In 2025, the EIC Fund, the European Innovation Council's investment arm, had its busiest year ever: more than €500 million deployed across 130-plus deals. Since 2021, the EIC Fund has put over €1.7 billion into roughly 350 deeptech companies and crowded in €5 billion of private capital alongside it — €3.5 for every euro of EU budget. By its own account, it is now one of Europe's largest and most active deeptech investors.

And yet most founders still file their EIC Accelerator application as if they were asking for a grant.

That is the first of two common misreadings. The second belongs to the founders who swing the other way — who treat an EIC win as a substitute for a lead investor, and learn the hard way that it isn't.

Both miss the same thing: the EIC Accelerator is two instruments bolted together. The non-dilutive grant comes first and can be existential. The equity — the larger sum, and the part that makes the EIC an investor at all — comes next, sometimes arriving only after additional milestones, months, or even years, after the grant agreement is signed.

Over recent weeks, I took a closer look at the EIC Accelerator dealflow and interviewed a few European VCs and founders who have raised EIC blended finance. Their answers, alongside the EIC's own 2026 data, tell three overlapping but distinct stories.

What the EIC Accelerator actually is

Before going further, it's worth being clear about what the EIC Accelerator actually is, because outside the EU-funding world, it is widely misunderstood. It is the flagship instrument of the European Innovation Council, one of the pillars of Horizon Europe, the EU's €10-billion-plus innovation programme running from 2021 to 2027. Only in 2026, the EIC Accelerator alone has a budget of €634 million. It exists to do one specific thing: take single deeptech startups and SMEs with breakthrough, potentially market-creating technology from TRL 6 upwards, through to market deployment, the awkward stretch between a working prototype and a sellable product — and push them across the funding gap that private capital usually finds too risky to cross alone. It is open to companies established in an EU member state or a Horizon Europe Associated Country. Ukraine and Switzerland, for instance, qualify in full. The UK is the telling exception: it is associated for the grant but carved out of the EIC Fund's equity, because Britain opted out of the EU's financial instruments after Brexit. A British startup can apply for the €2.5 million grant, but remains ineligible for the investment — the clearest possible sign that the two halves of this programme are separate instruments, with separate rules.

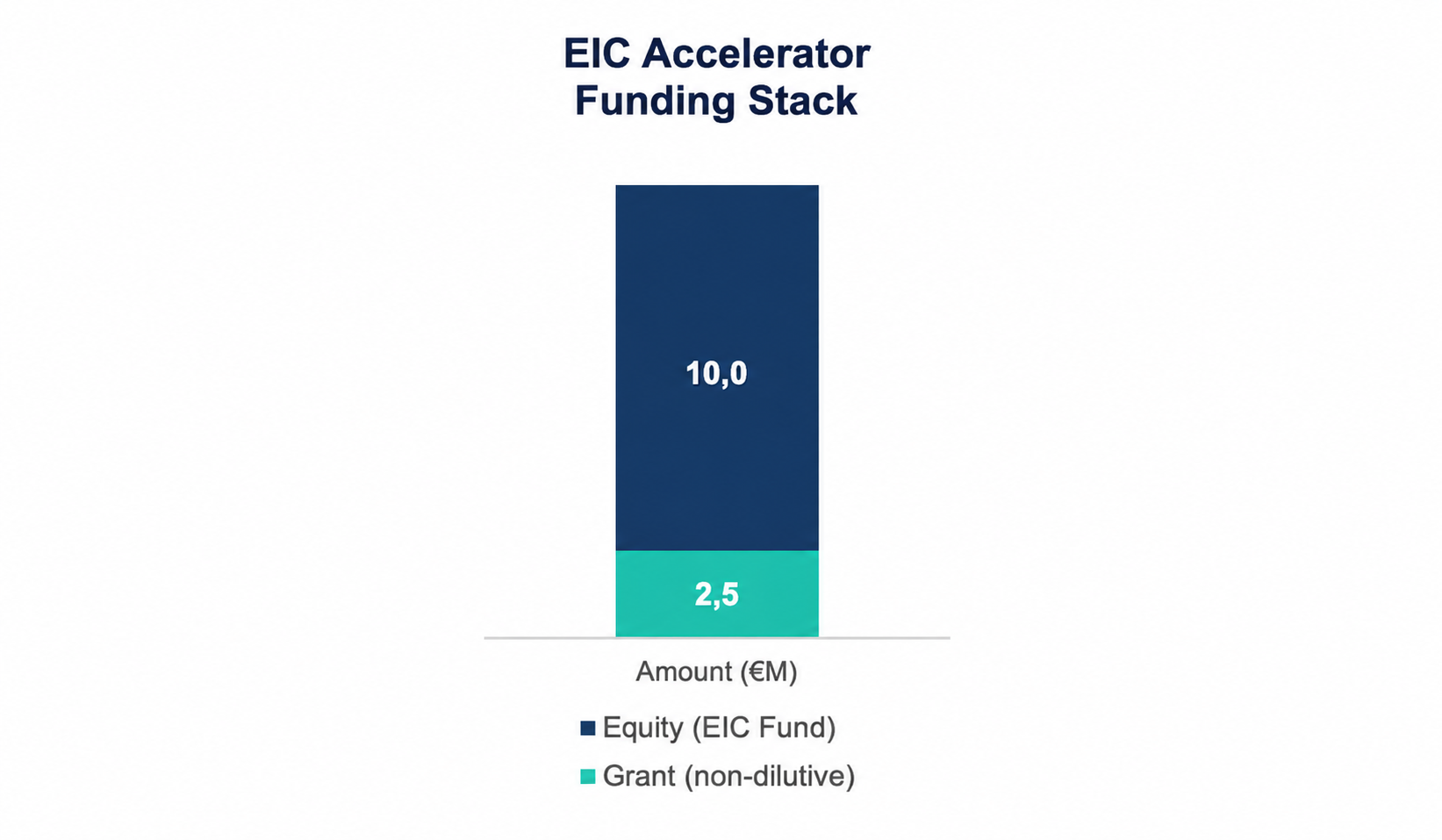

The funding comes in three shapes: grant only (up to €2.5 million, non-dilutive, covering 70% of eligible costs), equity only (up to €10 million through the EIC Fund), or — most commonly — blended finance combining the two, a package worth up to €12.5 million.

Crucially, the two components are sequential in their award order, but can be implemented in parallel. First, the grant is awarded by the EIC on the strength of a written proposal and a jury interview. The equity is decided afterwards by the EIC Fund, following its own due diligence run by the European Investment Bank. As a result, a company can be selected for funding, sign its grant agreement, and still be months away from knowing whether — and on what terms — the investment will actually land.

Getting even that far is brutally hard. Applicants pass a short, 12-page Step 1 screening (Short Application), then a 20-page Step 2 proposal backed by annexes of supporting evidence (Full Application) — whose evaluation now includes a technological expert interview — and finally a Step 3 jury interview in Brussels. End to end, the success rate sits in single digits (~7%). Even among the companies that reach the interview stage, only around a quarter walk away funded. Winning the EIC Accelerator is treated as a credential, and rightly so.

The equity itself behaves like venture capital, not a subsidy. The EIC Fund takes minority stakes — typically 10 to 20% — in cheques of €0,5 to €10 million, and it is patient money: a seven-to-ten-year horizon, up to fifteen, exiting only once a company can stand on private financing, through an IPO, a buy-out or a secondary sale. In strategic sectors, it can take a blocking stake to protect European interests. But the defining rule is this: the Fund never invests alone. It casts itself as an "initial risk-taker", even though this role belongs rather to the grant than equity component, and, by its own guidelines, systematically seeks co-investment on at least a one-to-one basis — a euro of private capital for every euro it commits. For a founder, the implication is structural and easy to miss: the EIC's investment is, by design, contingent on also convincing private investors to show up.

How the EIC sees itself

So much for the mechanics. The EIC's account of itself is more ambitious: not a grant-giver but Europe's deeptech "investor of choice," running its portfolio with the proactive, thesis-driven style it borrows from America's ARPA. The numbers it puts forward back the story up. Its 2026 Impact Report claims a portfolio of three unicorns, nine companies valued above €500 million and roughly 120 above €100 million, alongside twelve exits. The companies it has backed have gone on to raise more than €15.5 billion between them. In quantum and semiconductors, the EIC sat in close to half of all EU venture investment last year. In space, a quarter. Whatever else it is, it is not behaving like a donor.

For a founder, the point is not how the EIC ranks against other investors, but what this means for the way you apply. The grant is the appetiser, while the equity is the main course, and many startups still write the proposal like a typical grant application, not an investment memo. They lead with technology-readiness levels and work packages, and bury the things an investor actually underwrites: the market, the traction, the team, the unfair advantage, the route to a return. The people on the other side of the table — expert evaluators and a jury — increasingly think like investors. The proposals that win read like investments.

How VCs actually treat it

Ask the people the EIC says it co-invests with, and a more textured picture emerges — one that depends heavily on where a fund sits in the capital stack. Bitspiration Booster VC, a Cracow fund writing €100,000–€500,000 cheques at pre-seed and seed, is usually in a company before it ever applies to the EIC. For a fund like that, the EIC isn't a source of deals; it's a downstream destination.

"We don't use the EIC pipeline for sourcing," says Andrzej Targosz of Bitspiration Booster. "It works the other way around — our portfolio companies become EIC beneficiaries later. Four of the ten Polish EIC Accelerator winners were already in our portfolio before they won."

Bitspiration treats the EIC Fund as a co-investor like any other — held to the same standards, not a kingmaker, which fits the Fund's own rule that it can never be a company's only backer.

Move up the stack and the relationship inverts. OTB Ventures — Warsaw-based, writing Series A cheques from €1 million to €25 million and beyond — sits downstream of the EIC, and it does use the programme as a sourcing channel. That is partly why it joined the EIC's Trusted Investor Network: as Managing Partner Marcin Hejka notes in the EIC's 2026 report, the network widened the fund's deal flow into companies that might otherwise have taken longer to reach it. The EIC, in effect, sits in the middle of the European deeptech stack — seed funds feed into it, growth funds fish out of it.

Where the two funds agree is more telling than where they differ. Neither lets an EIC win move its own process. Selection — even an invitation to the final jury — does not raise diligence priority, speed up a term sheet, or lift a valuation. "It can be a positive validation signal, especially in deeptech," Targosz said, "but it doesn't replace our own assessment of the technology, the team and the market." Hejka, from the opposite end of the stack, is just as measured: the EIC is a catalyst and a validator, but the process is "more structured and time-consuming than purely private rounds." Two funds, two stages, one conclusion: the EIC is validation, not conviction. It tells the market a company is worth a look. It does not tell the market the round is done.

What founders experience

Founders see the split most clearly of all, because they live on both sides of it. The grant, when it lands, can be the difference between a company and a corpse. Bartłomiej Roszkowski, co-CEO of the Polish biotech Proteine Resources — only the ninth Polish company ever to win the EIC Accelerator — is blunt about it:

"Without the EIC, the company would have gone stagnant — and we wouldn't have Radix on board," he says, referring to the venture round that followed. On the grant side, he adds, the EIC was "great — no problems": fast, non-dilutive, and, in his case, existential.

*UpSpark advised Proteine Resources on its EIC application.

The equity is a different animal. Where the grant is decided largely on the proposal, the investment is a separate process run by the EIC Fund and the EIB — and it is relatively slow and conditional by nature. The decision can be deferred for months after due diligence begins, with fresh milestones attached even once the grant is signed and the company is already well known to the programme. The mechanics compound the wait: the Fund typically takes the lead investor's terms, then layers its own conditions and safeguards into the documentation, leaving the founder to choreograph the company, the lead and the EIC at once. The appetiser arrives first, usually within 5-8 months from submitting the Short Application. The main course follows, but can be months, or sometimes years, behind it. It can also never arrive too.

Even when the money is welcome, founders are clear about what it does and doesn't do. Paulina Mazurek, CEO of the quantum-software company BEIT, found the EIC decision opened doors: it was a strong early signal, "especially for a CEE deeptech company that has to build credibility faster than firms from more obvious hubs." But it did not close anything. None of the funds that took an interest right after the decision actually invested. The EIC's arrival on the cap table, she says, did not change the risk category investors placed the company in. The questions that decide a deeptech round — how fast the science becomes a product, how it scales — were exactly the same the morning after the win as the morning before. Winning the EIC opens doors. It does not close your round.

This is not universal, and it would be dishonest to pretend otherwise. The EIC's own 2026 report showcases founders for whom the equity did real work: a Norwegian AI company that credits the Fund's co-investment with helping convince its lead to join the next round; a German robotics firm that read the follow-on as a signal of long-term conviction; an Italian biotech that closed an €83.5 million Series A within months of selection. The honest synthesis is that outcomes vary — but the variation has a shape. The grant and the validation are the dependable parts. The equity is where the timing, the conditions and the uncertainty concentrate. The EIC is a reliable opener of doors. Whether it helps close the round depends on the company, the stage and, as we'll see, sometimes the postcode.

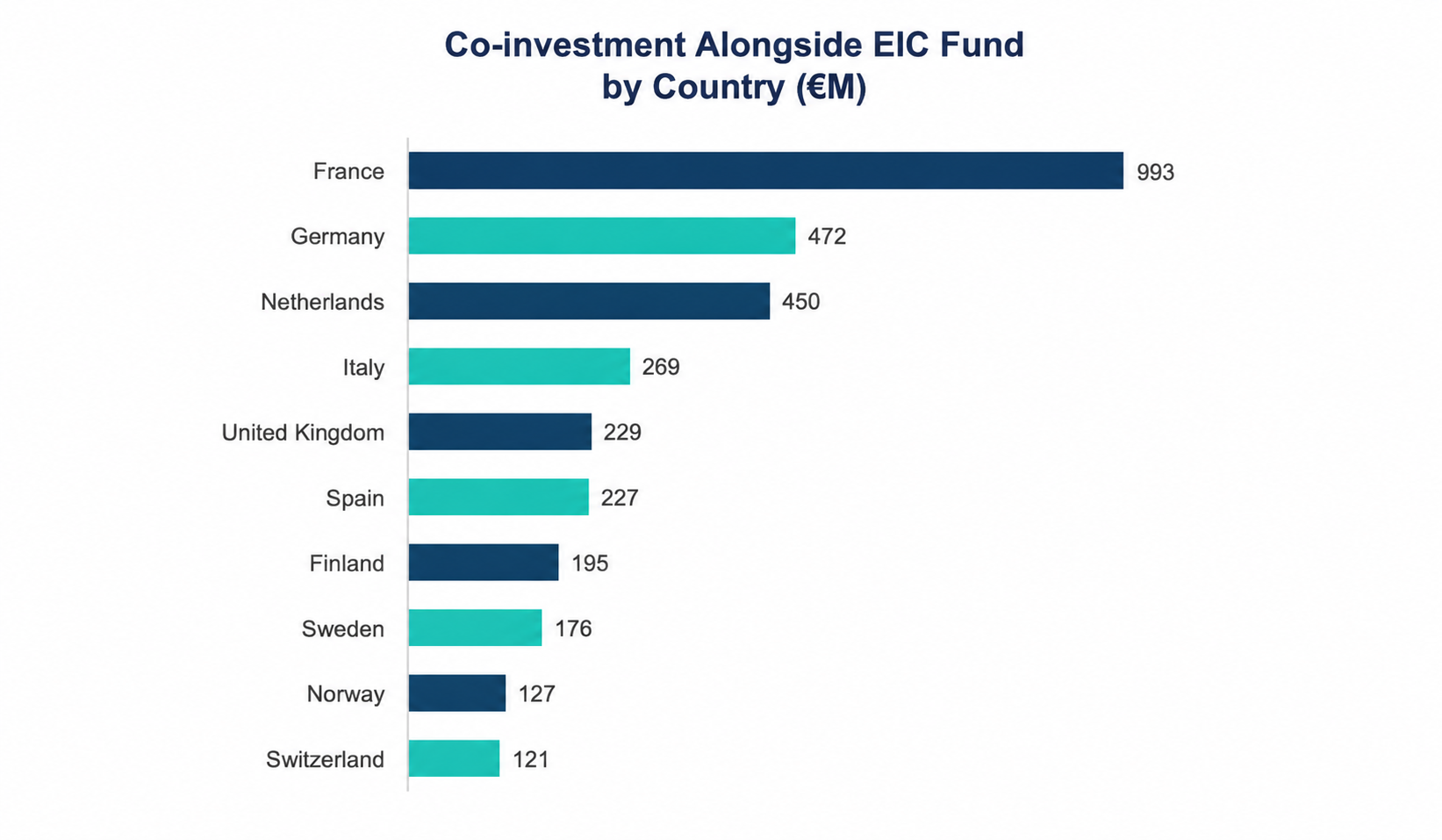

The CEE gap

And the postcode matters. The EIC is meant to be pan-European, but in practice its money doesn't spread evenly. In 2025, just 5% of EIC Accelerator companies came from Horizon Europe's "widening" countries — the lower-R&D-intensity member states that include most of Central and Eastern Europe — down from 6% the year before. The imbalance runs through the co-investment too: not one CEE country appears among the top ten European co-investors alongside the EIC Fund, a table led by France, Germany and the Netherlands. Proteine Resources, being only the ninth Polish company ever to win the EIC Accelerator, is not an anomaly. It is the pattern. The causes look structural rather than conspiratorial — a thinner capital stack, fewer serial founders who have scaled a deeptech company globally and can pattern-match the next one. Not, as far as the evidence goes, anything in how Brussels scores the proposals.

That thinness is also why the EIC matters more here. For a founder in Cracow or Vilnius, an EIC win does the work a Sand Hill Road logo does elsewhere: it manufactures the credibility a local track record can't yet supply. Exactly the early signal Mazurek valued. The CEE investor base is emerging in parallel — Bitspiration feeding companies in at seed from Cracow, OTB pulling them out at Series A from Warsaw, to use our examples — but it remains thin and stage-segmented. Whether the CEE origin also slows the equity process is harder to say. One founder wondered aloud whether a drawn-out investment decision owed something to it. Another put the friction down to local legal execution rather than geography. Neither would commit. The honest answer is that the gap is real, mostly structural, and only the EIC itself holds the data to say more.

What this means for founders

So what should a founder actually do with all this? Two things, mostly. The first is to take the investment memo framing literally, and to start early. Since the EIC Accelerator’s Full Proposal was capped at twenty pages in 2026, the centre of gravity has shifted to the annexes — the evidence files. Letters of intent and support, a freedom-to-operate report, emails from prospective investors, offtakers and suppliers: the third-party proof that turns a claim into a fact. Every piece of it takes time and diligence to assemble, and founders who only start chasing it after the Step 2 invitation arrives reach the deadline with prose where they needed proof. Gather the evidence from day one, not when Brussels asks for it.

The second is to be honest with yourself about what the win buys you. It buys validation and a grant — real things, sometimes existential ones. It does not buy a lead investor, and by the Fund's own matching rule, it never can. So run your private fundraising in parallel, not in sequence: line up the conversations that will actually close your round while the EIC process grinds on, rather than waiting for an equity decision that may be milestones and many months away. Until the EIC Fund's money is on your cap table, model your runway as if it might not arrive on time — because, often, it won't.

Finally, work with the investors already around you — but know the limits. The grant is non-dilutive, so it extends your runway without diluting anyone or asking the cap table for fresh cash: good news for the people already on it, and a reason to bring them in early. Many will re-up. But the EIC Fund does not price the round itself — it follows a lead investor who sets the valuation and the terms, and that lead has to come from outside your existing cap table. Insiders can join alongside new money, but they cannot be the whole round, and they cannot be the lead. It is the matching rule in different clothes: to unlock the equity, you must go out and win a new lead. The EIC requires the very thing it cannot give you.

Two footnotes. The Trusted Investor Network mostly takes care of itself — the EIC introduces its winners to the Network members after selection, though reaching out a little earlier won't hurt. And whoever you're speaking to, mention that the equity diligence is run by the European Investment Bank, not waved through by a grants committee. Many investors don't know it, and it changes how the ticket reads on a cap table.

The bottom line

None of this diminishes what the EIC is. It is real money, real validation, and — on the evidence of its own portfolio — a genuine force in European deeptech. It is simply not the thing either camp takes it for. To the founders who treat it as a grant: it is an investor, and it will read your proposal as one, so write it that way. To those who treat it as a lead: it is a validator, not a closer, and it will hand you the room without handing you the round. Win the room; then go win the round.

For VCs, the mirror image holds. An EIC ticket is a signal worth reading — especially at the growth stage, where the pipeline is genuine deal flow — but it was never meant to replace your own conviction. The EIC opens the door. Walking through it is still the founder's job, and the investor's call.

About UpSpark

Jakub Żbikowski is CEO and co-founder of UpSpark, a Cracow-based EU-funding consultancy specialising in deeptech and market-oriented programmes, including the EIC Accelerator. UpSpark’s overall success rate, across all programs the company targets, stands at around 40%, while in the super-competitive EIC Accelerator, it is approx. 19% (against a programme average of ~7%).

Disclosure: the author's firm advises companies on their EIC applications, including some referenced here — among them Proteine Resources cited in the article. All interviewees are quoted with their consent.