In business, a unicorn is broadly defined as a privately held and VC-backed company valued at $1bn. The number of unicorns originating from a specific country or region is often a good indicator of the development and maturation stage of the local startup ecosystem. As of 2022, Europe has generated a total of 179 unicorns, and 44 of them originate from the CEE region.

In this article, we will examine the unicorns originating from Europe, and more precisely - the CEE region - discovering trends that emerged in 2021 and 2022, the most popular industries and verticals, countries with the best environment for giant tech companies as well as VC firms that contributed the most to the financial well-being of CEE unicorns.

However, to do so, we must first look at the broader picture of Europe as a whole.

Unicorns: a backdrop in Europe

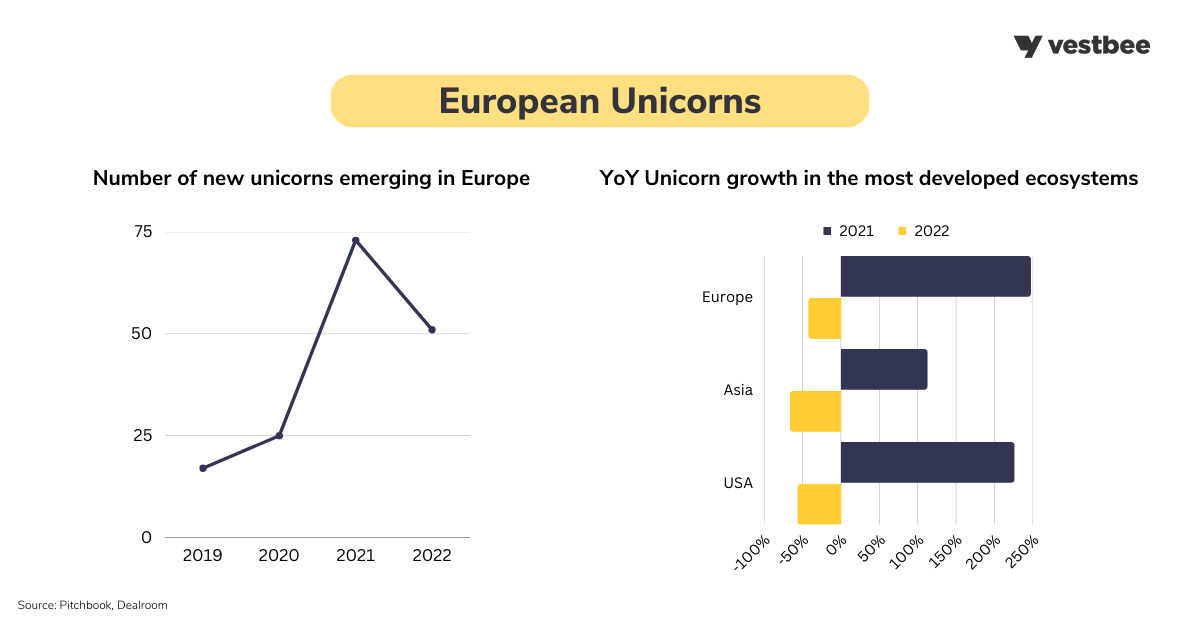

In recent years, Europe has seen unprecedented growth in the number of privately held, venture capital-backed companies valued at over $1 billion, referred to as unicorns. According to data from Pitchbook, the number of unicorns in Europe has been steadily increasing over the past decade, with a significant jump in the number of new unicorns from 2019 to 2021. In 2019 only 17 new unicorns emerged on the continent, 25 turned up in 2020, and 73 in 2021. However, this growth halted in 2022 due to an economic slowdown, and we saw the emergence of 51 new unicorns in 2022.

Despite this, the pace of unicorn growth in Europe during this time period was still higher than in more developed ecosystems, such as the US and Asia. In particular, 2021 was a record-breaking year for European unicorns, with a YoY growth of 246.7%, surpassing the growth in the US and Asia. Additionally, as reported by Pitchbook, the overall value of European unicorns has been increasing rapidly, reaching €466.2 billion by the end of September 2022, a 40.7% increase from the end of 2021.

On the other hand, the average unicorn valuation doesn’t look quite as rosy. Even though companies are still closing deals, the recent downturn has affected the valuations, which in turn have been systematically shrinking. The continuous rise was broken off in 2022 when the drop was recorded - from €4.0 billion in Q1 to €3.7 billion in Q3, according to Pitchbook data. This is most likely due to major down rounds of two giants - Swedish “buy now, pay later” company Klarna was cut by 82.8% and UK’s fintech SumUp saw a valuation decrease of 60%.

When it comes to the new year 2023 ahead, many analysts and fund managers predict that this trend of slashed valuations will continue, especially at later stages. It’s even possible that more tech giants might lose their unicorn status, sharing the same fate as Norwegian company Oda, which suffered a major valuation cut in the last month of 2022 and lost its unicorn status.

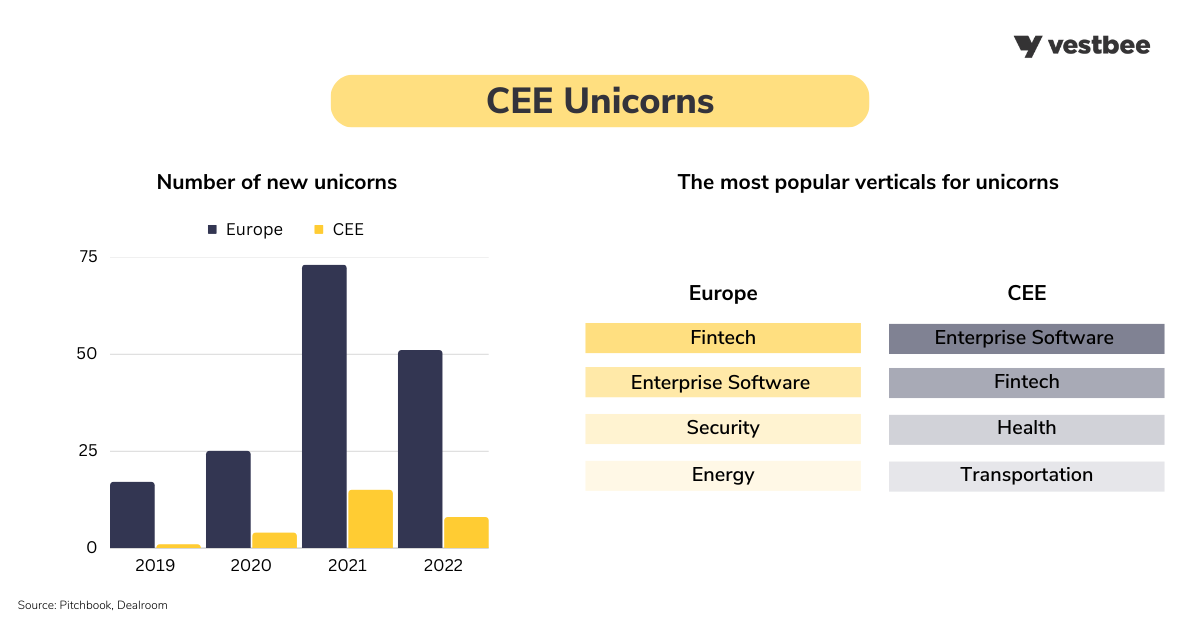

According to the sectoral analysis of European unicorns, fintech is the clear leader among all verticals, followed closely by enterprise software, security, and energy sectors.

According to the Affinity reports, investors with the biggest share of European unicorns in their portfolios include Index Ventures, DST Global, Accel, Goldman Sachs, Baillie Gifford, Wellington Management, SoftBank and Tiger Global Management. Furthermore, names that should be mentioned when it comes to the top investors with 2022 unicorn rounds, include Tiger Global, Index Ventures, Accel, Eurazeo, General Catalyst Partners, Insight Partners, Coatue Management, Tencent, Lightspeed Venture Partners, Global Founders Capital, to name a few.

Additionally, the European ecosystem is known for its diversity and decentralization, with 24 European countries having at least one unicorn. This is particularly notable when compared to the more centralized and concentrated nature of the United States. However, there are still significant disparities between Western and Eastern Europe, and it is important to examine these closely. Now, let's focus on the CEE region and the characteristics of its €1 billion+ companies.

Unicorns: a backdrop in the CEE

Despite the economic turmoil in 2022, the CEE region has demonstrated remarkable resilience to these challenges. So far, as it is stated in Dealroom’s Central and Eastern European startups 2022 publication, we have not seen big slashes in startup valuations, unlike those seen in the West. However, the total value of venture capital investments did decrease in 2022, from a record-breaking €5.4B in 2021 to €4.9 recorded at the end of Q3 2022. Despite this drop, the numbers have still doubled since 2020, according to Vestbee reports.

The combined enterprise value of CEE startups has quadrupled in the last five years, now totalling €190 billion and outpacing the average yearly growth rate recorded in Europe (4x in CEE, 3.1x in Europe).

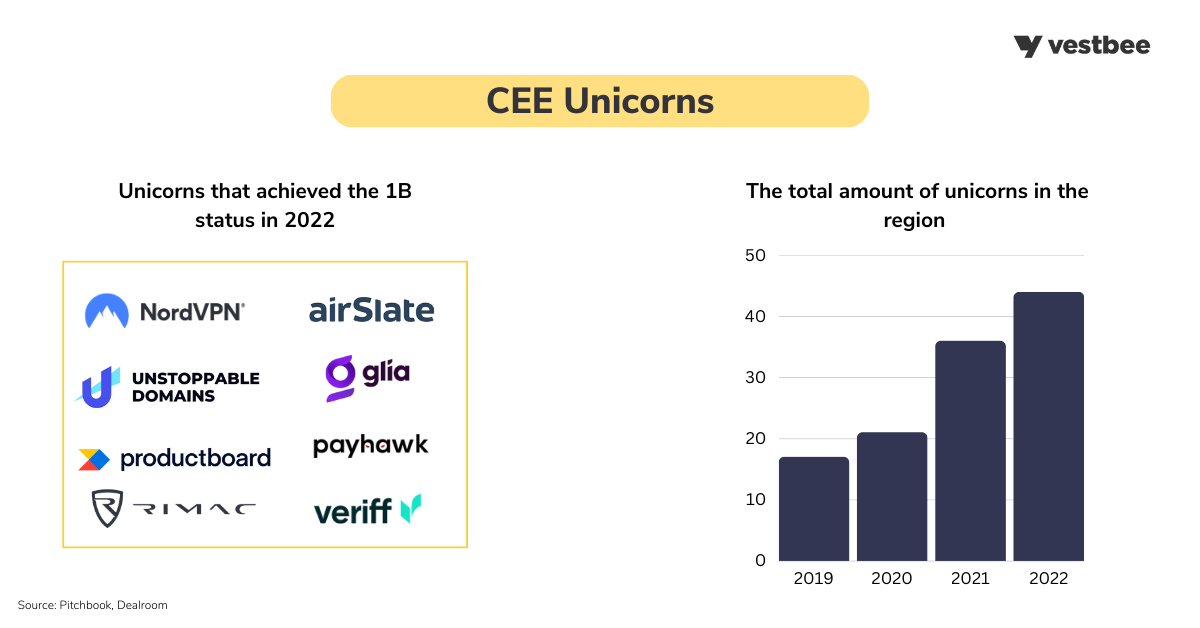

This positive trend is reflected in the creation of regional unicorns. 2021 and 2022 were particularly strong years for CEE billion-dollar companies, in fact, more than half of them emerged in these two years alone. As the ecosystem matured, it attracted more attention from international investors, encouraged more cross-border collaborations between regional venture capital firms, and in turn, the amount and proportion of funding that went to late-stage startups grew. As a result, the influx of mega-rounds fueled the development of local unicorns. In 2021 there were 15 new unicorns, 8 in 2022, and as of Q3 2022, the region has produced 44 unicorns in total. However, it must be noted that these €1 billion+ companies were also affected by the slowdown - they were still closing deals, but their rounds have shrunk. And even though more and more unicorns are emerging in the region as a whole, the data suggests a cooling trend in valuations.

Nonetheless, in recent years, the CEE unicorns have been scaling much faster - the average time to hit unicorn status for startups established in the last ten years was 7 years, whilst for those established in 2001-2010 it was 12 years. What is more, for the earliest companies created between 1990-2000 it was more than 19 years.

In 2022, the following companies from CEE reached a billion-dollar status:

- AirSlate (Ukraine)

- Rimac Automobili (Croatia, €500M Series D + €100M Series C)

- Nord Security (Lithuania, €100M Late VC)

- Glia (Estonia)

- Payhawk (Bulgaria)

- Productboard (Czechia, €125M Series D)

- Veriff (Estonia, €100M Series C)

- Unstoppable Domains (Ukraine)

The rise of these companies has been facilitated by the strong VC presence in the region (of both regional and international investors), which noticed CEE’s surging potential. Amongst the most notable international investors present in the region, with unicorns in their portfolios, there are Index Ventures (Productboard, Printify and Rohlik), Accel (UiPath, Vinted, Veriff), Bessemer Venture Partners (Productboard, Pipedrive), Molten Ventures (Wise), Atomico (Pipedrive, Katana), Sequoia (Bolt, UiPath, Productboard), Insight Partners (Vinted, Pipedrive), Creandum (Bolt, Seon) and Earlybird VC (UiPath, Payhawk).

Amongst the regional VC funds, it’s worth mentioning KAYA (Rohlik, Docplanner, Booksy), Orbit Capital (Rohlik), Eleven Ventures (Payhawk), Inovo VC (Booksy), Credo (UiPath, Productboard), and Superangel (Veriff).

Moreover, in 2022 there were 6 mega founding rounds, worth more than 100M, which included:

- Bolt (628M - Sequoia Capital, Fidelity Management, Whale Rock, Owl Rock, D1, G Squared, Tekne, Ghisallo)

- Rimac (500M - Softbank, Goldman Sachs)

- Rohlik (220M - Sofina, Index Ventures, Tomáš Čupr, et al)

- PayHawk (212M - Lightspeed Venture Capital, Sprints Capital, Endeavor Catalyst, HubSpot Ventures, Jigsaw VC)

- Veriff (100M - Tiger Global, Alkeon, IVP, Accel)

- Nord VPN (92M - Novator, Burda Principal Investments, General Catalyst, Ilkka Paananen, Miki Kuusi, Matt Mullenweg)

In terms of industry verticals, enterprise software leads in the CEE region, attracting twice as much venture capital funding as in the rest of Europe. It is closely followed by fintech, health, transportation, and gaming.

It is worth mentioning that the most notable CEE gaming companies are a unique case in the region. All of the largest companies such as CD Projekt, Ten Square Games, Play Way, and Huuge originate from Poland. They have made quick exits by becoming publicly listed on stock exchanges through IPOs while maintaining a strong local presence and retaining a majority of the workforce in the country. In general, it is widely observed that startups relocate as they scale, and CEE startups are more likely to do so than the European average. Big names such as Infobip (originally from Croatia) and Payhawk (Bulgaria) relocated to the UK, while GitLab, Grammarly, UiPath, and Glia moved to the US. However, as seen with the Polish gaming companies, even as they move their headquarters abroad, a significant proportion of the workforce is often retained in the CEE, sometimes even up to 90%.

Regarding the subsequent developments of unicorns, it’s worth pointing out that in 2022 no European unicorn became public. Given the unfavourable conditions in the market, the companies have decided to stay private longer rather than risk their valuations. As long as the VC funding is available they can flourish in the ecosystem, without the additional regulatory and reporting costs associated with the IPO preparations.

When the funding is considered, it is important to mention that almost a quarter of CEE-born unicorns or soon-to-be unicorns haven’t been backed by VC money. In fact, 10 of them were completely bootstrapped, including Allegro, Grammarly, CD Project, Playway, Wargaming, Jet Beans, Infobip, CCC, Printful, and Playtech. As Dealroom states, In Europe as a whole, only 7% of all unicorns were bootstrapped.

Most notable exits, unicorns, and soon-to-be unicorns in the CEE region by country

The startup ecosystems of the CEE countries share many similarities and often follow a similar growth trajectory, nonetheless, there are many differences between them. In terms of VC funding received in 2022, Estonia, the Czech Republic, Croatia and Poland were leading the region and accounted for nearly 70% of the total. Estonia, Romania, and Poland have created the most startup value since 2000.

Estonia, in particular, is a very interesting case not only in the CEE region, but in Europe as a whole - it is one of the smallest countries, yet with one of the biggest startup ecosystems. It has more startups per capita and has raised more investment per capita than any other country in Europe.

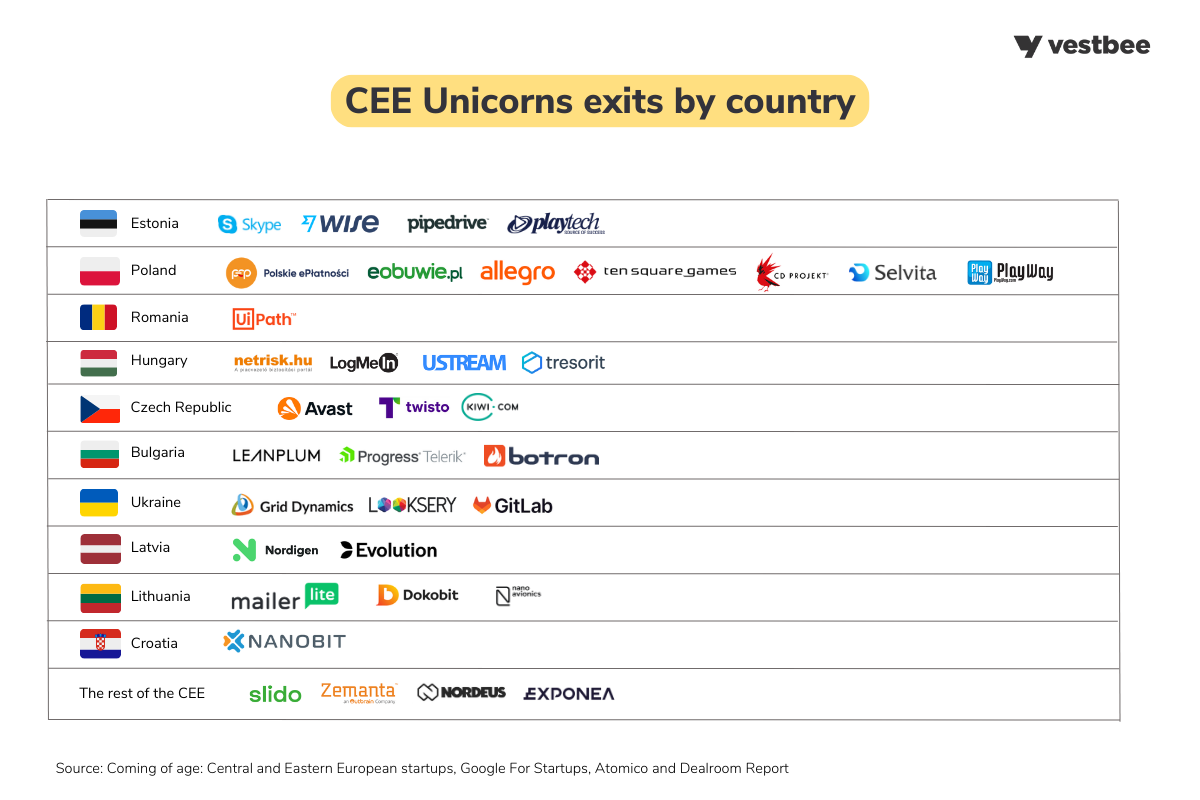

Exits

Estonia: Skype, Wise, Pipedrive, Playtech

Poland: Polskie ePlatnosci, eObuwie, Allegro, Ten Square Games, CD Project, Selvita, WP, InPost, LiveChat, PlayWay, Huuge

Romania: UiPath

Hungary: Netrisk.hu, LogMeIn, Ustream, Tresorit

The Czech Republic: Avast, Socialbakers, AVG, Twisto, Kiwi.com

Ukraine: Grid Dynamics, Looksery, GitLab

Bulgaria: Lean Plum, Progress Telerik, Botron, SMS bump

Latvia: Nordigen, Evolution

Lithuania: MailerLite, Nano Avionics, Dokobit

Croatia: Nanobit

Rest of the CEE (Western Balkans, Slovakia and Slovenia): Slido, Zemanta, Minit, Nordeus, Outfit7, Exponea

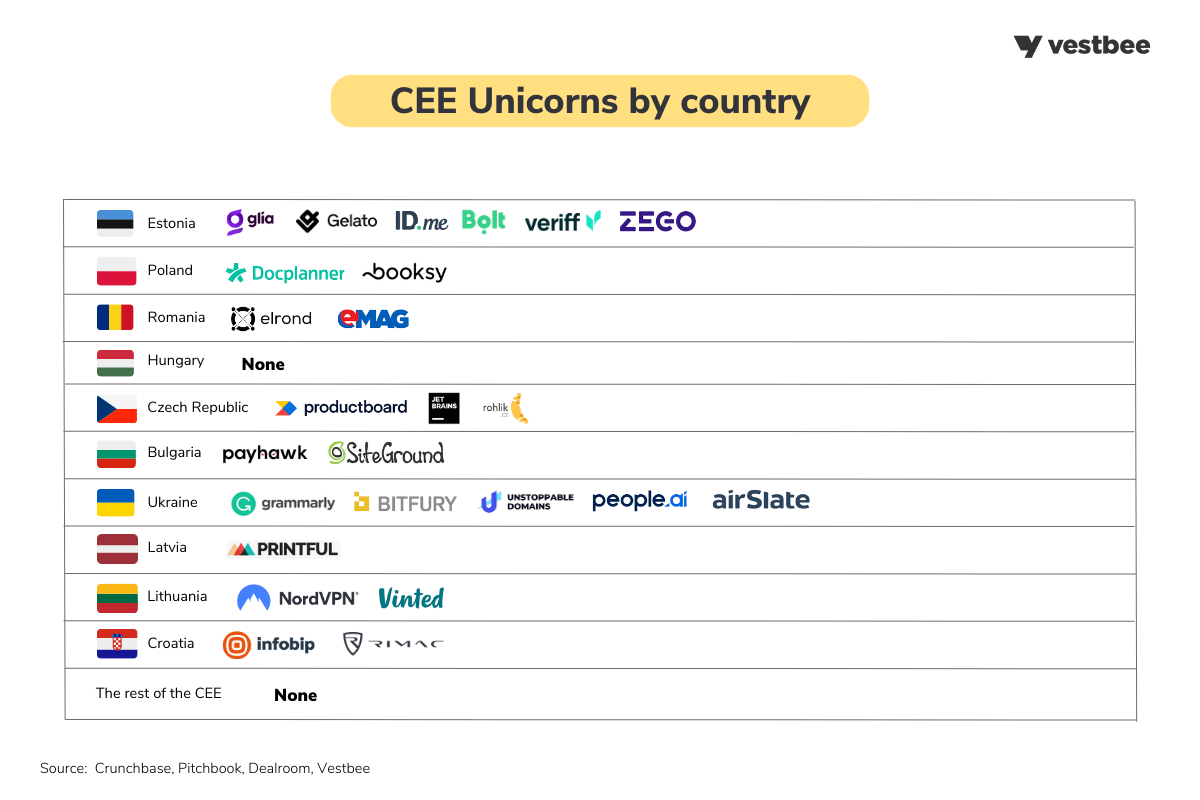

Unicorns

Estonia: Glia, Gelato, ID.me, Bolt, Zego, Veriff

Poland: Docplanner, Booksy

Romania: Elrond, Emag

Hungary: None

The Czech Republic: Productboard, Jetbrains, Rohlik

Ukraine: Grammarly, Bitfury, Unstoppable Domains, People.ai, Airslate

Bulgaria: Payhawk, Siteground

Latvia: Printful

Lithuania: Nord, Vinted

Croatia: Infobip, Rimac

Rest of the CEE (Western Balkans, Slovakia and Slovenia): None

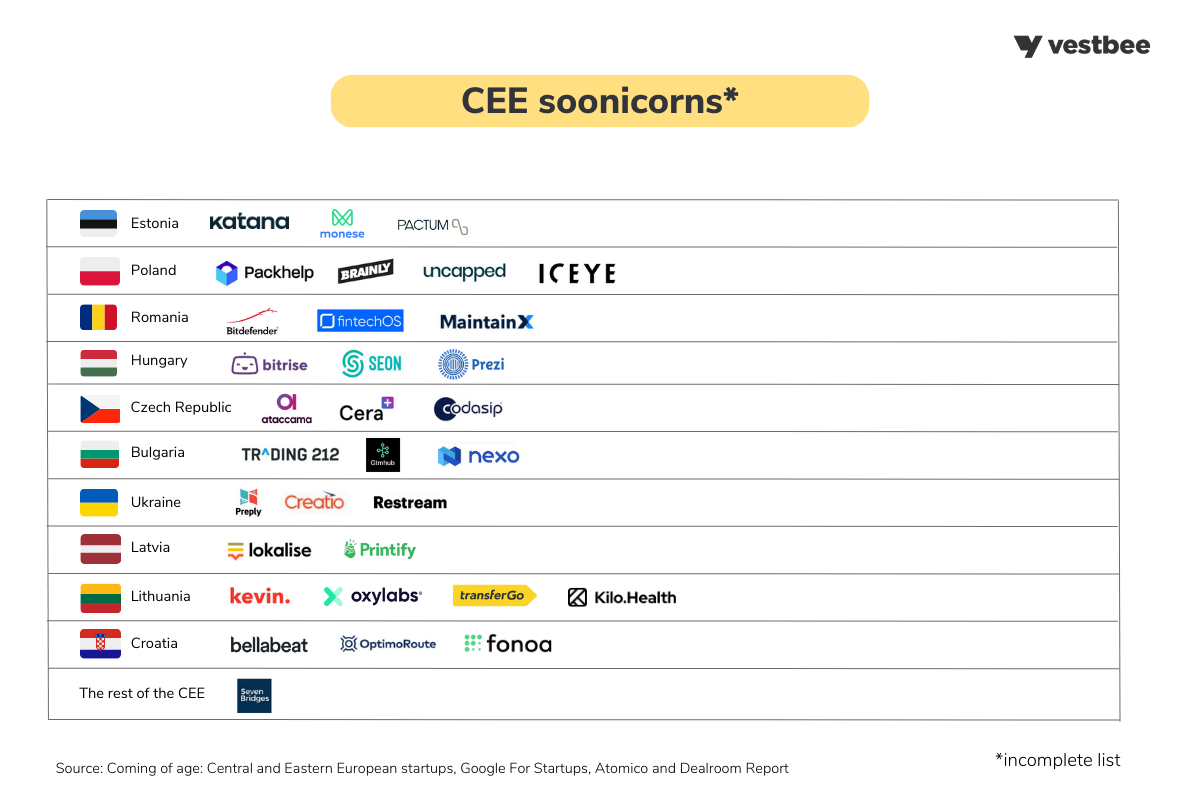

Soonicorns

Estonia: Katana, Monese, Skeleton, Eurora

Poland: Packhelp, Brainly, Silent Eight, Ramp, ICEYE, Uncapped

Romania: Bitdefender, FintechOS, MaintainX

Hungary: Bitrise, Seon, Prezi

The Czech Republic: Ataccama, Dodo, Cera

Ukraine: Creation, Restream, Preply

Bulgaria: Nexo, Gtmhub, Trading 212

Latvia: Lokalise, Printify

Lithuania: Oxylabs, Kilo.health, Kevin., Transfer GO

Croatia: Fonoa, Cognism

Rest of the CEE (Western Balkans, Slovakia and Slovenia): Seven Bridges

Source: Central and Eastern European startups 2022, Report by Dealroom and Atomico, November 2022

Most notable privately-held CEE companies, which became unicorns after 2010

*All valuations have been taken from Crunchbase

AirSlate

Originally from: Ukraine

Founded in: 2006

Became a unicorn in: 2022

Vertical: SaaS

Valuation: $181.5M

Investors: General Catalyst, Silicon Valley Bank, G Squared, Morgan Stanley Expansion Capital, HighSage Ventures, UiPath Ventures

AirSlate is a global SaaS technology company that provides no-code business process automation and document management solutions. The company's PDF editing, e-signature workflow, and business process automation solutions empower users to digitally transform their businesses to run faster and easier.

Rimac Group

Originally from: Croatia

Founded in: 2009

Became unicorn in: 2022

Vertical: Electric mobility

Valuation: $875.8M

Investors: SoftBank Vision Fund, Goldman Sachs, Porsche Ventures, Integrated Capital, InvestIndustrial Holdings

Rimac is a technology powerhouse that manufactures electric hypercars and provides full technology solutions to global automotive manufacturers. It has challenged the status quo with the vision to revolutionize and reinvent the sports car with its unique technology, successfully tackling the electrification challenge set upon the automotive industry.

Nord Security

Originally from: Lithuania

Founded in: 2012

Became unicorn in: 2022

Vertical: Cyber Security

Valuation: $100M

Investors: llusian Family Office, Matt Mullenweg, General Catalyst, Ikka Paananen, Miki Kuusi, Burda Principal Investments, Novator

Nord Security operates as an internet privacy and security provider for individuals and businesses. Its product portfolio includes the NordVPN offering and its Surfshark consumer line of solutions. In 2021 the company acquired Atlas VPN.

Glia

Originally from: Estonia

Founded in: 2012

Became unicorn in: 2022

Vertical: SaaS

Valuation: $152M

Investors: RingCentral Ventures, Insight Partners, Wildcat Capital Management, Donald Brown, Insight Partners, Tola Capital, ERA, Grassy Creek Ventures, Temerity Capital Partners

Glia is on a mission to reinvent how businesses support their customers in a digital world, partnering with many financial institutions all around the world. Glia's Digital Customer Service (DCS) solution enriches web and mobile experiences with digital communication choices, on-screen collaboration, and AI-enabled assistance.

Payhawk

Originally from: Bulgaria

Founded in: 2018

Became unicorn in: 2022

Vertical: Fintech

Valuation: $239.1M

Investors: Earlybird VC, Eleven Ventures, Vassil Terziev, QED Investors, Sprints, HubSpot Ventures, Endeavor Catalyst and more

Payhawk is a financial software that simplifies the process of tracking expenses, payments, and card spendings for growing businesses. The platform enables financial officers and business owners to manage the entire spending lifecycle end-to-end. It collects and analyzes receipts, invoices, and card transactions to help stay in control of the budget with no paperwork for the employees.

Productboard

Originally from: The Czech Republic

Founded in: 2014

Became unicorn in: 2022

Vertical: Product management

Valuation: $261.7M

Investors: Index Ventures, Reflex Capital, Credo Ventures, Sequoia Capital, Bessemer Venture partners, Tiger Global Management and more

Productboard is the product management system that helps product teams understand what customers need, prioritize what to build next, and align everyone around the roadmap.

Veriff

Originally from: Estonia

Founded in: 2015

Became unicorn in: 2022

Vertical: Cyber security

Valuation: $192.3M

Investors: Y Combinator, Superangel, SV Angel, IVP, Accel, Mosaic Ventures, LIFT99, NordicNinja VC, Alkeon Capital, Change Ventures and more

Veriff is an online identity verification company that protects businesses and their customers from online identity fraud. The highly automated machine learning-based platform connects companies with honest customers, helping them avoid the risks of digital fraud.

Unstoppable Domains

Originally from: Ukraine

Founded in: 2018

Became unicorn in: 2022

Vertical: Web3

Valuation: $72M

Investors: Boost VC, Gaingels, El Ventures, Protocol Labs, Pantera Capital, Rainfall Ventures, OKG Ventures and more

Unstoppable Domains is a platform that launches NFT domains secured by blockchains and builds uncensorable websites. It allows people to control their digital identity, use their usernames to log into more than 150 Web3 applications, and much more.

DocPlanner Group

Originally from: Poland

Founded in: 2011

Became unicorn in: 2021

Vertical: Healthcare

Valuation (Crunchbase): $140.5M

Investors: Piton Capital, RTA.vc, KAYA, Point Nine, One Peak Partners, Target Global, Winter Capital and more

DocPlanner is a booking platform which allows patients to find easily the perfect doctor and book an appointment. They also help doctors to better manage their practice and build their online reputation.

Elrond

Originally from: Malta-founded and Romania-based

Founded in: 2018

Became unicorn in: 2021

Vertical: Blockchain

Valuation: $1.9M

Investors: Authorito Capital, Woodstock Fund, Maven 11 Capital, NGC Partners, Mapleblock Capital, Binance Labs and more

Elrond specializes in building a high bandwidth, low latency, high security, a low-cost blockchain network that can accommodate transactions and value exchange at the internet scale. The company developed improvements in throughput, execution speed, and transaction cost.

People.ai

Originally from: Ukraine

Founded in: 2016

Became unicorn in: 202

Vertical: AI, enterprise software

Valuation (Crunchbase): $200M

Investors: Y Combinator, Lightspeed Ventures, ICONIQ Capital, SV Angel, GGV Capital, UpVentures Capital and more

People.ai is an AI platform for enterprise revenue, helping all departments, from sales, and marketing to customer services, to utilize all revenue opportunities. It captures all customer contacts, activity, and engagement as well as leveraging AI technology to deliver sales performance analytics, personalized coaching, one-on-one feedback, and pipeline reviews.

Printful

Originally from: Latvia

Founded in: 2013

Became unicorn in: 2021

Vertical: Delivery, E-commerce

Valuation: $130M

Investors: Bregal Sagemount

Printful is a print-on-demand drop shipping and fulfillment company that helps people turn their ideas into brands and products. The company fulfills and ships custom clothing, accessories, and home & living items for online businesses.

ID.me

Originally from: Estonia

Founded in: 2010

Became unicorn in: 2021

Vertical: Cloud Data Software

Valuation: $275.2M

Investors: Moonshots Capital, Stony Lonesome Group, Blu Venture Investors, BoxGroup, Musha Ventures, Lyft and more

ID.me is a digital identity network that aims to simplify the user's indication verification experience. It provides identity proofing, authentication, and group affiliation verification for organizations across sectors.

Zego

Originally from: Estonia

Founded in: 2016

Became unicorn in: 2021

Vertical: Auto Insurance

Valuation: $281.7M

Investors: Target Global, Socil Capital, Latitude, Balderton Capital, DST Global, Upscale and more

Zego is a commercial motor insurance provider that powers opportunities for businesses, from entire fleets of vehicles to self-employed drivers and riders. It combines best-in-class technology with sophisticated data sources to offer insurance products that save businesses time and money.

Rohlik

Originally from: The Czech Republic

Founded in: 2014

Became unicorn in: 2021

Vertical: Delivery Service, E-commerce

Valuation: $613.1M

Investors: Index Ventures, KAYA, Quadrille Capital, Partech, ORBIT Capital, EBRD and more

Rohlik is an innovative grocery delivery company that offers a 90-minute same-day delivery service. Its mission is to help people live happily and healthily whilst making their lives easier through technologically advanced delivery services coupled with excellent customer service.

Infobip

Originally from: Croatia

Founded in: 2006

Became unicorn in: 2020

Vertical: Enterprise Software

Valuation: $800M

Investors: BlackRock, One Equity Partners, Ares Management

Infobip specializes in omnichannel engagement powering a range of messaging channels, tools, and solutions for advanced customer engagement, authentication, and security. The company helps its clients and partners overcome the complexity of consumer communications, grow their business, and enhance the customer experience in a fast, secure and reliable way.

Gelato

Originally from: Estonia (and Norway)

Founded in: 2007

Became unicorn in: 2020

Vertical: E-commerce

Valuation (Crunchbase): $269M

Investors: Dawn Capital, SEB Pension Fund, Goldman Sachs Asset Management, SoftBank Vision Fund, Insight Partners

Gelato is a fast, smart and green one-stop-shop for customized print products on demand. Their solution enables entrepreneurs, creators, and global brands to sell their products globally and produce them locally in 30 countries, reaching up to 5 billion potential consumers overnight and in turn scaling their e-commerce business to new markets.

Jet Brains

Originally from: Czech Republic

Founded in: 2000

Became unicorn in: 2020

Vertical: Enterprise Software

Valuation: Not disclosed

Investors: Not disclosed

JetBrains is a global software vendor specializing in the creation of intelligent, productivity-enhancing tools for software developers and project managers. It has headquarters in Prague, Czech Republic, with R&D labs located in Amsterdam, Boston, Berlin, and Munich and offices all over the world in locations such as Amsterdam; Foster City, California; Marlton, New Jersey; and Shanghai. In 2011 the company created the Kotlin programming language.

Pipedrive

Originally from: Estonia

Founded in: 2010

Became unicorn in: 2020

Vertical: SaaS, CRM

Valuation: $90.2M

Investors: Rembrandt Venture Partners, Bessemer Venture Partners, AngelPad, Atomico, Insight Partners, TMT Investments, SquareOne and more

Pipedrive is the global sales-first CRM and intelligent revenue platform for small businesses. It is helping more than 100,000 sales teams worldwide to get more qualified leads, close deals faster, and grow their revenue. The company has been acquired by Vista Equity Partners.

Vinted

Originally from: Lithuania

Founded in: 2008

Became unicorn in: 2019

Vertical: E-commerce

Valuation: $562.3M

Investors: Insight Partners, Accel, FJ Labs,Sprints, Burda Principal Investments, Lightspeed Venture Partners, Full in Partners and more

Vinted is an online peer-to-peer marketplace, where users can buy, sell, and swap clothes with ease and at a low cost. It aims to popularise second-hand shopping for clothes and accessories, which directly contributes to waste reduction.

Bolt

Originally from: Estonia

Founded in: 2013

Became unicorn in: 2018

Vertical: Transportation

Valuation: $2B

Investors: G Squared, Naya Capital, D1 Capital Partners, Sequoia Capital, Korelya Capital, Superangel, Startup Wise Guys, Mobi, NordicNinja VC, International Finance Corporation, Patio Ventures

Bolt is an Estonian mobility company that offers car hire, micromobility and food delivery services. It is one of the fastest-growing startups, present in 35+ countries across the globe. Their aim is to help cities evolve towards decreased traffic congestion and pollution through flexible urban mobility which requires less car ownership.

Bitfury

Originally from: Ukraine

Founded in: 2011

Became unicorn in: 2018

Vertical: Blockchain

Valuation: $170M

Investors: Georgian Co-Investment Fund, iTech Capital, Binary Financials, ZAD Investments, Korelya Capital, DRW Venture Capital, Galaxy Digital, Armat Group, and more

Bitfury is the leading full-service blockchain technology company and one of the largest private infrastructure providers in the blockchain ecosystem. Bitfury develops and delivers both the software and the hardware solutions necessary for businesses, governments, organizations, and individuals to securely move an asset across the blockchain.

Grammarly

Originally from: Ukraine

Founded in: 2009

Became unicorn in: 2017

Vertical: AI, SaaS

Valuation: $400M

Investors: General Catalyst, IVP, Sozo Ventures, Spark Capital, SignalFire, and more

Grammarly develops writing assistance technology, using a combination of technical approach and human expertise to offer unmatched, market-leading communication support to individuals, students and enterprises. In order to do so they deploy advanced machine learning and AI to break new ground in natural language processing that analyzes written sentences to understand context and tone.

Sources:

VC Funding In CEE Report - 3Q 2022

VC Funding In CEE Report - 2Q 2022

VC Funding In CEE Report - 1Q 2022

Central and Eastern European startups 2022, Dealroom report, November 2022

Coming of age: Central and Eastern European startups, Dealroom report, October 2021

European VC Pulse Check H1 2022, Dealroom report, August 2022

The Relationship Intelligence Benchmark Report: European Unicorn Edition, Affinity, June 2022

European unicorn creation races ahead of global peers, Pitchbook, July 2022

Crunchbase, Pitchbook

Related Posts:

VC Trends Shaping CEE Startup Ecosystem In 2023 (by Olga Chechłacz, Editor, Vestbee)

New VC Funds Investing in Europe - 4Q 2022 (by Ilya Mikhalchyk-Kananenka, Community Builder, Vestbee)

Outlook Of The CEE Startup and VC Ecosystem In 2023 (by Katarzyna Groszkowska, Editor, Vestbee)