Key takeaways

- Global venture funding reached $113 billion in Q1 2025 — its strongest performance since mid-2022 — but this was largely driven by OpenAI’s record-breaking $40 billion raise. Stripping out that single deal, global investment levels were flat year-over-year and down quarter-over-quarter. The quarter highlighted a clear shift toward late-stage and AI-focused investments, while early-stage and seed funding continued to decline. With over half of all VC dollars going to AI, the sector has firmly cemented its dominance, though this growing capital concentration is widening the gap between mature companies and emerging startups.

- Venture funding in Europe held steady at $12.6 billion in Q1 2025, showing no significant change from previous quarters, but reflecting continued resilience compared to pre-pandemic levels. Despite this stability, Europe’s share of global venture capital fell to 11%, driven by massive funding activity elsewhere, particularly in the US. Healthcare, biotech, and AI were the leading sectors, while the UK remained the continent’s dominant market. Strong early- and growth-stage activity signals investor confidence, though overall momentum is tempered by increasing concentration of capital in select regions (like UK and Gemany) and sectors (AI, biotech).

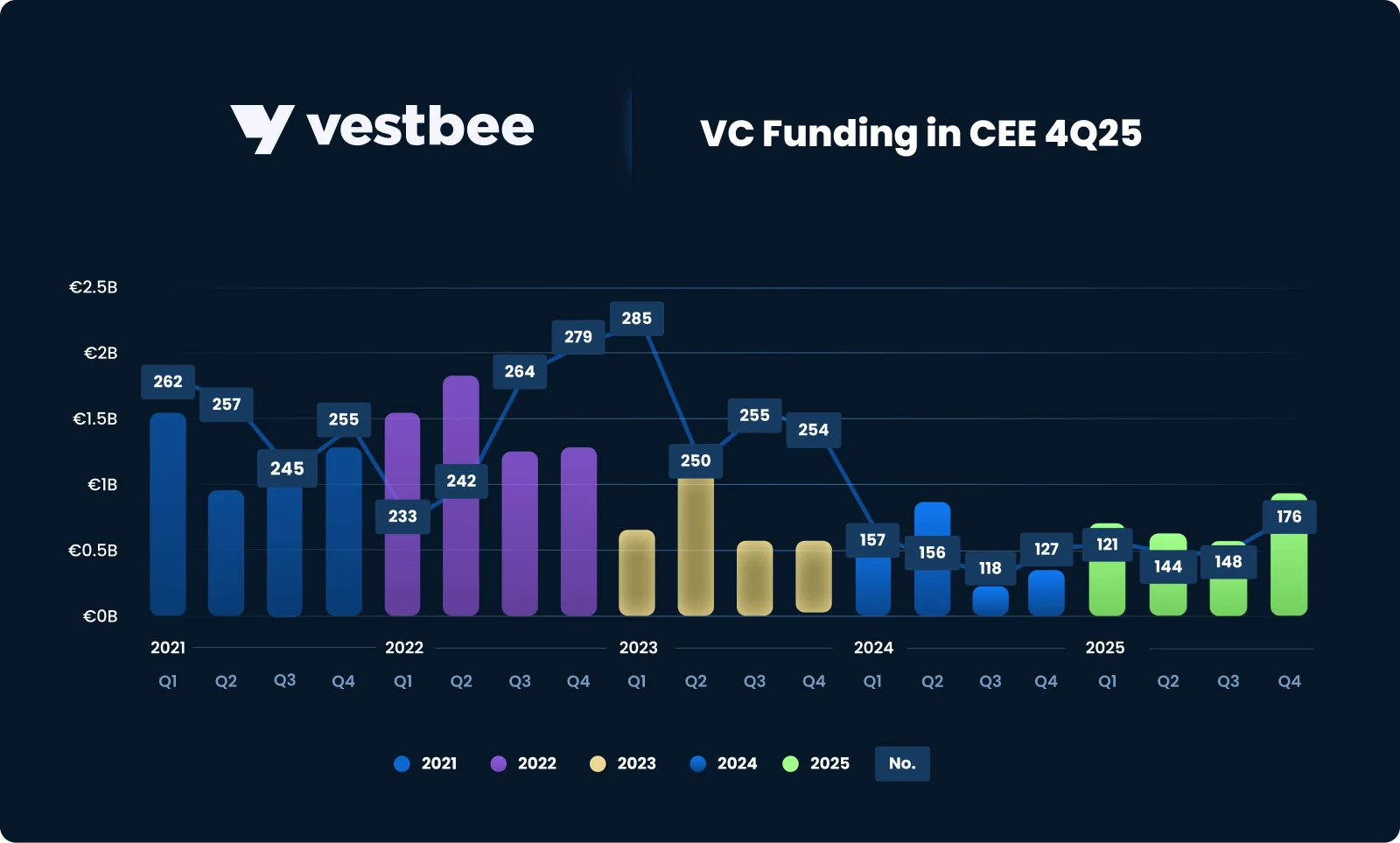

- Venture funding in Central and Eastern Europe (CEE) showed signs of fragility in Q1 2025, with deal volume down 23% year-over-year and underlying capital deployment declining. The contraction reflects both global macroeconomic pressures and structural limitations within the region’s investment landscape, including cautious international participation and constrained local fund activity. Yet, despite these headwinds, the region’s enterprise value continues to climb, reaching €243 billion — a testament to the ecosystem’s underlying potential. To sustain this momentum, CEE will require renewed investor confidence, stronger local funding capacity, and a clearer path to exits to avoid a prolonged capital gap and risk of innovation stagnation.

Global venture capital trends: a late-stage rebound driven by AI

Aside from a single substantial funding round totaling $113 billion—the highest quarterly sum since mid-2022—the first quarter of 2025 otherwise marked a flat period for global venture capital activity. This apparent surge was heavily influenced by a single transaction: OpenAI’s landmark $40 billion round, which alone accounted for more than one-third of all capital deployed in the quarter. Without this record-setting raise, global venture funding would have remained relatively flat compared to the same period last year and declined modestly from Q4 2024, according to Crunchbase data.

OpenAI’s round not only set a new record as the largest private market deal in history but also propelled the company to a $300 billion valuation, placing it second only to SpaceX among the world’s most valuable private startups. This event highlights the growing role of megadeals in shaping the global funding landscape and their capacity to skew broader trendlines.

Excluding such outliers, a deeper look reveals diverging dynamics across stages. Late-stage investment led the quarter’s growth, surging over 30% quarter-over-quarter and rising by 147% year-over-year to reach $81 billion. In stark contrast, early-stage funding contracted significantly, falling to $24 billion — the lowest level recorded in over a year. Seed-stage investment followed a similar trajectory, declining 14% year over year to $7.2 billion. It is worth noting, however, that seed data is often revised upward as additional rounds are disclosed post-quarter.

AI remained the dominant theme in global VC, with the sector attracting nearly $60 billion in funding — more than half of all capital raised in Q1. While OpenAI alone comprised a substantial portion of that figure, the broader enthusiasm around AI innovation continues to command investor attention and capital allocation at an unprecedented scale. The first quarter of 2025 now stands as the strongest period ever recorded for AI-related venture investment, solidifying the sector's position as the primary engine of global funding activity.

This continued concentration of capital into late-stage and AI-driven investments suggests a growing polarization within the venture landscape: while mature startups with clear market traction continue to raise large rounds, younger companies are increasingly facing tighter capital constraints and longer fundraising cycles.

Venture capital in Europe: a stabilized landscape amid global shifts

In the first quarter of 2025, venture capital activity across Europe remained stable, with total funding reaching $12.6 billion, according to Crunchbase. This figure represents no significant movement from either the previous quarter or the same period last year, indicating a period of relative steadiness following the volatility seen since the downturn began in 2022. While the quarterly total sits within the post-downturn range — fluctuating between slightly over $10 billion and $16 billion over the past year — it is clear that Europe's venture ecosystem has grown meaningfully compared to pre-pandemic benchmarks. Both 2023 and 2024 exceeded the funding volumes recorded in 2020 and prior years, signaling a more mature and resilient startup landscape despite ongoing global uncertainty.

However, Europe’s relative share of global venture capital declined in Q1, accounting for just 11% of worldwide funding — a significant drop from 16% in 2024. This shift is primarily attributed to large-scale capital deployment in other markets, particularly North America. A single, unprecedented transaction — OpenAI’s $40 billion raise — notably skewed global distribution and underscores the growing influence of mega-rounds in shaping regional dynamics.

From a sectoral perspective, health and life sciences led the way, capturing $4 billion in investment, or approximately one-third of all European VC funding in Q1. Financial services and artificial intelligence were also prominent, attracting $2.8 billion and $2.7 billion respectively. This sectoral distribution reflects enduring investor interest in innovation-driven verticals, particularly those aligned with long-term macroeconomic trends such as digital health and next-generation AI applications.

The UK maintained its status as Europe’s dominant venture market, with domestic startups raising an estimated $4.4 billion in Q1. Germany and France followed, securing $1.6 billion and $1.3 billion respectively. Notably, Spain emerged as a strong performer this quarter, with local startups raising $1 billion — the country’s first quarter crossing this threshold in over two years.

Across stages, growth and early-stage companies each attracted over $5 billion in capital, illustrating continued investor confidence in backing innovations across various development stages. Growth-stage deals accounted for approximately $5.6 billion across more than 80 transactions, while early-stage rounds totaled $5.4 billion across over 280 deals. Meanwhile, seed-stage activity remained robust with $1.6 billion invested across 850 rounds, a figure likely to be revised upward as additional data becomes available.

Several large financings defined the quarter’s landscape, including London-based Isomorphic Labs ($600 million) and Rapyd ($500 million), as well as high-profile biotech investments such as Verdiva Bio ($411 million) and Windward Bio ($200 million). Late-stage rounds outside the UK included Berlin-based Amboss ($259 million) and Barcelona-based TravelPerk ($200 million), pointing to the geographic diversity and cross-border strength of Europe's innovation ecosystem.

VC investment trends in CEE

Central and Eastern Europe: funding volatility amid ecosystem maturity

In the first quarter of 2025, CEE experienced a nuanced venture capital lanscape. Total funding reached €700 million, representing a 9% increase compared to Q1 2024. However, this uptick is primarily attributed to a significant €170 million Series C round by ElevenLabs, an AI voice startup founded by Polish entrepreneurs but headquartered in the US. Excluding this outlier, the region's funding would have declined to €530 million, indicating a 17% year-over-year decrease. Furthermore, the number of funding rounds dropped from 157 in Q1 2024 to 121 in Q1 2025, marking a 23% decline according to Dealroom.

The funding contraction in CEE can be attributed to a convergence of structural and cyclical factors. On the macroeconomic front, persistent inflationary pressures, tighter monetary policy, and geopolitical uncertainties — have heightened investor risk aversion across emerging markets. International funds, once key drivers of capital inflows into the region, have increasingly shifted their focus toward larger, more mature ecosystems perceived as more stable and immediately scalable. Meanwhile, domestic investors are grappling with capital constraints, limited fund replenishment, and a more selective approach to follow-on investments. Regulatory uncertainties and a still-developing exit environment further temper confidence. This retreat from both global and local capital sources has widened the funding gap, making it particularly difficult for early- and late-stage startups to secure the resources necessary for growth and market expansion.

Despite these challenges, the CEE startup ecosystem demonstrates significant resilience and growth. As of Q1 2025, the region's combined enterprise value reached €243 billion, a substantial increase of 35% from €180 billion in 2020. This growth trajectory underscores the region's maturation and its potential to bridge the gap with Western European counterparts.

However, sustaining this momentum requires renewed investor confidence and strategic capital deployment. Startups in the region are facing longer fundraising cycles, increased scrutiny, and more stringent deal terms. Without a resurgence in investment activity, there is a risk of innovation stagnation and a widening gap between CEE and more mature ecosystems.

Startup investment rounds in CEE in Q1 2025

- Number of funding rounds: 121 (110 fully disclosed in terms of date and funding amount).

- The biggest disclosed investment rounds: ElevenLabs, a €170M Series C, Mews, a €66M venture round, Blackwall, a €45M Series B

- Total value of funding closed in CEE: over €700M* (total value includes Polish-founded but US-based ElevenLabs)

- Countries with the highest number of funding rounds: Poland — 36 rounds, Estonia — 18, Czechia — 17 rounds

- The most active VC funds: J&T Ventures , Interactive Venture Partners, SMOK VC, Day One Capital, Inovo VC, Tera Ventures, Radix Ventures, Underline Ventures, bValue Fund, Impact Ventures, EBRD VC, Catalyst Romania, Lighthouse Ventures, Simpact Ventures, Tensor Ventures, Coinvest Capital, Startup Wise Guys, SmartCap, FIRSTPICK

- The most popular industries: AI, healtech, biotech, financial services, SaaS.

*20 rounds undisclosed in terms of transaction value & outlier (ElevenLabs was included there as well)

What shaped the CEE ecosystem in Q1 2025

In the first quarter of 2025, the CEE venture capital landscape saw a total of 121 funding rounds, with deal activity remaining relatively stable across the quarter — 34 in January, 40 in February, and 36 in March. While the volume of transactions reflected cautious investor sentiment, consistency in monthly activity suggests a base level of resilience within the region’s startup ecosystem.

Among the largest publicly disclosed deals were the €170 million Series C round raised by Polish-founded, US-headquartered ElevenLabs; a €66 million venture round by Mews, a Czech-founded (Netherlands-based) hospitality tech company; and Estonian Blackwall’s €45 million Series B. These rounds not only drove a significant share of capital raised in the region, but also demonstrated the ongoing trend of CEE-founded startups increasingly operating out of or incorporating in Western Europe or the US to access larger funding pools and bigger markets.

Geographically, Poland, Estonia, and Czechia emerged as the region’s most active markets, recording 36, 18, and 17 transactions respectively. Together, these three countries accounted for nearly 60% of all deals and approximately 70% of total capital raised in Q1, reaffirming their status as the primary hubs for venture activity in CEE. Their relative maturity, stronger founder talent pipelines, and growing base of repeat entrepreneurs continue to attract both domestic and international investor attention.

In terms of sector focus, investor appetite in the region mirrored broader European and global patterns, with pronounced interest in AI, healthtech, biotech, financial services, and SaaS. This aligns with pan-European data, where health and life sciences led venture activity, drawing $4 billion in Q1 funding — roughly one-third of total European VC investment. The convergence of sectoral interest signals a growing integration of CEE innovation into broader continental investment theses, particularly in capital-intensive and deep tech verticals.

Now, let's discover the note-worthy and recently raised VC funds from CEE.

New VC funds from CEE in 1Q 2025:

- Prague-based Soulmates Ventures has raised a €50 million fund to support sustainable startups, investing under Article 9 of the SFDR. The fund aims to invest up to €3 million per startup, with follow-up funding reaching €5 million.

Interested in other new VC funds investing in CEE and Europe? Check out our article New VC Funds Investing in Europe — 1Q 2025.

Let's take a closer look at the Q1 results on a month-by-month basis. However, this review was solely based on fully disclosed rounds (name of startup, closing date, round’s size, participating investors).

Investment rounds in March

- Number of funding rounds: 36

- The biggest investment rounds: Mews, a €66M venture round, Greenway, €50M venture round, Blackwall, €45M Series B

- Total value of funding secured in CEE: over €255M

- Countries with the most funding rounds: Poland — 8, Estonia — 8

- The most active VC funds: Inovo VC, Tera, Coinvest Capital

- The most appreciated industries: AI, hospitality, cybersecurity

In March 2025, startups across CEE secured over €255 million in funding across 36 publicly disclosed rounds. Poland and Estonia led in terms of transaction volume, each recording eight deals, while Czechia emerged as the top performer by total capital raised — largely driven by Mews’ €66 million funding round.

Notably, March’s elevated funding volume — the highest monthly total in Q1 — was heavily skewed by a handful of landmark deals. In addition to Mews, significant contributions came from Greenway (€50 million) and Blackwall (€45 million). Together, these three transactions accounted for a substantial share of the capital deployed during the month. When excluded, the overall funding volume would appear considerably more subdued, highlighting the outsized influence of mega-deals in shaping monthly investment metrics.

Sector-wise, activity in March was concentrated in AI, hospitality, and cybersecurity, aligning with both regional strengths and global investment trends. Prominent investors this month included regional players such as Inovo VC, Tera Ventures, and Coinvest Capital, all of which continued to demonstrate commitment to the local ecosystem. Additionally, global funds including Tiger Global Management, Battery Ventures, Kinnevik, and Goldman Sachs Alternatives played a key role — particularly in headline deals like Mews — reaffirming the strategic appeal of select CEE startups for international capital.

Overall, the data reinforces a familiar dynamic within CEE: while standout rounds can temporarily boost aggregate funding levels, the underlying contraction in deal flow raises concerns about the long-term vibrancy of the ecosystem. Sustained innovation and growth will require more consistent support across all stages of the startup lifecycle, not just isolated injections of capital into breakout companies.

Find out more: TOP CEE funding rounds closed in March.

Investment rounds in February

- Number of funding rounds: 40

- The biggest investment round: Nomagic, a €31.5M Series A, Atrandi, a €22.1M Series A, Bible Chat, a €14M Series A

- Total value of funding secured this in CEE: over €176M

- Countries with most funding rounds: Poland — 9, Czech Republic — 7 rounds

- The most active VC funds: Underline Ventures

- The most appreciated industries: robotics, AI, biotech, IT

February 2025 emerged as the most active month of the first quarter in CEE in terms of deal volume, with 40 publicly disclosed funding rounds. The total capital raised slightly surpassed €176 million, reflecting continued — albeit uneven — investor engagement across the region. Noteworthy transactions included a €31.5 million Series A round into Polish robotics startup Nomagic, along with significant early-stage raises by Lithuania’s Atrandi (€22.1 million) and Romania’s Bible Chat (€14 million).

Poland and Czechia led the month’s activity both in volume and value, recording 9 and 7 deals respectively and jointly accounting for more than €87 million — nearly half of February’s total funding. This sustained activity reinforces their status as key innovation hubs within the broader CEE startup landscape, drawing consistent interest from regional and international investors alike.

On the investor front, Underline Ventures emerged as the most active player in February, participating in multiple deals across the region. Meanwhile, institutional and global funds such as EBRD, Khosla Ventures, and Almaz Capital contributed to some of the largest rounds this month, underscoring a growing willingness among select international players to back high-potential ventures in the region. Sectorally, funding remained concentrated in robotics, AI, biotech, and IT — verticals that continue to attract capital due to their scalability and alignment with long-term innovation trends.

While February delivered promising signs of regional momentum, the underlying data also reflects a cautious investment climate. Deal sizes remained concentrated in a handful of standout rounds, while broader early-stage activity appeared restrained. To build a more resilient ecosystem, the CEE region will require not only headline-grabbing investments but also sustained funding across the venture lifecycle — especially for early-stage startups that form the foundation of future growth.

Find out more: TOP CEE funding rounds closed in February.

Investment rounds in January

- Number of funding rounds: 34

- The biggest investment round: ElevenLabs, a €170M Series C round, ThreatMark, a €13.2M venture round, Fudosecurity, a €9M venture round

- Total value of funding secured in CEE: over €266M

- Countries with the most funding rounds: Poland — 8 rounds, Czech Republic — 6 rounds

- The most active VC fund: Interactive Venture Partners, SMOK VC, Radix Ventures, SmartCap

- The most appreciated industries: Fintech, Security, AI, SaaS.

In January 2025, startups across CEE raised over €266 million across 34 publicly disclosed funding rounds, making it the strongest month of the first quarter in terms of capital raised. However, this headline figure is disproportionately influenced by the €170 million Series C round secured by ElevenLabs — an AI voice startup founded by Polish entrepreneurs but now headquartered in the US. When excluding this outlier, the month’s total drops significantly to under €70 million, revealing a much more subdued funding environment.

Poland and Czechia led regional activity with 8 and 6 funding rounds, respectively, though overall deal flow remained muted by historical standards. Compared to January 2024, the number of deals fell by over 38%, underlining the ongoing contraction in venture activity as investors continue to exercise caution amid a challenging macroeconomic backdrop.

Beyond ElevenLabs, few sizable deals stood out. Czech cybersecurity firm ThreatMark secured €13.2 million in a venture round, while Polish-American SaaS company Fudo Security raised €9 million. These three transactions alone accounted for over 70% of the capital raised in January, illustrating the current reliance on large, high-profile rounds to sustain monthly totals in a sluggish market.

Sectorally, investor interest gravitated toward fintech, cybersecurity, AI, and SaaS — areas aligned with broader European and global VC trends. Among the most active investors were Interactive Venture Partners, SMOK Ventures, Radix Ventures, and Estonia’s SmartCap, which maintained a visible presence in the region despite the broader pullback in funding.

This data underscores a persistent challenge for the CEE startup ecosystem: while landmark deals continue to draw attention and demonstrate the region’s potential to produce globally relevant ventures, the underlying deal flow remains thin. The heavy concentration of funding into a few transactions suggests growing polarization in the market, where only the most mature or high-profile startups are able to secure meaningful capital. Without a broader resurgence in early- and growth-stage investing, particularly from both local and international funds, the ecosystem risks losing momentum at its foundational levels.

Find out more: TOP CEE funding rounds closed in January.

Now let’s look closer at the top 50 funding rounds closed in CEE between January and March 2025.

Top 50 CEE startup funding rounds closed in Q1 2025:

- Mews is a Czech-founded unicorn, a hospitality tech company that helps hotels manage operations and enhance guest experiences

- Blackwall is a cybersecurity company offering both mitigation and web security solutions for hosting and managed services.

- JutroMedical is an AI-first primary care provider integrating online and offline care.

- Stargate Hydrogen is a greentech startup specializing in electrolyzer development.

- Splx AI develops an AI security platform designed to address the risks associated with AI and LLM technologies

- Intelliseq specializes in the automated analysis and interpretation of human genome variations.

- Frankenburg Technologies specializes in rocket science and produces missiles for air defence.

- Cino offers shared payments via a single virtual card.

- Qneiform helps users find their ideal recruit.

- ArtMaster is a firm specializing in music education.

- Fleetbrains leverages AI to revolutionize fleet sales and stock management.

- ENGYcell provides personalized energy storage solutions to reduce energy costs and gain energy independence.

- Nomagic provides smart pick-and-place robotic solutions for order fulfilment. Its solutions automate tedious tasks while reducing fulfilment costs, allowing warehouses to face labour shortages and scale to 24/7 operations.

- Atrandi Biosciences develops Semi-Permeable Capsule (SPC) technology, which enables high-throughput experiments while keeping each cell separate.

- Bible Chat develops AI-powered solutions for Christian communities. These solutions offer users personalized, biblically grounded support, prayer assistance, and 24/7 guidance.

- Whalebone develops advanced, user-centric cybersecurity solutions for telecommunications providers, ISPs, enterprises, governments, and public institutions.

- Wealthon provides integrated financial solutions for small and medium-sized businesses.

- Bethink offers an e-learning product that combines technology, educational publishing, and direct learning experiences.

- Trace.Space is a robotics and automation company specializing in autonomous inventory management.

- Crown is a B2B procurement technology company that simplifies buying with its online auction platform.

- Pulsetto is a healthtech startup that specializes in vagus nerve stimulation for stress relief, mental resilience, and sleep optimization.

- Pointship develops a digital asset marketplace that allows users to manage, exchange, and utilize assets like loyalty rewards, game credits, and event tickets.

- grid.online offers a shared transportation network for parcel delivery through an API-driven platform that connects clients with flexible, efficient capacity.

- CulturePulse develops ARES, an AI-powered behavioural and psychological digital twin that allows users to test content for audience resonance before launching it live.

- GaltTec develops microtubular solid oxide fuel cells (MT-SOFCs). These cells provide high power density, durability, and flexibility, which makes them ideal for drones, IoT devices, off-grid equipment, and space applications.

- Edmund develops AI-powered solutions designed to simplify manufacturing troubleshooting and maintenance processes.

- ElevenLabs is an AI audio research and deployment company that develops advanced text-to-speech technology tailored for publishers and creators.

- ThreatMark offers a machine learning-based platform designed to protect financial institutions from evolving digital fraud.

- nexos.ai develops an AI orchestration platform that enables enterprises to integrate, manage, and optimize multiple AI models.

- Axoflow offers an automated security data curation platform that simplifies data management by eliminating the need for manual, code-heavy wrangling.

- Safetica Technologies is a cybersecurity company that protects sensitive data and prevents internal security threats.

- Ongeno is developing a therapy that, in the first phase of trials, has been shown to improve the health of sclerosis patients, reduce disability, and prevent disease progression over the long term.

- Wultra develops easy-to-deploy post-quantum authentication solutions designed specifically for financial institutions.

- Gridio is a smart energy platform designed to optimize electric vehicle charging. It automatically charges EVs during the cheapest and cleanest energy periods, requiring no additional hardware.

- Kodesage offers an AI-powered platform that helps enterprises modernize and manage complex legacy software systems.

- Letsdata uses AI to detect and prevent information operations (InfoOps), including manipulation and synthetic identities, across platforms like X, Telegram, Facebook, Instagram, and TikTok.

- Naco Technologies develops nano-coatings to replace expensive metals in hydrogen production.

- Outfindo is an AI-driven platform that simplifies the online shopping experience by guiding customers to the right products.

- Wonder Legends Studio develops transmedia projects, including video games and animated series, using Unreal Engine to create immersive and narratively rich worlds.

- Readmio provides a new way to read fairy tales by using voice recognition and sound effects to engage children.

- Elcogen offers three products for emission-free power and hydrogen production.

- Gridraven develops AI-driven software designed to optimize electricity grid capacity without the need for additional infrastructure.

- Yope is a mobile application that records real-time video of the user and their interaction with any content on their smartphone and the world around them.

- Prosoma is redefining mental health care in oncology through digital innovation.

- Commody is a collectible car platform enabling enthusiasts to co-own exclusive vehicles and potentially profit from value changes.

- Soldera helps renewable energy producers earn extra income by automating energy certificate trading, simplifying the process and maximizing profits.

- Fudo Security is a privileged Access Management solution ensuring secure remote connections and active monitoring for critical resources.

- .lumen builds Spatial Navigation AI shown in the Glasses for the Blind.

- Griselda is an automated system of input, processing and transmitting information using artificial intelligence.

- Fastlane Labs is MEV-aware infrastructure and smart contracts to make DeFi usable and keep it decentralized.

If you have some insights about the report, drop me a line!

Want to get a more detailed view of the CEE startup & VC ecosystem in Q1 2025? Discover our monthly, quarterly, and yearly reports:

- VC Transactions in CEE in 1Q 2024

- Central and Eastern European Startups Report 2025

- New VC Funds Investing in Europe — 1Q 2025

- TOP CEE funding rounds closed in January

- TOP CEE funding rounds closed in February

- TOP CEE funding rounds closed in March

Disclaimer: This report features VC rounds that have been publicly disclosed before the publication date or were shared by our VC and startup community. Grants, debt funding and transactions below €50,000 were not considered. Furthermore, while we value all startups operating in CEE, our focus is on companies that originate from the region, self-identify as CEE companies, or have a significant presence of CEE founders.

Sources: Vestbee VC & startup community, startup press releases, open data from web & social media sources, PFR’s (Polish Development Fund) reports, DaaS platforms such as Crunchbase and Dealroom.