation 1, Presto Ventures, SFG Holding, Startup Wise Guys, Superhero Capital.

The most appreciated industries: Ecommerce, Energy, Finance, AI, and Analytics.

*90 rounds undisclosed in terms of the transaction value

During the fourth quarter of 2022, Central and Eastern Europe experienced a total of 279 investment rounds, with 189 with fully disclosing company details, funding amounts, dates, and participating investors. In terms of fully disclosed data, October had 64 funding rounds, while November and December had 67 and 58 respectively. During these three months, funding amounts remained at the 300-500M EUR level, with startups securing over €480M, €290M, and €390M, respectively, resulting in an overall investment value of over €1.1B.

Among the countries, Poland, Estonia, and Romania were the most active, securing 139, 35, and 20 investments, respectively. Notably, Poland's extensive VC ecosystem and active funds and private investors contributed to a significant number of investments compared to other countries. In terms of funding rounds, Estonian Sunly (€200M), Czech Mews (€185M), and Romanian ZoidPay (€70M) secured the most significant funding rounds.

The sectors that received the most funding were Ecommerce, Energy, Finance, AI, and Analytics, and the most active investors were EBRD, InnovX, Depo Ventures, New Vision 3, Change Ventures, Eleven Ventures, Impetus Capital, Kaya, Nation 1, Presto Ventures, SFG Holding, Startup Wise Guys and Superhero Capital.

VC investments in CEE in Q3 2022

Total value of funding closed in CEE: over €1.3B*

Number of funding rounds: 264

The biggest disclosed investment round: Cera - Venture Round - €150M (plus €150M in Venture Debt), Unstoppable Domains - Series A - €63M, Fonoa Technologies - Series B - €58M

Countries with the most funding rounds: Poland - 127, Estonia - 34, Ukraine - 19.

The most active VC funds: SATUS Starter, EBRD, EIC, Movens Capital, Presto Ventures, Endeavor, KAYA, LT Capital, Plural VC, Creandum, Eleven Ventures, Inventure, Smok Ventures, Next Road Ventures, Speedup Group

The most appreciated industries: Healthcare, Fintech, AI, Blockchain, SaaS, and Energy.

*69 rounds undisclosed in terms of the transaction value

In the third quarter of 2022, there was a noticeable deviation from the growth trajectory observed earlier in the year. The amount of capital deployed during this quarter was similar to that seen towards the end of 2020, despite a promising start to the year, with startups raising over 1.6B EUR in 1Q and over 2B EUR in 2Q. The discernible decline in deal value can be attributed to market-wide uncertainty due to the ongoing war in Ukraine, the pending energy crisis, rampant inflation, and the looming risk of a recession.

The Central and Eastern European market saw 264 VC transactions in Q3, with a relatively stable distribution of deals throughout the quarter. There were 75 deals in July, 54 in August, and 69 in September, with their value gradually decreasing over time. According to publicly disclosed data, deal value exceeded over €480M in July, over €340M in August, and over €300M in September. Notably, the average size of transactions decreased, and only one mega-round, the Czech-UK Cera - €150M Equity + €150M Debt, was recorded during the quarter.

Other significant rounds in Q3 were secured by Unstoppable Domains from Ukraine (Series A - €63M) and Croatian Fonoa Technologies (Series B round - €58M). Poland, Estonia, and Ukraine accounted for the most funding rounds, with 127, 34, and 19 deals, respectively. In terms of investment volume, the Czech Republic led the way with over €290M, followed closely by Estonia with over €260M and Ukraine with over €170M.

Healthcare, Fintech, Artificial Intelligence, Blockchain, SaaS, and Energy were among the most popular investment directions in Q3. Some of the most active investors in the region were SATUS Starter, EBRD, EIC, Movens Capital, Presto Ventures, Endeavor, KAYA, LT Capital, Plural, Creandum, Eleven Ventures, Inventure, Smok Ventures, Next Road Ventures and Speedup Group.

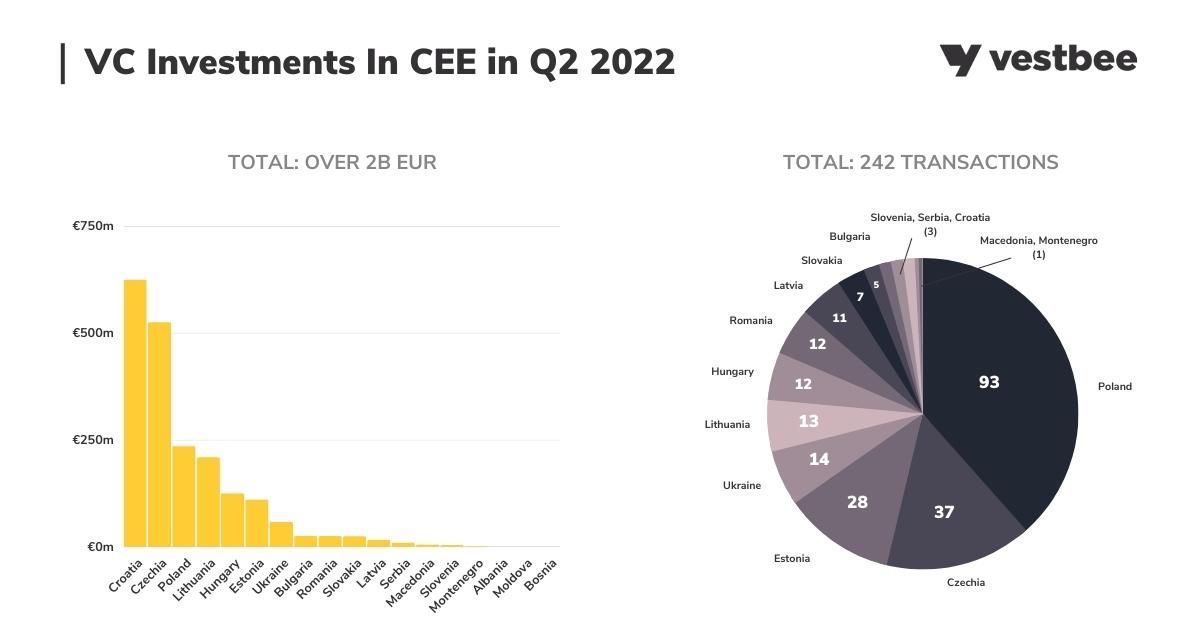

VC investments in CEE in Q2 2022

Total value of funding closed in CEE: over €2B*

Number of funding rounds: 242

The biggest disclosed investment rounds: Rimac Group - Series D - €500M (plus additional Venture Round €120M in April), Rohlik - Series D - €220M, Ataccama - Venture Round - €142M

Countries with most funding rounds: Poland - 93 rounds, Czech Republic - 37, Estonia - 28 rounds

The most active VC funds: Change Ventures, MITON, Geek Ventures, Hiventures, Movens Capital, Nation 1, Startup Wise Guys, Credo Ventures, DEPO Ventures, Early Game Ventures, EEC Ventures, Hoxton Ventures, Khosla Ventures, Presto Ventures, Purple Ventures, SMOK Ventures

The most appreciated industries: Automotive, Delivery Services, Fintech, E-commerce, AI, Analytics, SaaS, Data analytics.

*34 rounds undisclosed in terms of the transaction value

During 2Q of 2023, the VC and startup ecosystem in Central and Eastern Europe witnessed a consistent number of 242 VC transactions, with a slight upswing in May, wherein startups obtained more than 70 rounds compared to 60+ in April and June. In May, startups raised over €900M, with Croatian Rimac's €500M round significantly impacting the monthly data. Almost half of the total funding secured in the market for the quarter was attributed to mega-rounds worth over €100M. Additionally, round sizes continued to increase, signifying a gradual maturation of the regional market.

Croatian Rimac Group's €500M Series D round was the biggest disclosed investment round in 2Q 2023, followed by Czech Rohlik's €220M Series D round, and Czech Ataccama.

Poland, the Czech Republic, and Estonia were the most active countries in terms of funding rounds, with 93, 37, and 28 rounds, respectively. While Croatia led in investment volume with over €620M, the Czech Republic followed closely with over €540M. Polish and Lithuanian startups also attracted significant investor attention, raising over €230M and €200M, respectively.

The Automotive, Delivery Services, and E-commerce sectors were the most popular among investors, while Financial Services, AI, and Data & Analytics remained in the investment circle.

Notable investors who remained highly active during the second quarter included Change Ventures, MITON, Geek Ventures, Hiventures, Movens Capital, Nation 1, Startup Wise Guys, Credo Ventures, DEPO Ventures, Early Game Ventures, EEC Ventures, Hoxton Ventures, Khosla Ventures, Presto Ventures, Purple Ventures, and SMOK Ventures.

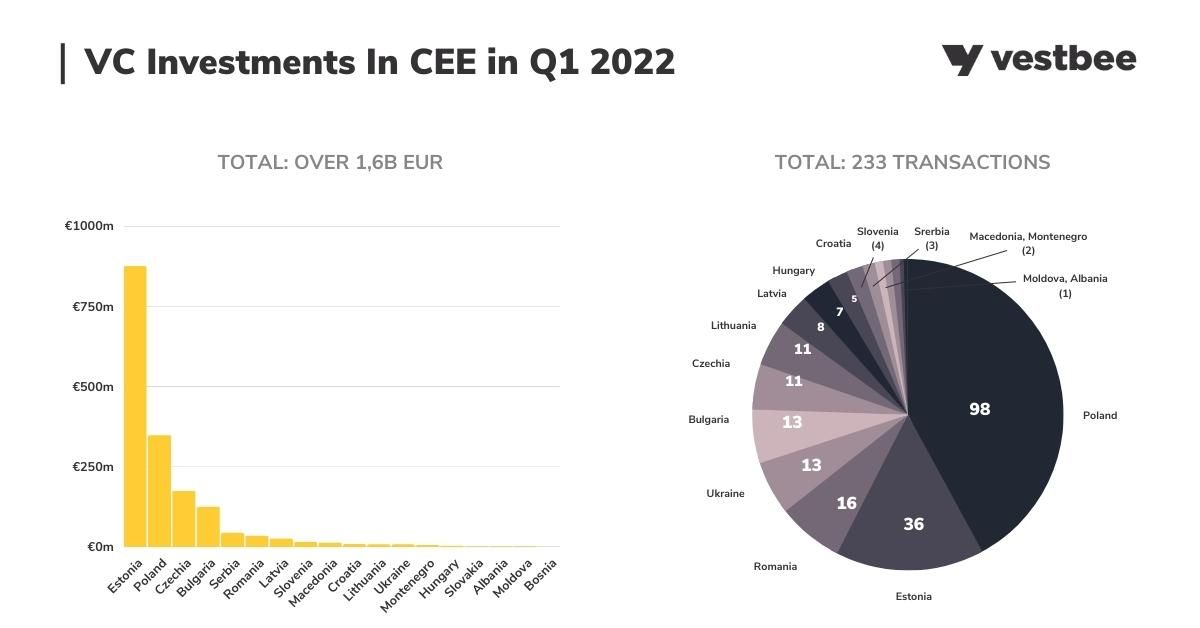

VC investments in CEE in Q1 2022

Total value of funding closed in CEE: over €1.6B*

Number of funding rounds: 233

The biggest disclosed investment rounds: Bolt - Series F - €628M, ICEYE - Series D - €120M, ProductBoard - Series D - €110M

Countries with most funding rounds: Poland - 98, Estonia - 36, Romania - 16

The most active VC funds: Startup Wise Guys, Early Game Ventures, Karma Ventures, Presto Ventures, Specialist VC (United Angels VC), Credo Ventures, Vitosha Venture Partners, Inovo Venture Partners, Accel, Earlybird Venture Capital.

The most appreciated industries: Ecommerce, Fintech, Analytics, AI, SaaS, Advertising, Big Data.

*36 rounds undisclosed in terms of the transaction value

During the first quarter of 2022, 233 investment rounds took place in Central and Eastern Europe, with only 170 fully disclosed in terms of funding amount, company details, date, and participating investors. January witnessed 63 funding rounds, followed by 62 in February and 43 in March. While the immediate impact of the Russian invasion of Ukraine and the significant depreciation of public tech stocks was not yet predictable at the time, uncertainty surrounding current macroeconomic conditions and the potential slowdown was palpable in the CEE startup landscape, leading to more GPs adopting a bearish stance.

In terms of funding rounds, Poland, Estonia, and Romania led the pack with 98, 36, and 16, respectively, while Poland, Estonia, and the Czech Republic recorded the highest total investments exceeding €250M, €920M, and €160M, respectively. Additionally, Lithuania and Bulgaria also attracted significant funding rounds, while entrepreneurs in Ukraine were able to secure 13 funding rounds, demonstrating their resilience despite ongoing conflict.

The largest disclosed investment rounds were secured by Estonian Bolt (Series F - €628M), Polish/Finnish ICEYE (Series D - €120M), and Czech Productboard (Series D - €110M), with the finance, Data & Analytics, and AI sectors attracting the most funds.

Startup Wise Guys, Early Game Ventures, Karma Ventures, Presto Ventures, Specialist VC (United Angels VC), Credo Ventures, Vitosha Venture Partners, Inovo Venture Partners, Accel, and Earlybird Venture Capital were among the most active investors in financing rounds.

Now that we have analyzed the VC transactions from 2022 and their impact on the CEE market, to stay ahead of the curve and make informed decisions we recommend checking our 2023 forecast.

Now, after already analysing VC transactions in 2022 and how they shaped the whole CEE market, if you are interested in further CEE startup & VC scene development we recommend you to take a look at the VC trends in 2023 (general) and VC trends in 2023 (cleantech & impact) forecasts.

Hall Of Fame - Meet The TOP CEE Funding Rounds Closed In 2022!

The year 2022 was remarkable in terms of the number of investment rounds and their cumulative deal value and below we share some of the most interesting ones.

- Rimac Automobili - founded in 2009, is a Croatian automotive and technology company that specializes in the development of high-performance electric vehicles (EVs) and related technologies. Rimac secured a series D round in the amount of €500M from Goldman Sachs, Ischyros New York, Porsche, and SoftBank Vision Fund.

- Bolt - Estonia-based, Bolt is a transportation platform providing ride-hailing services. Bolt also offers scooter and bike-sharing services, as well as food delivery services in select markets. Bolt aims to offer more affordable prices for riders while also providing better earnings for drivers compared to its competitors. Bolt secured a series F round of €628M from D1 Capital Partners, Fidelity Management and Research Company, G Squared, Ghisallo Partners, Owl Rock Capital, Sequoia Capital, Tekne Capital, and Whale Rock Capital Management.

- Rohlik - Czech grocery service that offers online grocery shopping and delivery services. Rohlik offers a wide range of grocery products, including fresh produce, meat, dairy, and bakery items, as well as non-perishable goods and household items. Rohlik has secured a series D round in the amount of €220M from Index Ventures, ORBIT Capital,and Sofina.

- Sunly - is an Estonian independent power producer that builds solar and wind farms, which helps the current energy crisis. Company has recently secured a funding round in the amount of €200M from Mirova to build and expand its renewable energy portfolio.

- Mews - Czech hospitality startup which provides a cloud-based hotel property management platform with tools covering reservations, payments and more. Company has recently secured a round of €185M from Revaia, Derive Ventures, Orbit Capital, Thayer Ventures, Salesforce Ventures, Notion Capital, henQ, Battery Ventures, Kinnevik, Goldman Sachs.

- Cera - Czech-UK Cera is a home healthcare company that uses digital solutions to provide better and more affordable care for elderly and vulnerable patients. Cera empowers patients to receive the care they need in the comfort of their own homes. Cera has recently secured a €150M equity round (+150M debt) from Kairos HQ, alongside the Vanderbilt University Endowment, Schroders Capital, Jane Street Capital, Yabeo Capital, Squarepoint Capital, Guinness Asset Management, Oltre Impact, 8090 Partners.

- Ataccama - Czech unified data management and governance technology developer that creates tools for working with data. Startup has recently secured a €142M round from Bain Capital Tech, Opportunities,

- ICEYE - Polish startup that is transforming satellite imaging with its innovative synthetic-aperture radar satellite constellation. This advanced technology provides monitoring capabilities for any location on earth, revolutionizing the way we observe and gather data about our planet. ICEYE has secured a €120M round from Seraphim Space, BAE Systems, Kajima Ventures.

- Productboard - Czech product management system is an innovative solution that helps organizations streamline their product development processes and bring products to market more quickly and efficiently. Productb has secured €110M series D round from Sequoia Capital, Kleiner Perkins, Index Ventures, Credo Ventures, Bessemer Venture Partners.

- Nord Security - Lithuanian cybersecurity startup with a mission is to build a radically better internet and restore trust in digital networks, by securing consumer and enterprise accounts, networks and information against advanced cyberthreats. Company secured a venture round in the amount of €95M from Burda Principal Investments, General Catalyst, and Novator.

- SEON - Hungarian-UK cybersecurity startup that creates fraud prevention tools to help organisations reduce the costs and resources lost to fraud. The company raised a Series B round in the amount of €89M round from Creandum, IVP, and PortfoLion Capital Partners.

- Veriff - Estonian global online identity verification company that enables organizations to build trust with their customers through intelligent, accurate, and automated online IDV (identity verification). The startup secured a series C round in the amount of €89M from Accel, Alkeon Capital, Institutional Venture Partners, Tiger Global Management

- Payhawk - Bulgarian spend management software that allows customers to save time and money, manage spend, and scale business quicker and cheaper. Payhawk has secured a Series B round in the amount of €89M from QED Investors, Sprints Capital, Jigsaw VC, HubSpot Ventures, Greenoaks Capital, Endeavor Catalyst, Earlybird Venture Capital.

- ZoidPay - Romanian crypto liquidity platform enabling instant card issuance for purchases at any merchant. The startup secured a €73M funding round from GEM Digital.

- Ramp - Polish cryptocurrency payment-infrastructure startup building a crypto payments infrastructure that allows users to easily exchange fiat currency for cryptocurrencies. Ramp secured a Series B round in the amount of €70M from Balderton Capital, Cogito Capital Partners, Korelya Capital, Mubadala Capital Ventures.

*If you have some insights or feedback regarding our report, drop me a line!

Disclaimer: This report features VC rounds that have been publicly disclosed before the publication date, or were shared by our VC and startup community. Grants and transactions below €50k were not considered. Furthermore, while we value all startups operating in CEE, our focus is on companies that originate from the region, self-identify as CEE companies, or have a significant presence of CEE founders.

Sources: Vestbee VC & startup community, startup press releases, web & social media monitoring, Crunchbase, PFR (Polish Development Fund).

Related Posts:

VC And Startup Trends 2023: Cleantech, Energy, Greentech, Impact Investing (by Olga Chechłacz, Editor, Vestbee)

CEE Unicorns: The Rise Of Startup Ecosystem In Central & Eastern Europe (by Katarzyna Groszkowska, Editor, Vestbee)

VC Trends Shaping CEE Startup Ecosystem In 2023 (by Olga Chechłacz, Editor, Vestbee)