Key takeaways

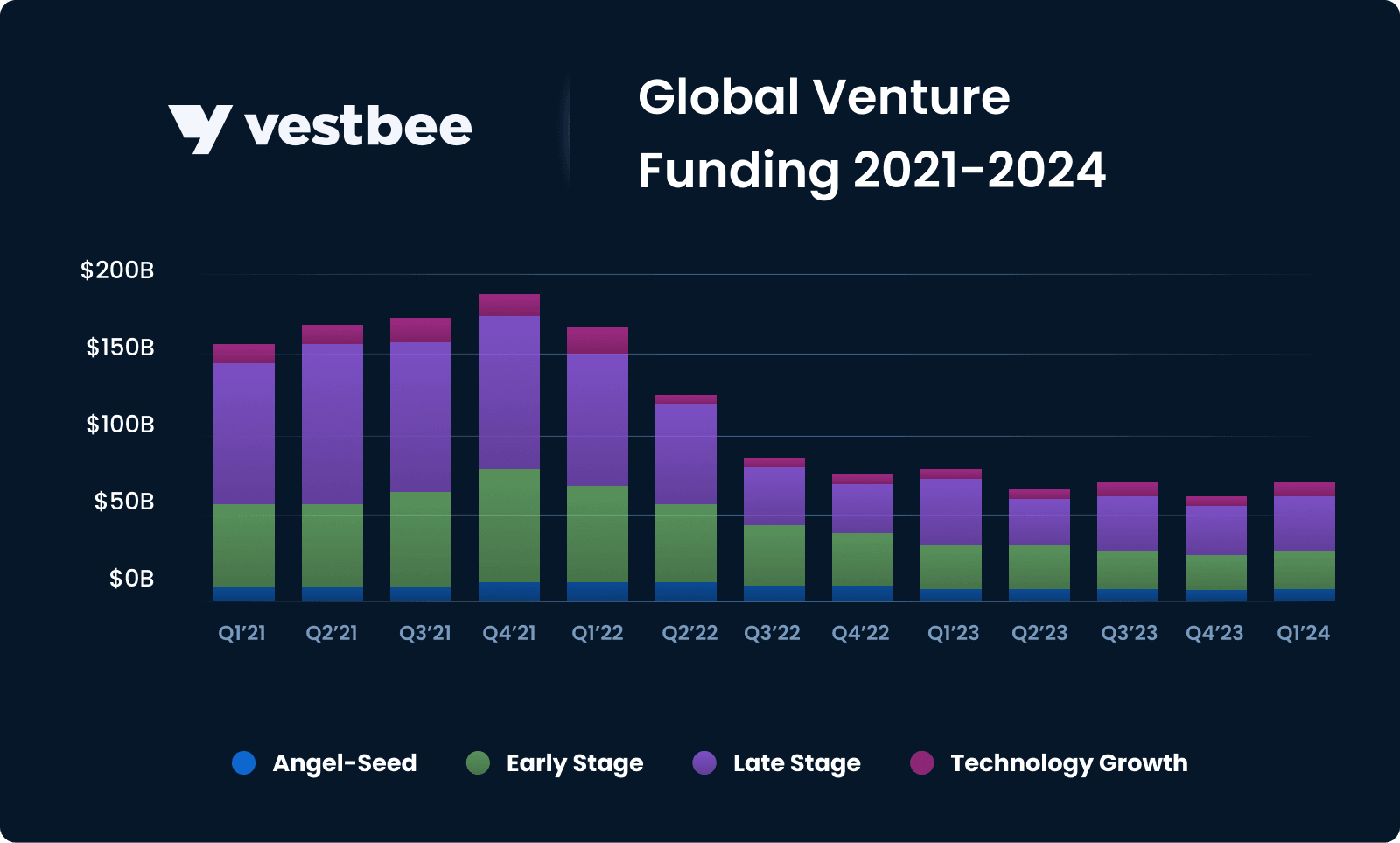

- The first quarter of 2024 witnessed a significant downturn in global startup funding, marking the second-lowest level since 2018. Despite a modest 6% increase compared to the previous quarter, there was a substantial 20% decrease from the same period last year. This decline highlights a cautious approach among investors, who are increasingly favoring early-stage investments amidst a challenging funding landscape. It reflects a strategic shift towards risk mitigation and strategic capital allocation within the venture capital ecosystem.

- Despite not reaching peak levels, it's crucial to acknowledge the substantial growth in the European startup funding landscape over the years. From 2014 to 2021, Europe's venture capital ecosystem experienced consistent growth, with funding levels more than doubling in 2021 alone. However, after a brief surge in 2022, European VC investment returned to pre-2021 levels, indicating a stabilization in the market.

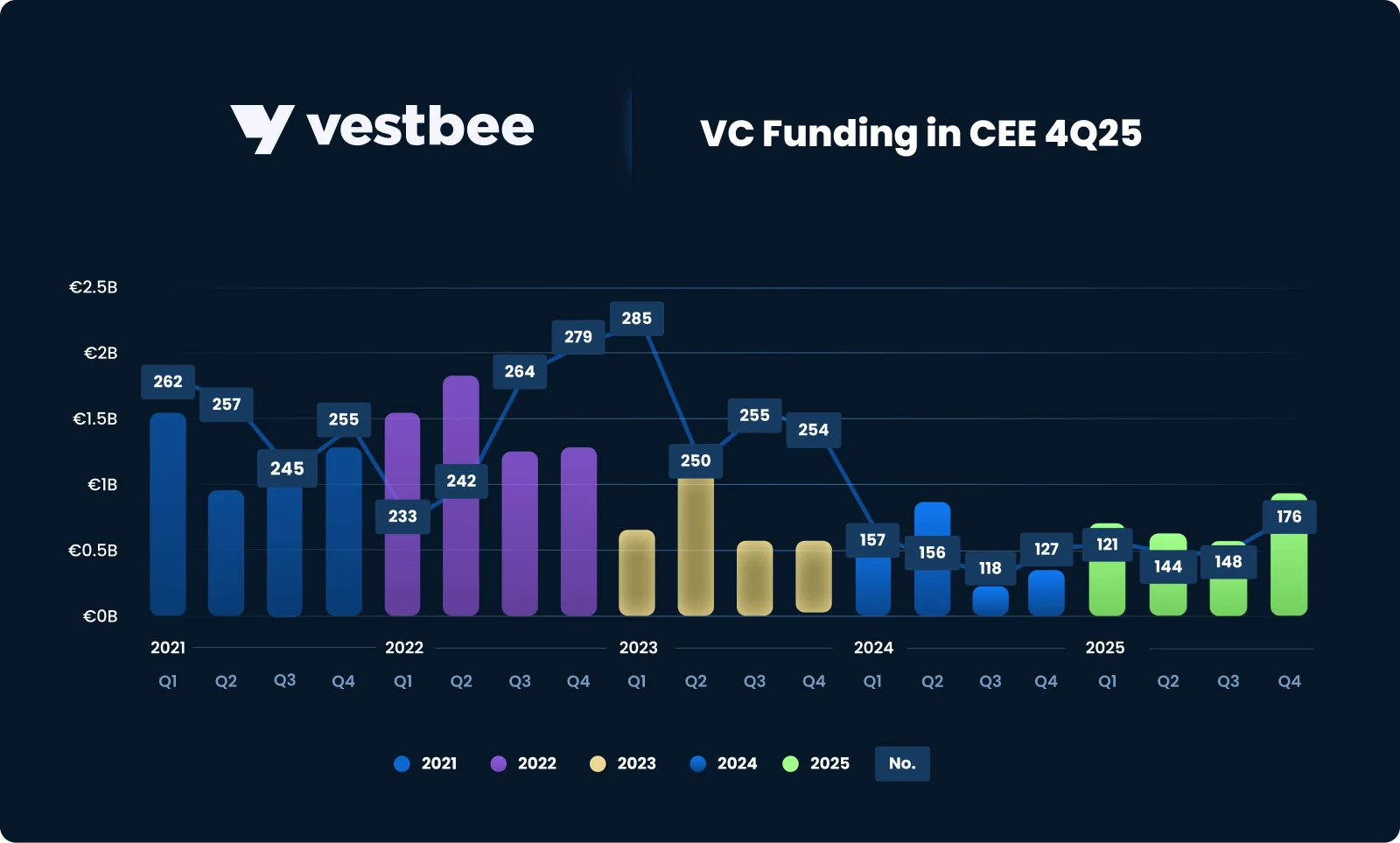

- Similar to previous quarters, there's a palpable sense of anticipation in Central and Eastern Europe, with funding amounts reverting to levels seen in 2019-2020 and stakeholders eagerly awaiting a catalyst to reignite investor interest. While challenges persist, there's optimism for the future, and it's essential to remain vigilant and responsive to the evolving dynamics of the CEE region in the forthcoming quarters.

Global VC investment trends

An analysis of Crunchbase data reveals that the first quarter of 2024 marked the second-lowest global startup funding since the start of 2018. Global venture funding amounted to $66 billion in Q1, representing a 6% QoQ increase but a significant 20% YoY decrease. The previous quarter, Q4 2023, recorded the lowest funding levels in the past six years. Although funding amounts for the most recent quarter are expected to see some upward adjustment as additional data is incorporated and reviewed, the prevailing investor sentiment remains cautious.

In the first quarter, AI maintained its prominence as a top sector for investment. According to Crunchbase data, companies in the AI sector secured $11.4 billion, representing approximately 17% of global funding. Notable rounds in the AI sector included:

- Beijing-based Moonshot AI, a leading language model company, which raised $1 billion with Alibaba Group as the lead investor.

- Sunnyvale, California-based humanoid robot company Figure secured $675 million in funding and forged a partnership with OpenAI.

- Shanghai-based MiniMax, known for its AI companions and avatars, raised $600 million in another round led by Alibaba.

Despite AI's significant presence, it wasn't the largest sector in terms of funding last quarter. The healthcare and biotech industry claimed that title, raising $15.7 billion, or 24% of total global funding, in Q1.

Seed-stage companies secured slightly over $7 billion in funding, marking a decrease of over $1 billion compared to the previous year. Nevertheless, seed funding, known for its resilience even during the last economic downturns, still surpasses the global quarterly amounts observed in 2020. This trend underscores the strategy adopted by many venture investors, who opted to invest earlier in the startup cycle amid a tightened funding environment. Additionally, many founders delayed raising a Series A round, as the criteria for subsequent investment became more stringent.

On the other hand, late-stage companies secured $29.5 billion in funding, reflecting a 36% decrease compared to the previous year, which marks the largest pullback by stage in Q1. In a market characterized by slower funding, late-stage funding typically experiences quarterly fluctuations.

VC investment trends in Europe

According to Crunchbase data, European startups received $11.8 billion in funding during Q1 2024, showing a slight increase from Q4 2023 but a decrease of less than 10% compared to Q1 2023. In general, the total venture funding for European startups in the latest quarter was slightly below the average seen in 2023. During this period, European startups accounted for approximately 18% of global venture capital, while North America retained the lion's share, comprising just over 50% of quarterly venture funding.

The UK dominated the European venture market in Q1, representing 26% of total funding. Germany and France followed closely behind, each accounting for 16% of venture capital allocated in Europe. The Netherlands and Sweden emerged as other significant regions for European funding.

In Europe, key sectors attracting significant funding included financial services, healthcare, and energy. AI companies secured $1.4 billion in funding, representing approximately 12% of European venture capital. Notably, this amount was approximately $1 billion less than the funding raised by financial services companies alone.

Late-stage investments, spanning from Series C onwards, amounted to $4.6 billion invested across 84 companies, while the early-stage funding surpassed late-stage funding in Q1, with over $5.4 billion invested in more than 300 European startups. Remarkably, this trend of early-stage investment outpacing late-stage funding has persisted amidst a slowdown in funding markets throughout 2023. Crunchbase data reveals that this pattern has occurred in three out of the past five quarters. Furthermore, European seed-stage startups secured $1.7 billion in funding across more than 900 companies in Q1, according to Crunchbase data. However, it's worth noting that seed funding has remained below the $2 billion mark since Q3 2023. It's important to keep in mind that seed data tends to lag behind and may increase over time as additional deals are added to the Crunchbase dataset.

VC investment trends in CEE

Over the past five years, the total value of startups in the CEE startup ecosystem has more than doubled, increasing from €89 billion in 2019 to €213 billion in 2023. Notably, startups and scaleups supported by venture capitalists have experienced the most rapid growth, contributing an impressive €21 billion to their value within this timeframe. Between Q4 2023 and Q1 2024, there was a decrease in the number of funding rounds, although the total financing volume remained relatively consistent, with a slight edge favoring Q1 2024. Overall, these figures closely resemble those from 2019-2020 rather than the higher levels seen in 2021-2022.

Notably, significant declines have been observed in the Polish market as well, particularly evident in the reduced activity of seed funds supported by public capital. This quarter underscored the pivotal role these funds play within the Polish market, as their scarcity was keenly felt, resulting in declines both in the value and number of investments. Moreover, the absence of significant funding rounds further compounded the challenges faced by companies seeking funding. However, despite these challenges, the availability of VC funds remains significantly better than pre-2019 levels, and the second quarter is expected to pose continued difficulties for companies seeking financing.

Startup investment rounds in CEE in Q1 2024

- Number of funding rounds: 157 (134 fully disclosed in terms of amount, month, investors, and company details)

- The biggest disclosed investment rounds: Mews - Series D - €101.3M, Project 3 Mobility - Series A - €100M, Starship Technologies - Venture round - €84.6M, Bob W - Series B - €40M, CloudTalk - Series B - €26.3M, Tuum - Series B - €25M.

- Total value of funding closed in CEE: over €640M*

- Countries with the highest number of funding rounds: Estonia - 31 rounds, Poland - 30, Czechia - 18 rounds.

- The most active VC funds: New Vision 3, Credo Ventures, EIT Digital, Vitosha Venture Partners, Presto Ventures, FundingBox Deep Tech Fund, Inventures, Launchub Ventures, Movens Capital, PortfoLion Capital Partners, Practica Capital, Tera Ventures, Baltic Sandbox Ventures, CofounderZone, KAYA VC, Sunfish Partners, Techstars, ZAS Ventures, Coinvest Capital, DEPO Ventures, DOMiNO Ventures, Inovo VC, J&T Ventures, N1 Fund, Reflex Capital, Startup Wise Guys, Taiwania Capital.

- The most popular industries: Enterprise Software, AI, fintech, healthcare, energy, SaaS, cloud.

*23 rounds undisclosed in terms of transaction value

Comparing Q1 2023 with its counterpart in 2024 reveals a consistent aggregate financing value, yet a notable downturn of nearly 50% in the volume of funding rounds is apparent. While the total financing value remained stable, the number of funding rounds decreased from over 280 in Q1 2023 to over 150 in Q1 2024, highlighting the significant challenges companies encounter in securing capital investments during this period. This decline can be attributed to the prevailing macroeconomic landscape, characterized by heightened uncertainty and reduced participation of foreign investors in the CEE region, along with decreased activity of public funds.

Additionally, the market situation is further impacted by several larger rounds, with the few largest rounds collectively raising nearly 50% of total funding this quarter. Excluding these larger rounds would significantly alter the market dynamics.

What shaped the CEE ecosystem in Q1 2024

In Q1 2024, a total of 157 venture capital transactions were recorded. Notably, February stood out with 64 rounds, showing a peak in activity for the quarter. However, the funding amounts in Q1 2024 indicated an overall stagnation, reverting to levels seen in 2019-2020.

Some of the largest rounds disclosed in Q1 were secured by Czech Mews - Series D - €101.3M, Croatian Project 3 Mobility - Series A - €100M, Estonian Starship Technologies - Venture round - €84.6M, Estonian Bob W - Series B - €40M, Slovakian CloudTalk - Series B - €26.3M, and Estonian Tuum - Series B - €25M.

Moving into the first quarter, Estonia, Poland, and Czechia led the way with 31, 30, and 18 funding rounds, respectively. These countries also dominated in terms of total funding amounts, securing nearly 60% of the total funding for the quarter. The thematic focus of investment during this period revealed a strong preference for sectors such as Enterprise Software, AI, Fintech, SaaS, and Cloud, with some minor increases in Hospitality or Mobility during mega-rounds.

Among the most active investors were New Vision 3, Credo Ventures, EIT Digital, Tenity, Vitosha Venture Partners, Presto Ventures, FundingBox Deep Tech Fund, Inventures, Launchub Ventures, Movens Capital, PortfoLion Capital Partners, Practica Capital, Tera Ventures, Baltic Sandbox Ventures, CofounderZone, KAYA VC, Sunfish Partners, Techstars, ZAS Ventures, Coinvest Capital, DEPO Ventures, DOMiNO Ventures, Inovo VC, J&T Ventures, N1 Fund, Reflex Capital, Startup Wise Guys, and Taiwania Capital.

Now, let's discover the note-worthy and recently raised VC funds from CEE.

New VC funds from CEE in 1Q 2024:

- OTB Ventures has closed its second $185 million deeptech fund. It will be used predominantly for Series A investments, with up to a 10% allocation for seed ones.

- Lithuanian Practica Capital has closed its third and largest fund at €80 million. It will target seed-stage investments in tech startups in Lithuania, Latvia, and Estonia, offering up to €3 million initially and ongoing support up to €8 million.

- Poland’s SMOK Ventures has closed its second $25 million fund, with plans to support up to 35 pre-seed and seed startups from Central and Eastern Europe and the region’s founders abroad. The checks’ amounts that the VC usually writes range from $100,000 to $1 million

- Romanian-foundеd GapMinder has launched an €80 million venture capital fund, GapMinder Fund II. It will invest in seed and late seed stages tech companies from Romania, Moldova, Serbia, Croatia, Slovenia, and Bulgaria.

Interested in other new VC funds investing in CEE and Europe? Check out our article New VC Funds Investing in Europe - 1Q 2024.

Let's take a closer look at the Q1 results on a month-by-month basis. However, this review was solely based on fully disclosed rounds (name of startup, closing date, round’s size, participating investors).

Investment rounds in March

- Number of funding rounds: 46

- The biggest investment rounds: Mews - Series D - €101.3M, Argyle - Series C - €14.1M, BotGuard - Series A - €12M

- Total value of funding secured in CEE: over €170M

- Countries with the most funding rounds: Estonia - 14, Poland - 7 rounds.

- The most active VC funds: Vitosha Venture Partners, Tenity

- The most appreciated industries: AI, Blockchain, Fintech, SaaS, Energy.

In March, the CEE startup landscape encountered a challenging funding climate, seeing a total investment of just over €170 million dispersed across 46 disclosed funding rounds. Estonia and Poland emerged as the primary contributors, with 14 and 7 investment rounds, respectively, but it was Czechia that stood out for its significant contribution to the total funding value secured during this period. This was largely fueled by the Series D mega round closed by Mews, marking Czechia's third unicorn with a valuation of $1.2 billion EUR.

However, despite the boost from the Mews mega round, the last month of the quarter exhibited a downturn. Even in comparison to the corresponding months in 2023 and 2022, there was a noticeable decline both in the volume of financing and the number of funding rounds.

The most popular investment directions were AI, blockchain, fintech and SaaS in general, while among the most active investors were Vitosha Venture Partners and Tenity ,but Goldman Sachs, Kinnevik, LGVP, Notion Capital, and Revaia are also worth distinguishing due to their participation in the biggest investment round this month (Mews’).

Find out more: TOP CEE funding rounds closed in March.

Investment rounds in February

- Number of funding rounds: 64

- The biggest investment round: Project 3 Mobility - Series A - €100M, Starship Technologies - Venture round - €84.6M, Bob W - Series B - €40M.

- Total value of funding secured this in CEE: over €340M

- Countries with most funding rounds: Poland - 11, Estonia - 10 rounds.

- The most active VC funds: Credo Ventures, PortfoLion Capital Partners, Baltic Sandbox Ventures, EIT Digital, New Vision 3

- The most appreciated industries: AI, Analytics, Fintech, Healthcare, Hospitality.

February marked the peak of strength within the venture capital landscape for the quarter. The month witnessed a total secured funding of over €340 million, spread across 64 disclosed funding rounds. Notable investments included the ones into companies like Croatian Project 3 Mobility (€100M Series A), Estonia founded and US-based Starship Technologies (€84.6M), and Estonian (Finland-based) Bob W (€40M Series B).

In terms of geographical distribution, funding activity remained consistent with trends observed throughout the quarter, with Poland and Estonia leading the pack with 11 and 10 rounds, respectively. However, Croatia and Estonia emerged as the front-runners in attracting investment, surpassing €105 million and €150 million, respectively.

February saw notable participation from key investors such as Credo Ventures, PortfoLion Capital Partners, Baltic Sandbox Ventures, EIT Digital, and New Vision 3. The spotlight remained on sectors like AI, analytics, SaaS, fintech, with a growing interest in Hospitality, reflecting the ongoing enthusiasm for AI investments amidst a more cautious investment climate.

To sum up, while February stood out as the strongest month in the quarter, a trend of stagnation persisted within the venture capital ecosystem, mirroring the subdued funding dynamics and cautious investor sentiment witnessed in similar periods in 2022-2023.

Find out more: TOP CEE funding rounds closed in February.

Investment rounds in January

- Number of funding rounds: 47

- The biggest investment round: CloudTalk - Series B - €26.3M, Carmoola - Series A - €18.1M, Slovakian InoBat - Series C - €12M

- Total value of funding secured in CEE: over €120M

- Countries with the most funding rounds: Poland - 12, Estonia - 7 rounds, Czechia - 7 rounds.

- The most active VC fund: Credo Ventures, Taiwania Capital, N1 Fund, Movens Capital, ZAS Ventures, Presto Ventures

- The most appreciated industries: AI, SaaS, Analytics.

January marked another relatively subdued month in the CEE VC ecosystem. Startups secured just over €120 million across 47 disclosed funding rounds. While Poland and Estonia once again emerged as the most active ecosystems, hosting 12 and 7 funding rounds respectively, it's worth noting Czechia's notable presence with 7 rounds as well.

Among notable funding rounds were the ones secured by Slovakian CloudTalk (€26.3M Series B), Ukrainian (UK-based) Carmoola (€18.1M Series A), and Slovakian InoBat (€12M Series C). Investors maintained a strong interest in sectors such as AI, SaaS, and analytics. Among the most active investors this month in the CEE landscape were Credo Ventures, Taiwania Capital, N1 Fund, Movens Capital, ZAS Ventures, and Presto Ventures.

In summary, January witnessed a slowdown in the VC ecosystem in CEE compared to comparable periods in 2022-2023.

Find out more: TOP CEE funding rounds closed in January.

Now let’s look closer at the top 50 funding rounds closed in CEE between January and March 2024.

Top 50 CEE startup funding rounds closed in 1Q 2024:

- Mews, a cloud-based hotel property management system that helps simplify hotel operations, so properties can focus on their guests.

- Project 3 Mobility is a startup building an urban ecosystem for autonomous, safe, and effortless movement.

- Starship Technologies develops starship robots that make food and package deliveries more efficient, more convenient and more sustainable, improving everyday life.

- Bob W, a marketplace for premium short-term apartment rentals.

- CloudTalk is a next-gen business calling software.

- Tuum is a cloud-native banking platform that allows any business to offer tailored financial services to their customers.

- Colossyan is the AI video platform for workplace learning.

- Ezra provides full-body MRI screening for potential early cancer and abnormalities in up to 13 organs.

- Carmoola is a mobile application that allows users to get a car finance budget within 60 seconds, apply for a loan, and manage their car finance.

- Argyle unlocks real-time income and employment data through permissioned payroll connections, enabling greater automation, efficiency, and visibility.

- BotGuard provides a service to protect websites against malicious bots, crawlers, scrapers, and hacker attacks.

- InoBat specializes in the pioneering research, development, manufacture, and provision of premium innovative electric batteries.

- Better Stack lets you see inside any stack, debug any issue, and resolve any incident.

- Daytrip is a platform that connects users with local drivers who will transport you door-to-door, from one city to the next.

- Nasekomo is revolutionizing the human food chain by producing animal feeds from organic waste using bio converting insects.

- Saleor Commerce is the world’s fastest growing open-source ecommerce platform, with billions of dollars transacted.

- Sky Engine AI is a full stack deep learning and synthetic data cloud platform for Data Scientists, enabling 3D generative Vision AI at scale.

- Vasa Therapeutics is a private biotechnology company committed to the discovery and development of therapeutics that target the pathophysiology of cardiovascular aging.

- OneNotary provides a reliable online notary service.

- Powerful Medical provides AI solutions that enable medical professionals to accurately diagnose and treat cardiovascular disease.

- edrone creates marketing automation and CRM systems specifically tailored for e-commerce businesses.

- Glycanage is a biological age test to discover, measure and optimize health and wellness.

- Hedepy develops an app that provides psychotherapy through video calls.

- Kurs expands human activities beyond Earth by providing rendezvous and docking technology.

- Evrotrust offers remote identity verification and secures qualified electronic signatures.

- GScan is the world leader to 'x-ray' infra and industrial objects to assess their integrity and aging using only safe flux of cosmic muons.

- Upheal is a leading AI therapy notes and analytics platform for mental health professionals.

- Sessions develops an AI-powered platform that makes meetings & webinars insanely productive.

- SP Tech develops the algorithms that optimize railways around the world.

- Competera is an industry-agnostic pricing solution for online, offline, omnichannel, mono- or multi-brand retailers.

- Mindgram develops a science-based platform and mobile app for complete mental wellness.

- Choice is a SaaS service for DINE IN experience, take away and own delivery.

- Livespace creates a process-focused CRM platform for B2B sales teams.

- Flowpay provides small and medium size enterprises with short and medium-term financing opportunities for their activities.

- Rendin is a rental platform that offers home rentals and secure rental agreements.

- Evergrowth is the premiere B2B account-based sales platform, leveraging AI-driven insights to craft customer-centric sales frameworks.

- Axiology provides a tokenized securities depository, leveraging distributed ledger technologies for tokenized sustainable securities.

- PeopleForce develops an HR software for businesses that provides HR solutions for onboarding, recruiting, time tracking, performance, and more.

- SmartSchool is an AI teaching assistant for math teachers that grades student work and gives them instant & personalized feedback.

- Maas Loop develops a waste recycling solution that helps retailers, catering, and hotel sectors to recycle metal, glass, and plastic garbage.

- Aleet is a technology company specializing in the dynamic management of fleet operations with a use of AI/ML.

- Gotiva is a technology company developing innovative entertainment apps that empower digital content creators to distribute and monetize their content to millions of users worldwide.

- CTO2B helps organizations in managing the cloud service adoption and runtime operations.

- Cognitiwe addresses inefficiencies in fresh food and grocery retail to help them reduce waste, save energy and resources to be more sustainable.

- Scorestars is a catalyst for a new era of sports entertainment, integrating licensed digital players into live games to elevate fan engagement.

- XVision is an automated x-ray analysis application that assists radiologists by providing accurate interpretations of medical images.

- 1.security is an operator of a cybersecurity platform designed to manage the Microsoft environment.

- Codejet allows you to save at least 50% of developers' time by transforming projects created in Figma into clean and ready code.

- Multilango is an operator of a learning platform designed to improve employees' language skills.

- Lakmoos provides instant market research. The startup builds data models that simulate how target groups make decisions.

If you have some insights about the report, drop me a line!

Want to get a more detailed view of the CEE startup & VC ecosystem in Q1 2024?

Discover our monthly, quarterly, and yearly reports:

- VC Transactions in CEE in 1Q 2023

- VC Transactions in CEE in 2Q 2023

- Central and Eastern European Startups Report 2024

- New VC Funds Investing in Europe - 1Q 2024

- TOP CEE funding rounds closed in January

- TOP CEE funding rounds closed in February

- TOP CEE funding rounds closed in March

Disclaimer: This report features VC rounds that have been publicly disclosed before the publication date or were shared by our VC and startup community. Grants and transactions below €50,000 were not considered. Furthermore, while we value all startups operating in CEE, our focus is on companies that originate from the region, self-identify as CEE companies, or have a significant presence of CEE founders.

Sources: Vestbee VC & startup community, startup press releases, web & social media monitoring, Crunchbase, PFR (Polish Development Fund), Dealroom.