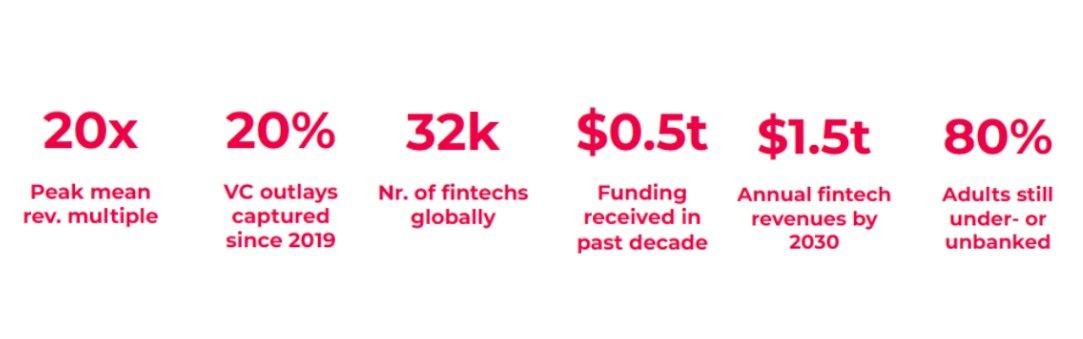

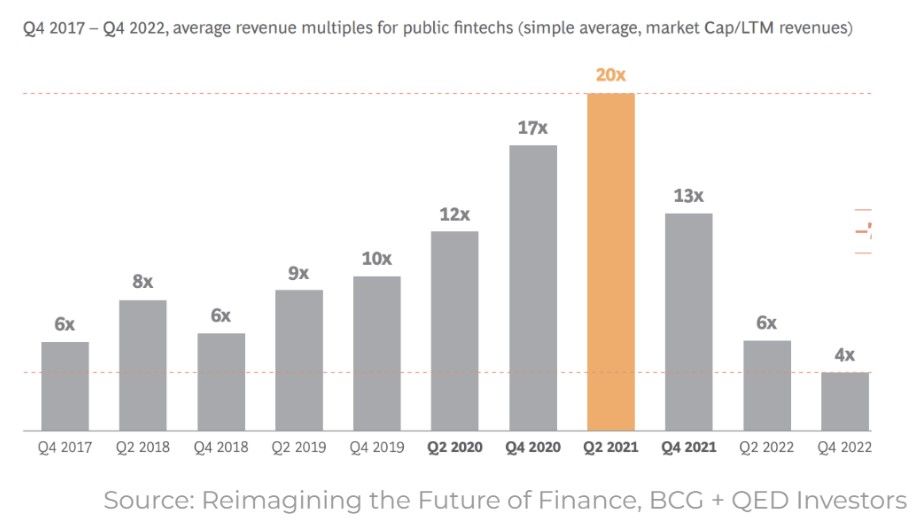

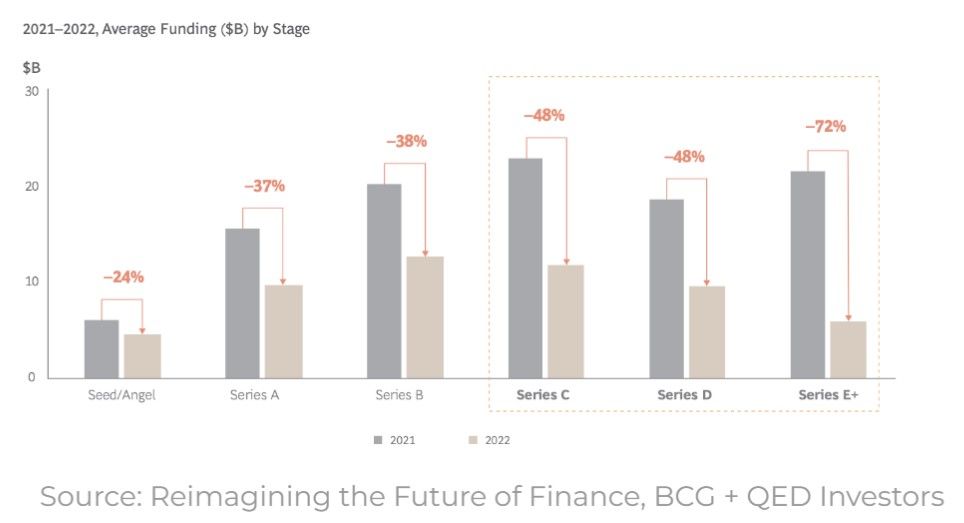

The pandemic served as a catalyst for broad consumer adoption of digital financial services, propelling certain fintech segments like payments and transaction banking into the mainstream through transformative players like Stripe, Square, and Alipay. However, a shift occurred in early 2022 as fintech valuations plummeted by 60%, even as revenue growth maintained a more moderate pace. This was accompanied by a notable 40% decline in new funding, particularly in the later stages of development, prompting a refocus on attaining profitability over extravagant expansion. This transformation signifies a maturation within the industry, emphasizing sustainable growth in place of rapid but unsustainable success.

Fintech Collapse

Persistent inflation, fueled by a confluence of factors including geopolitical tensions, supply-chain disruptions, and the arduous process of post-pandemic recovery, has yielded a noteworthy outcome: the escalation of interest rates, effectively eradicating the availability of zero-priced funding.

A shakeout is underway, targeting growth-stage enterprises grappling with ambiguous product-market congruence. Amid this evolution, attention has pivoted towards bolstering unit economics, nurturing recurring revenue streams, securing patents, cultivating devoted customer bases, and fortifying brand identities.

A brighter future

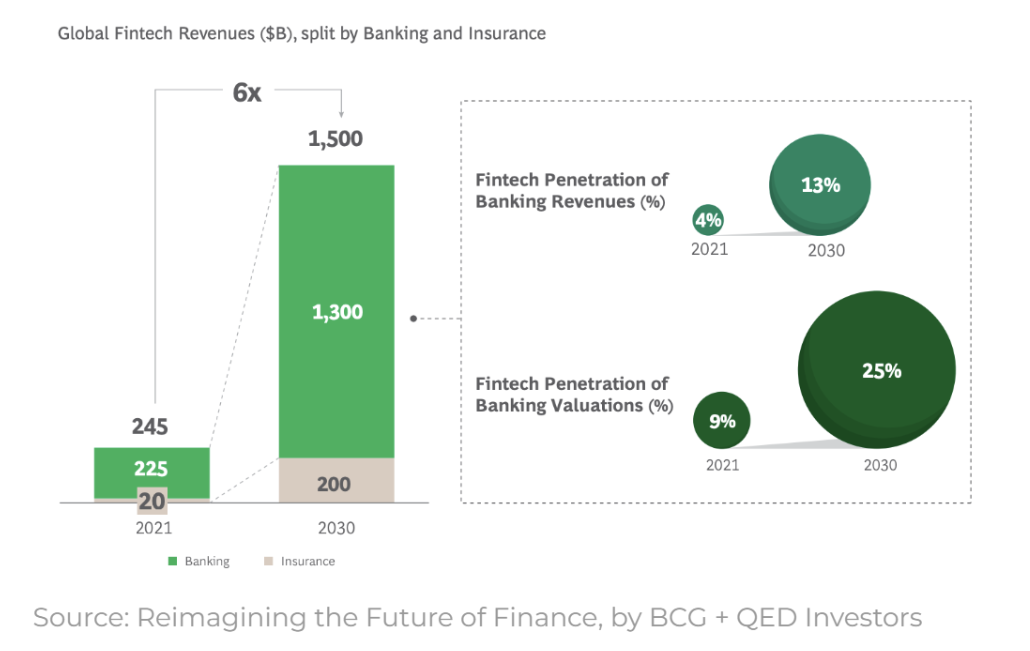

The financial services industry remains exceptionally conducive to revolutionary change on multiple fronts. Despite being one of the largest and most lucrative business segments, it paradoxically lags behind in delivering satisfactory customer experiences. This incongruity is further accentuated by the staggering statistics: a staggering 1.5 billion adults globally remain unbanked, while an additional 2.8 billion are categorized as underbanked. Astonishingly, even with its vast potential, the industry has merely harnessed a mere 2% of its revenue capacity. This glaring disparity between existing reality and potential advancement underscores the immense opportunities that still await transformative innovations within the financial services realm.

There are two, somewhat connected, trends that further fuel long-term optimism when looking at the infrastructure supporting the ongoing fintech revolution. These are the unbundling (and perhaps re-bundling) of the financial infrastructure and brands from non-financial backgrounds entering the financial services industry (embedded finance), often relying on technology-heavy solutions to target existing retail consumers.

The unbundling of financial infrastructure

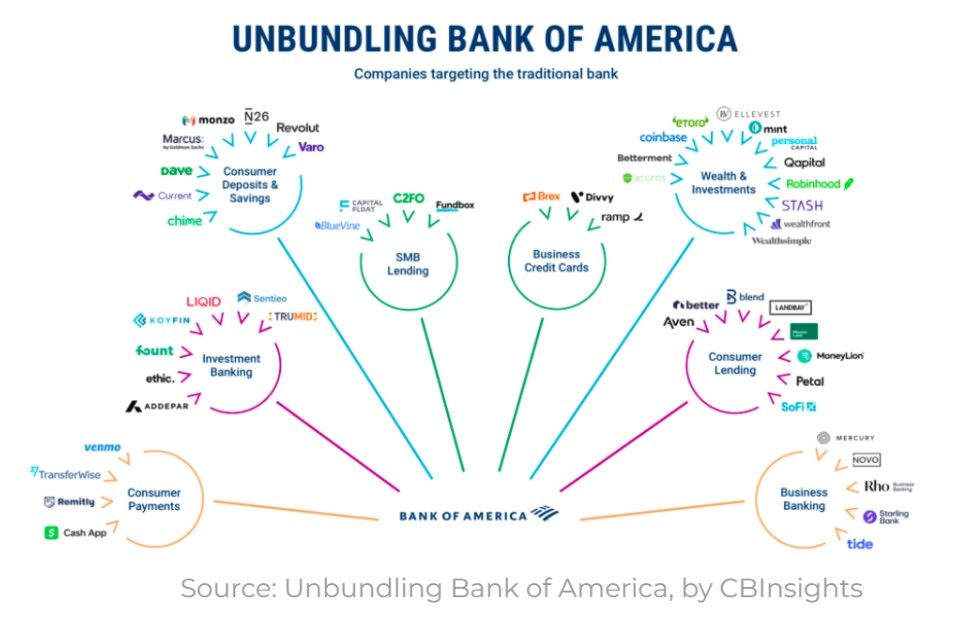

A wide variety of fintechs have sprung up in the past decade slowly chipping away at large banks dominance in a variety of fields, by focusing on niche tailored solutions and value propositions, serving long-tail clients or simply competing on ease-of-use and price in single domains. The below image created by CBInsights illustrates the ongoing unbundling quite well in a variety of fields.

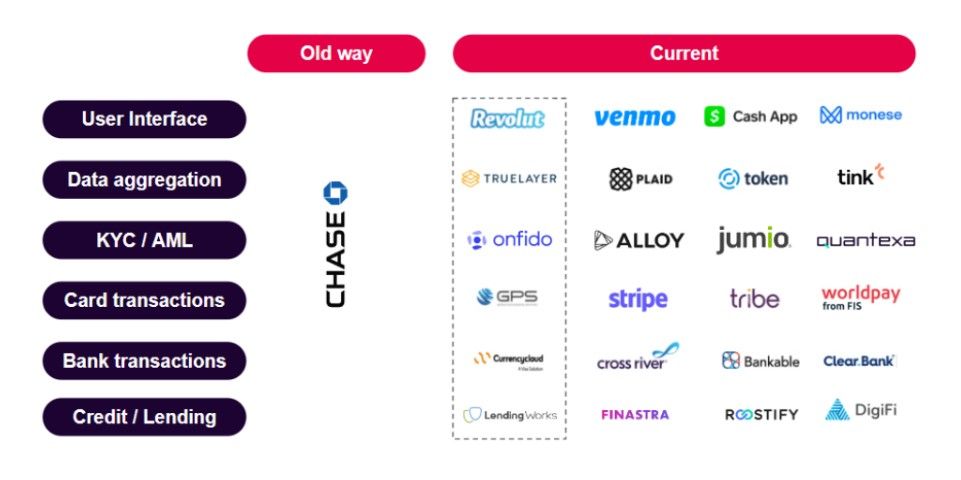

However, the unbundling of financial services goes even deeper than this. Even the rapid rise of many of the disruptors themselves has been built on the white-labeling APIs of many specialized “as-a-service” solutions. Reducing the need for in-house development and at times leveraging the already acquired licenses of providers, has allowed new fintechs to seriously reduce their go-to-market and allows them to keep adding new products and services at a previously unthinkable pace.

Perhaps not unexpectedly the trend that immediately followed the complete unbundling of the secor was a sort-of rebundling of all these back-end solutions with a variety of middleware or BaaS provider with different approaches gathering multiple use cases to create one-stop-shop experiences, further reducing internal development needs and GTM.

Brands entering financial services

In a striking convergence of industries, several prominent companies are expanding their horizons beyond their core offerings to venture into the realm of financial services. E-commerce platforms, once primarily focused on enabling businesses to establish and manage online stores, are now seizing a substantial portion of their revenue from financial services. These services encompass not only payment processing solutions but also innovative offerings like financing options, banking-like applications such as Shopify Card and Shopify Balance. Similarly, cloud-based business management software tailored for wellness services, exemplified by yoga studios, has not only streamlined operations but has also embraced financial services, capturing over half of their revenue from payment processing and financing options.

On the ridesharing front, industry behemoth Uber has orchestrated a strategic entry into the financial services arena. Leveraging its extensive user base and aiming for a closed-loop ecosystem, Uber has woven a web of financial services offerings. The repertoire includes Uber Wallet, Uber Money, Uber Credit, and the Uber Debit card, transforming the ridesharing platform into a multifaceted financial hub.

Even within the realm of retail, companies like Walmart have ventured into the financial services sector with remarkable prowess. Diversifying their services beyond traditional retail operations, Walmart now extends its influence through Walmart Pay, a mobile payment system, Walmart MoneyCard, a prepaid debit card service, and Walmart2Walmart, a money transfer solution. This strategic expansion signifies a broader trend where corporations are leveraging their brand recognition and customer base to establish a formidable presence in the financial services landscape.

In essence, the convergence of various industries with financial services underscores a fundamental transformation in business models. Companies are recognizing the value of integrating financial offerings with their core services to foster customer loyalty, create self-contained ecosystems, and explore new revenue streams. This synergy not only benefits businesses by providing diversified income channels but also enhances the customer experience by offering integrated and convenient solutions for both their primary needs and financial requirements.

Key Takeaways

The fintech landscape boasts robust fundamentals and immense potential, regardless of prevailing market conditions. While payments will continue as the primary category, a host of novel sub-categories are sprouting within, such as the noteworthy emergence of chargebacks. B2B solutions catering to SMBs and the B2B2X model are poised for the most substantial growth. The rise of local champions is reshaping the industry, while businesses operating across borders—like neobanks and lending platforms—may face hurdles in developed markets but find substantial opportunities in emerging economies for fostering financial inclusivity. The expansion of big-tech players and incumbents further intensifies the competitive arena. Despite challenges in predicting winners and timing recovery, investment in the industry's infrastructure remains a prudent strategy.

Related Posts:

FinTech Startups From NAMER, EMEA and LATAM To Keep On The Radar (by Sofia Drobychevskaya, Editor, Vestbee)

VC Of The Month - Flashpoint (by Konrad Koncerewicz, Head of VC & Startups, Vestbee)

Top FinTech VC Funds From Europe To Finance Your Startup (by Katarzyna Skoneczna, Editor, Vestbee)