VC Landscape in 2023

According to Crunchbase, global VC funding in all of 2023 reached $285 billion, the lowest it has been since 2017. The industry is 38% down overall – sharper declines were seen in early stage (42%) and late stage (37%), which account for 90% of deal value, and seed stage down just over 30%. Even comparing it to a more normal, pre-pandemic levels it’s still about 20% down from 2018-2020.

European Ecosystem accounted for less than 20% of global VC funding in the past year ($52 billion) and felt a similar YoY decline (39%). The deal volume, however, is higher than pre-pandemic levels.

The funding drought and inflated valuations of 2021 caused several issues for the industry: multiple flat and down-rounds, another waves of layoffs and a shift from hyper-aggressive growth towards sustainability and efficiency.

SaaS Companies in 2023

Public SaaS companies in 2023 have performed really well, with BVP Emerging Cloud Index growing 36,9% YoY (on par with NASDAQ’s 39,7% growth) and outperforming both S&P500 and Dow Jones (+22,2% and +12% YoY growth respectively).

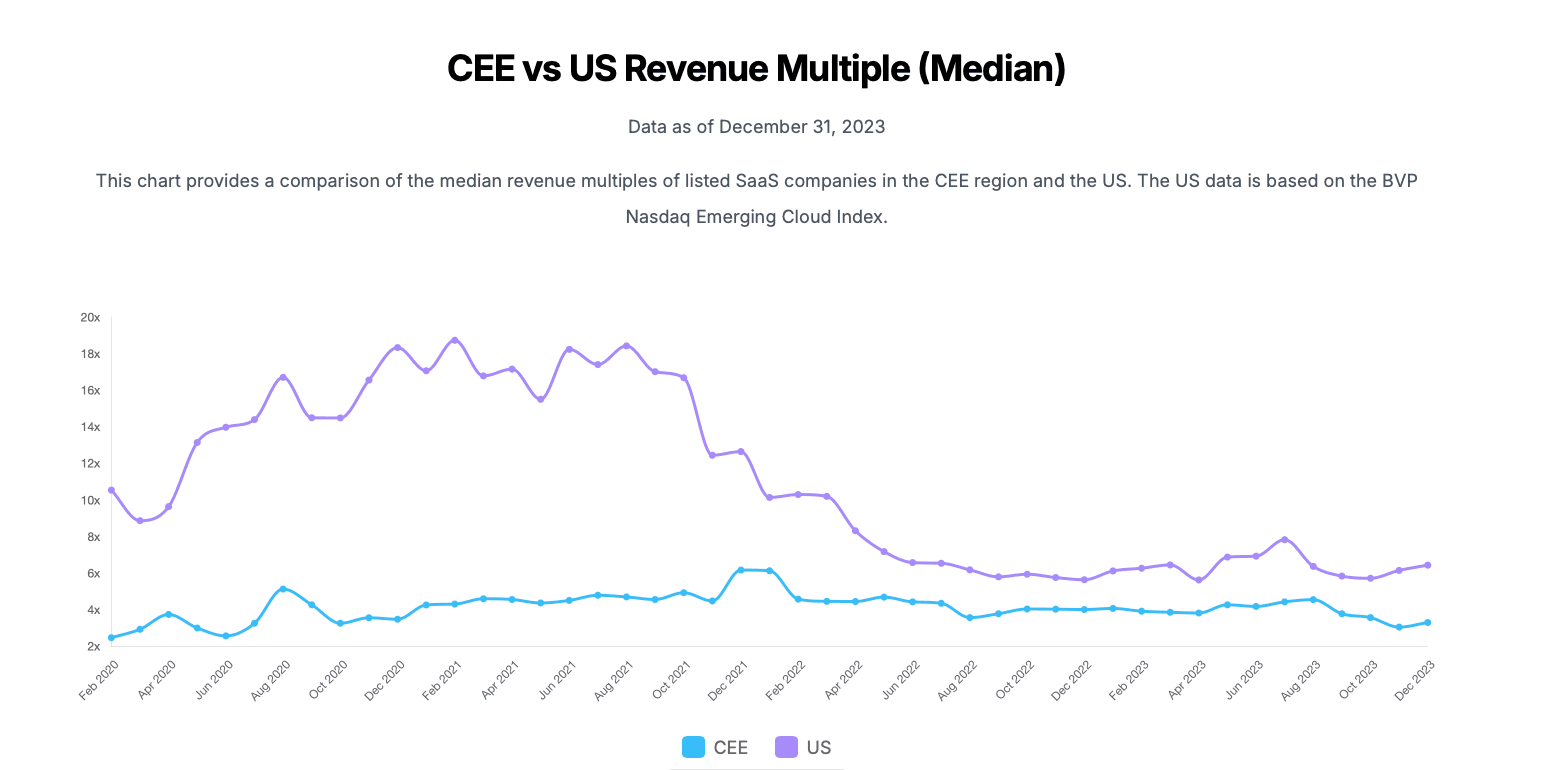

The median revenue multiple across 2023 fluctuated around 6x and investors were more optimistic at the end of 2023, compared to the year before with a 14% increase in revenue multiple (6,44x vs 5,64x), and the median revenue growth of SaaS companies listed on Nasdaq in 2023 was 18,9%.

A different picture, however, can be seen looking at a 3 year horizon. During that time the Cloud Index performed much worse than NASDAQ, S&P500 and Dow Jones – seeing a 37% fall since the beginning of 2021 (whereas competing indices rose by 14%, 25,2% and 21% over that period). The median revenue multiple fell from it’s peak of almost 19x in early 2021 by 70% to today’s value of 6,44x. This is correlated with the slowdown of revenue growth among companies included in the BVP Cloud Index – from over 30% growth rate in most of 2021 to 18,9% in December 2023.

In Q3 summary we were a tad optimistic about the new activity on the public markets. We saw IPOs of 3 highly valued tech companies in Klaviyo , ARM and Instacart. Unfortunately, our optimism quickly disappeared as these were the last major debuts that year. So far, year 2024 doesn’t look any more promising, as according to SaaStr, so far only one SaaS company (ServiceTitan, a provider of cloud-based software designed to accelerate the home and commercial service industries) is preparing an IPO in the first half of 2024.

Key updates from the CEE SaaS Index for 2023:

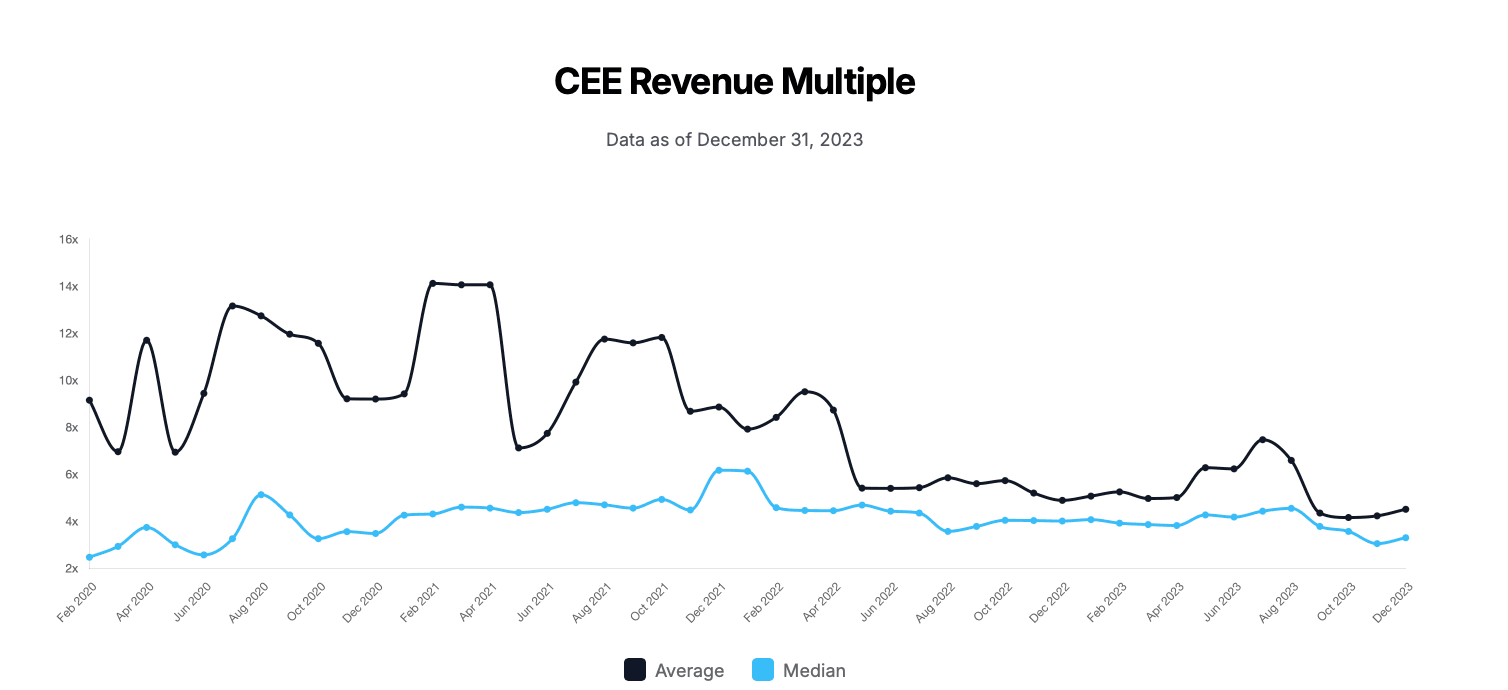

- The median CEE revenue multiple at the end of 2023 amounted to 3,30x annualized revenue (down 40% from an all-time high of 5,51x in December 2021), and down 27% from this year’s record of 4,55 in September.

- Market capitalization of all companies included in the CEE SaaS Index remained stable at €1.75 billion – remaining at this level from Q2 of this year.

- Investors, both in the CEE and the US were most optimistic during the summer. The US median revenue multiple was the highest in July (7,83x), and the CEE SaaS Index reached it’s high point of 4,55x in August. The lowest multiples in the CEE and the US were noted in November (3,05x) and April (5,63x) respectively.

- For most of the year revenue multiples in the CEE were about 40% lower than in the US (the lowest difference of 29% was noted in August 2023), but in the last two months of the year the gap rose to 50%. While in Central and Eastern Europe the median multiple in December is 19% lower than at the beginning of the year, the American index saw a 5% increase over the same period.

About CEE SaaS Index

CEE SaaS Index is a simple tool for startups and investors to value SaaS companies in Central & Eastern Europe based on revenue multiples from publicly traded SaaS companies from the CEE region, developed by Vestbee and Warsaw Equity Group.

While revenue multiples from publicly traded SaaS companies can provide a helpful starting point for valuation, currently available indexes are only based on US-listed SaaS companies, leaving the CEE region without relevant benchmarks, despite the region's thriving startup ecosystem and quadrupled VC funding over the last three years.

With projected growth and increased investment in CEE tech companies, a more appropriate valuation benchmark for regional startups and investors is required. To meet this need, Vestbee and the Warsaw Equity Group have collaborated to develop the CEE SaaS Index, providing a relevant benchmark for both regional and international investors.

Related Posts:

CEE SaaS Index - September 2023 update (by Ewa Chronowska, CEO, Vestbee & Paweł Maj, Partner, Warsaw Equity Group)

CEE SaaS Index - June 2023 update (by Ewa Chronowska, CEO, Vestbee & Paweł Maj, Partner, Warsaw Equity Group)

Vestbee and WEG launch CEE SaaS Index valuation tool for startups (by Konrad Koncerewicz, Head of VC & Startups, Vestbee)